ESG Economist - Copper remains very essential in energy transition

The dominant critical or strategic metals are indispensable in the energy transition and are sometimes referred to as the new oil. In the IEA's three forward-looking scenarios, growth in demand for metals and minerals increases sharply, with the strongest growth until 2030. Demand for copper for making clean technologies is the most dominant in terms of volume, followed by demand for graphite; in terms of growth, lithium stands out with almost a nine-fold increase by 2040. With this, copper - besides being an indicator of the health of the global economy - has also become a good gauge of the energy transition.

A smooth energy transition will require business processes to become increasingly less dependent on fossil fuels at a faster pace. On the path to climate neutrality, the need for low-carbon technologies will rise sharply, thereby also increasing demand for critical metals essential for making all kinds of non-fossil technologies. The energy transition has the effect of increasing pressure on metals markets. Increasing quantities of metals such as copper, nickel, cobalt and lithium will be needed in the coming years, while supply will struggle to match this stronger growth. In this analysis, we take a closer look at the most dominant critical or strategic metals needed and, above all, indispensable in the energy transition. We look at how demand for those metals will evolve in the coming years under different IEA scenarios and how these metals will affect the price trend for energy transition metals.

Metals demand under various transition scenario’s

It is especially the critical metals and minerals that are vital for the energy transition, especially for making renewable energy technologies such as solar panels, wind turbines and electric vehicles (EVs). Sometimes they are even referred to as the new oil. The clean technologies have a high metal & mineral intensity. Since the mining of many of these metals and minerals is concentrated in only a few countries, their strategic importance is high. It only increases the pressure on these metal markets in the coming years.

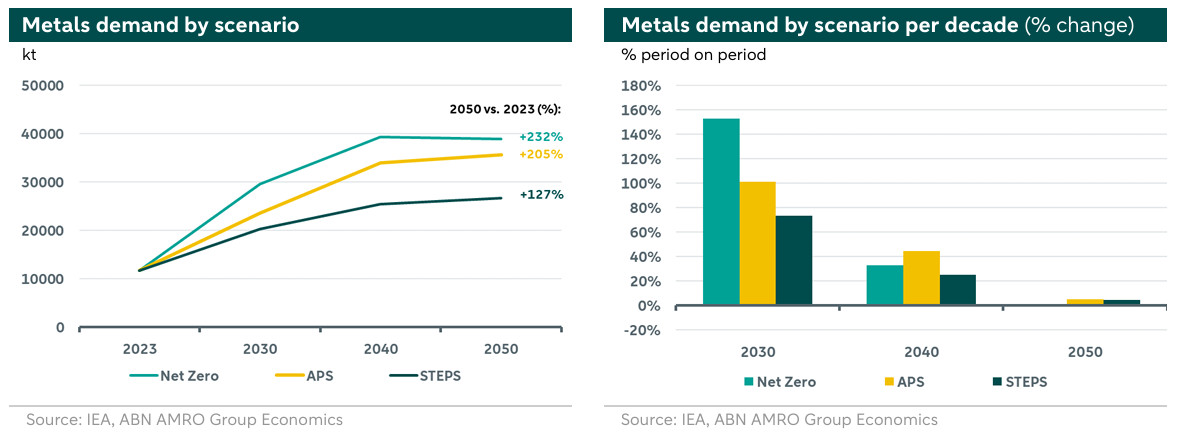

The International Energy Agency (IEA) has compiled three forward-looking scenarios and projected the growth in demand for metals and minerals through 2050 under each scenario. These scenarios are successively the Net Zero Scenario, the Announced Pledges Scenario (APS) and the Stated Policies Scenario (STEPS). Net Zero outlines a path for the global energy sector to achieve net zero CO2 emissions by 2050. The APS assumes that governments will comply fully and on time with all climate-related pledges they have announced as of the end of August 2023. These include both the 2030 targets and commitments to net zero targets or carbon neutrality in the longer term, regardless of whether these announcements are enshrined in legislation or updated in so-called National Determined Contributions (NDCs). The STEPS provides a more conservative benchmark for the future and sets the direction of emission reductions in the energy system, based on current policy proposals.

