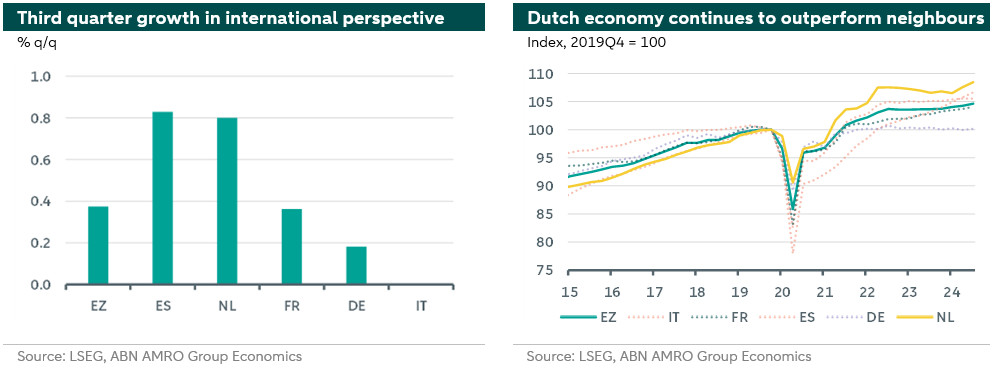

Dutch macro perspectives – Internal demand drives strong third quarter growth

The Dutch economy showed solid growth as GDP expanded by 0.8% q/q in the third quarter, mostly on the back of strong spending from households and the government. This is in line with the broader eurozone, where growth increased to 0.4%, which also looks to have been driven by increased private consumption. The strong third quarter for the Dutch economy follows an already high and still upwardly revised second quarter with 1.1% q/q. Zooming out, the Dutch economy has seen a strong half year, following a period of stagnation in 2022 and 2023.

Household consumption drives growth, recovering from decline in Q2

Private consumption rebounded (+0.8% q/q) from the large decline in Q2. Indeed, households are seeing their real incomes increase on the back of still high wage growth and lower inflation, but the spending effect was somewhat delayed as households prioritized saving and deleveraging in recent months. In the third quarter, spending growth was mostly concentrated in goods. Given the pickup in new mortgage lending and housing transactions – the latter mostly driven by first-time buyers – the housing market is also provided an impulse to goods consumption (a theme we covered in our September Global Monthly). Services consumption likely also benefited from the good weather. Public spending by the government also rose (+0.8% q/q) on the back of higher spending on health care and public administration. Increased activity in the housing market is also visible in investment, which rose by 0.7% q/q, mostly driven by higher investment in housing and machinery. The government likely accounted for a large share of the increase in investment, given the bleaker outlook for private investment.

Employment declines from its peak

With 1.06 vacancies per unemployed, the labour market remains tight, although this tightness has eased from its peak. Labour demand declined, and less new vacancies were created over the third quarter. The unemployment rate rose marginally, as there were less job finders and more job losers. Still, the number of jobs rose, mostly in public sectors like healthcare and public administration, which aligns with the rise in public spending we saw in Q3. Generally, the unemployment rate is expected to remain low in the years to come due to strong labour demand and limited labour supply, given the greying population.

On the external side risks remain

Exports rose by 0.4% q/q, which is less than the second quarter. As a trade-oriented economy, the Netherlands is significantly affected by international developments, and trade is expected to contribute only marginally to overall GDP growth in 2024. With an underperforming German economy, the Netherlands’ main trading partner, and slowing global manufacturing, the outlook for external demand remains subdued.

Growth to continue in the quarters ahead, but tariffs are a headwind in 2025-26

All in all, we expect the Dutch economy to recover further in the quarters ahead, mostly driven by internal demand. In the beginning of 2025, growth will be more broad-based, with the outlook for external demand improving as growth in the eurozone picks up further, and ECB rate cuts feed through to the economy. Then, towards the end of 2025 we expect growth to decline with the introduction of trade tariffs by the US. We are currently revising our forecasts, which will be published in the upcoming Global Outlook.