EBA shelves inclusion of environmental and social risks into Pillar 1

The EBA published a report about the appropriateness and feasibility of including ESG factors in the current prudential framework. The regulator notes that there are still challenges regarding ESG data, for instance, the lack of a common, standardized and complete classification system. At this stage, the EBA does not recommend introducing environmental-related adjustment factors in the calculation of banks’ capital requirements.

The European Banking Authority published a report about the appropriateness and feasibility of including ESG factors in the current prudential framework

As the prudential framework aims to safeguard the stability of the financial system, it might be worth adapting the framework to account for environmental and social risks

Nevertheless, environmental and social risks are not considered to be new risks, but rather risks that drive the traditional categories of financial risks through a variety of channels

The regulator notes that there are still a few challenges regarding ESG data worth considering before including it in a regulatory framework, for instance, the lack of a common, standardized and complete classification system

Furthermore, there is also a mismatch between the design of the Pillar 1 framework and the uncertain, long-term nature of environmental and social risks

At this stage, the EBA does not recommend introducing environmental-related adjustment factors in the calculation of banks’ capital requirements

Earlier this month, the European Banking Authority (EBA) published a about the appropriateness and feasibility of including ESG factors in the current prudential framework, and the Pillar 1 Framework in particular. The report follows a discussion paper that the EBA had published in May. Meanwhile, the EBA noted that this report is the first of more reports that will follow regarding the incorporation of environmental risks in the regulatory framework of banks.

The prudential framework in the EU is based on the Basel framework, which aims to ensure that banks are well capitalized and follow prudent risk management, in order to avoid disruptions to the financial system that could impact the entire economy. As such, the framework has been adjusted over time, reflecting the emergence of new risks, climate risk being one of them. Given that environmental and social risks pose financial risks to banks, it raises the question as to whether the prudential framework should be revised accordingly.

The EBA’s report focussed on the question whether environmental and social risks should be incorporated into Pillar 1 capital requirements. These form the starting point for bank capital requirement calculations, addressing credit risk, operational risk, and market risk. Pillar 1 capital requirements are complemented with Pillar 2 and Pillar 3 capital adequacy assessments.

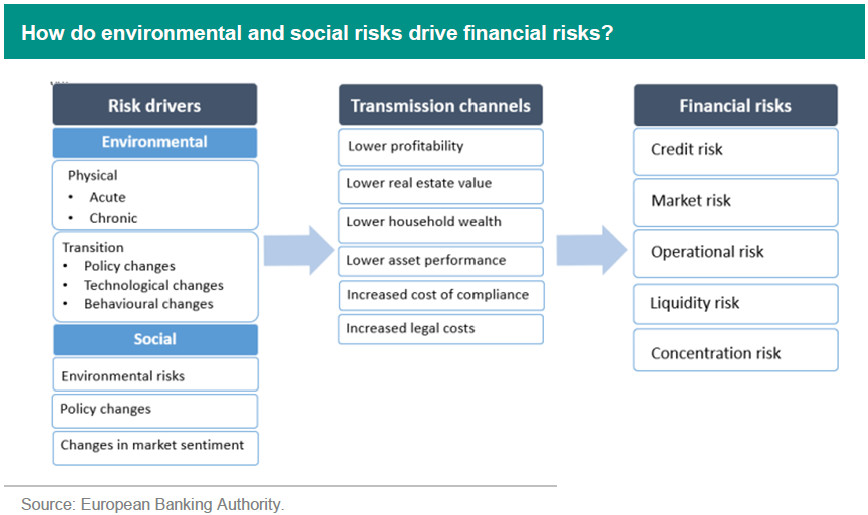

At first glance, it seems fair to include environmental and social factors into Pillar 1 capital requirements, as they pose a risk to bank’s core business activities, such as through their lending activities or through their investment in assets. However, the EBA also notes that environmental and social risks should not be understood as entirely new categories of risk, but rather as risks that drive the traditional categories of financial risks through a variety of transmission channels (such as credit risk). The figure below illustrates the risk drivers as well as their transmission channels on the ‘more traditional’ financial risk factors affecting banks’ balance sheets.

The graph above illustrates how environmental and social factors feed through into credit risk, market risk, among others, which also raises the question of the extent to which they feed through. On this topic, the EBA stresses the uncertainty about the manner that these risks will translate into financial risks, partly due to their non-linearity (a gradual incorporation of environmental and social risks into the Pillar 1 framework versus a sudden jump in unexpected losses for banks due to, for instance, floods or wildfires). Another issue is the extent to which environmental and social risks will affect different sectors in the economy, which could imply differences in financial risks for sustainable and non-sustainable firms (eventually resulting in lower/higher credit risk, respectively).

Meanwhile, the regulator considers that there are still some other challenges concerning the inclusion of environmental and social risks into regular metrics. One of these is related to ESG data. In this respect, the EBA mentions the following:

Availability of relevant, high-quality and granular data;

Lack of a common, standardized and complete classification system: definitions of what is environmentally and socially sustainable remain fragmented across jurisdictions. Furthermore, the definitions are often ‘binary’, which might be misleading, as there are different ‘shades’ of environmentally and socially sustainable, which entangle different levels of risk;

Challenges in linking non-financial forward-looking ESG information to prudential parameters: estimating the probability of materialisation of physical risks remains a challenge and requires forward-looking information;

Challenges in the use of ESG ratings or scores: often, the methodologies backing ESG ratings are not transparent;

Complexity of analysis: the granularity of classifications for what can be considered environmentally and socially sustainable may vary across different exposure classes.

The regulator also has some issues related to time horizons. Environmental risks are forward-looking, often perceived as long-term risks, with an uncertain timing and magnitude. This creates a mismatch with the Pillar 1 framework, which was not designed to align with the manifestation of long-term environmental risks, but rather to ensure resilience to unexpected adverse circumstances, pointing rather to short- and medium-term horizon. Moreover, Pillar 1 requirements are designed to protect institutions from risks with high confidence levels that may not be achieved if longer-term horizons were to be considered.

Conclusion

Overall, the EBA does not recommend introducing environmental-related adjustment factors in regular risk metrics at this stage. The regulator considers that the Pillar 1 framework already recognises environmental risk drivers in capital requirements through certain mechanisms, like internal and external ratings, and that accounting for further environmental-related risks would most likely result in double counting.

On the other hand, the EBA does recommend, as a short-term action, that external credit ratters integrate environmental and/or social factors as drivers of credit risk whenever relevant. Furthermore, it recommends for banks, as a medium- to long-term action, to increasingly reflect environmental factors in their financial collateral valuations. Finally, the EBA notes that all the above-mentioned considerations will be re-assessed in the medium- to long-term, when more relevant, reliable and comparable data on sustainability-related matters is made available.

This article is part of the SustainaWeekly of 30 October 2023