Whichever path or scenario is eventually taken, demand for metals and minerals will grow strongly. Until 2030, growth in demand for metals and minerals will be strongest. The growth in the Net Zero scenario is by far the strongest up to and including 2030, because in this scenario there will be a firm commitment to the deployment of clean technologies. This is much stronger than in the other scenarios. As a result, demand for transition metals rises much faster. In the medium- to long-term, demand growth then weakens. This is most pronounced in the Net Zero scenario. In each scenario, the demand for and supply of these critical metals will not get too far out of balance over the projected time horizon. The chance of this happening is, however, much greater in a Net Zero scenario than in the other scenarios.

Continuous production of clean technologies and a reliable supply of critical metals and minerals is a prerequisite for the smooth running of the energy transition. The moment the supply of these metals and minerals cannot keep up with the growth in demand, it creates bottlenecks in the supply chain. This imbalance will eventually push up the price of many metals and minerals further, raising concerns about the affordability of the energy transition. Should it come to the point where the price for the primary transition raw materials rises more sharply, this will then encourage further scaling up in recycling capacity and material efficiency.

Metals demand growth remains high in all scenarios

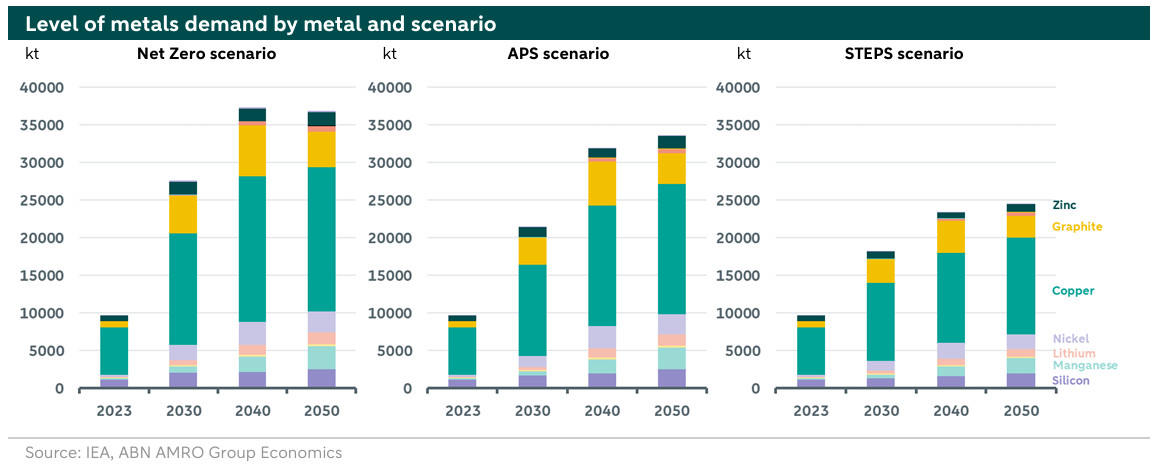

The demand for critical transition metals thus increases sharply in the coming years in all scenarios. The list of these transition metals for making clean technologies is long. In its analysis, the IEA assumes 37 critical metals for 11 specific clean technologies. In terms of volume, 7 metals are dominant in the coming decades. These include copper, graphite, nickel, manganese, silicon, lithium and zinc. Steel and aluminium are also widely used to make many clean energy technologies. However, these are not considered here. Steel is not a critical metal and multiple factors determine the growth in demand for steel. In addition, both steel and aluminium are used to a much lesser extent in the technology itself and much more for the body work of the clean technology.

About 30% of refined copper is used in the production of all kinds of electrical appliances and equipment. About 28% is returned to the construction sector, 16% to infrastructure and 12% to transport, such as conventional cars and trucks, as well as aircraft. Finally, about 5% of the total demand for copper goes to the production of electric vehicles (EVs). Much lithium, graphite and nickel are also destined for EVs. Most of the available lithium and graphite are widely used in batteries, while some 16% of refined nickel goes to the EV battery sector, among others. In addition, manganese is also essential for making EVs and both manganese and silicon are essential for battery technology. However, silicon is also needed for making solar panels and manganese for making wind turbines. Zinc is widely used in clean technologies, such as solar panels and wind turbines.

The increase in volume of these metals are shown in the figure above by scenario. Demand for these metals remains high in all scenarios, with the strongest increase seen in the period up to 2030. The peak in demand in the Net Zero scenario will be in 2040, while in the other scenarios it will not occur until 2050. Demand for copper for making clean technologies is the most dominant in terms of volume, followed by demand for graphite.

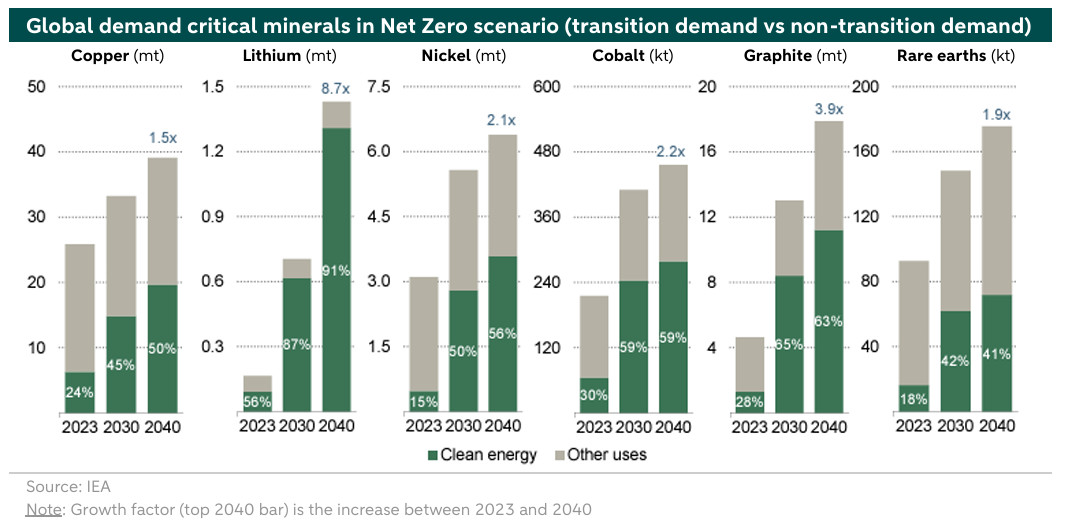

Of the 37 metals on the IEA list, there are then also 7 metals that are the most dominant in terms of growth in the coming decades. These are copper, lithium, nickel, cobalt, graphite and rare earths.

Under the Net Zero scenario, copper demand increases by 50% by 2040 from 2023 levels, according to the IEA. The volumes of copper needed remain by far the largest, but the projected growth rate of copper demand remains in line with historical growth rates. As such, demand for copper is not the strongest growth of these 7 critical transition metals. Demand for nickel, cobalt and rare earth elements is doubling and demand for graphite is increasing by almost a factor of four by 2040. However, demand for lithium stands out the most with almost nine-fold increase by 2040. Furthermore, the share of demand for making clean technologies increases significantly in all cases up to 2040. This often makes the clean energy technologies sector the most dominant end-use sector, especially in the case of lithium.

Transition metals price trends

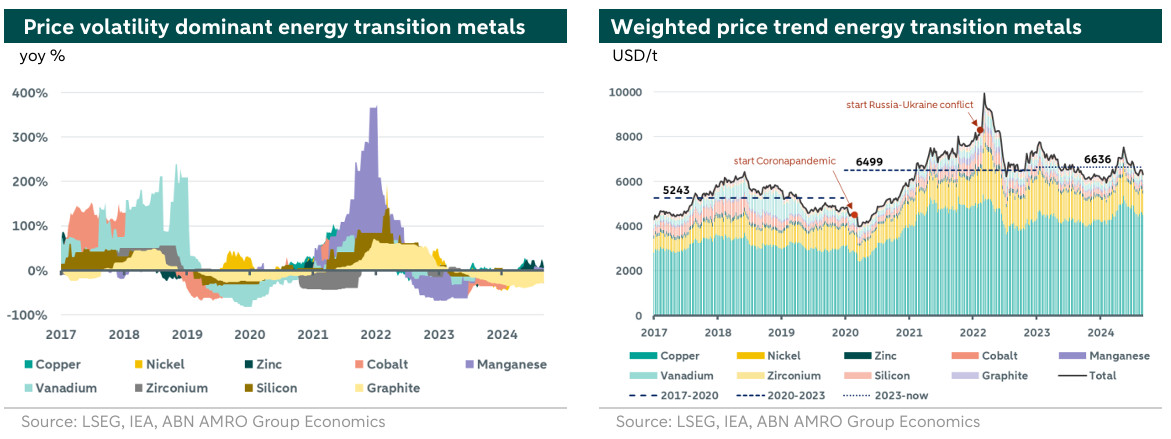

The volatility in the prices of critical metals is high, as can also be seen in the left-hand figure below. It is notable here that the volatility in the base metals (copper, nickel and zinc) is much less than in the so-called minor metals (such as cobalt, manganese, vanadium, zirconium, silicon and graphite). In particular, the prices of manganese, vanadium and cobalt have seen very sharp price rises and falls since 2017.

The lower volatility in the prices of base metals is beneficial as much larger quantities of these metals are needed for the energy transition. As the quantities of minor metals needed for the energy transition are much lower, the strong price volatility in these metals has, on balance, less impact on the trend in the weighted price of transition metals collectively (see right figure above). This weighted price trend for transition metals has been moving in a range between USD 4,000/t and USD 10,000/t since 2017. The low point in this price trend is just after the Corona pandemic outbreak, at a time when the economy came close to a standstill. The peak in the price is reached after the start of Russia's invasion of Ukraine. The average price of these transition metals in the period before the start of the Corona pandemic is about 25% lower than in the period 2020 and beyond. After Russia's invasion of Ukraine, the uncertainty in the metals markets has still not completely disappeared and a lot has to happen before the transition metals price returns to its pre-Corona pandemic levels.

The trend in copper prices has a firm relationship with the strength of the global economy. This is because copper is a metal found in relatively many sectors of an economy. And this makes that trends in the copper market and price can give a good indication of the health of the global economy. The state of China's economy in particular has a lot of influence on trends in the copper market, as the country has a significant share the production of and demand for refined copper. The current state of the Chinese economy is relatively weak, with the downturn in the property sector also depressing domestic demand. Such trends have a negative impact on copper prices. However, these pressures are likely to be temporary. Demand from the energy transition-affiliated sectors is going to increase increasingly in the coming years, thus gaining more influence on copper market trends.

With copper's great dominance - in terms of quantity - in many variants of clean technologies, the metal will eventually also become a gauge of the energy transition. In the process, the possibility of a sharply rising copper price could potentially have a delaying effect on the transition over time. After all, a higher copper price lowers the profitability of many renewable projects. On the other hand, a sharply falling copper price makes the energy transition and its renewable projects more profitable and affordable.

Annually, there is a slight imbalance in the copper market, with demand for refined copper exceeding its supply. However, there is plenty of copper available globally. Copper ore reserves in the earth's crust are huge. According to the US Geological Survey (USGS), the identified copper reserves in the earth's crust are 2.1 billion tonnes of copper and the undiscovered reserves are an estimated 3.5 billion tonnes. This provides many decades of copper extraction and consumption to come. Currently, however, the problem is that extraction capacity is not growing as fast as consumption for refined copper. This can lead to market distortions. As a result, refined copper shortages are expected to increase more sharply after 2027, increasing the likelihood of copper prices rising further. This would eventually encourage investment in extraction capacity. However, higher input costs for making low-carbon technologies hamper production of those technologies, which could potentially create disruption for the energy transition, risking possible delays.