Decarbonisation strategies in Dutch sectors

ABN AMRO's Group Economics has mapped the greenhouse gas (GHG) emissions of over 30 sectors in the Netherlands. For each sector, the path for further emission reduction is highlighted. But more importantly, key strategies for companies to achieve GHG emission reductions are discussed in depth.

Decarbonisation requires hefty investments and public policy support

(complete report contains over 100 pages; for a copy in Dutch click here)

Summary

Within many of the economic sectors of the Dutch economy, the transition to a low-carbon or carbon-free pathway is now well underway. But our publication shows that some sectors are struggling, while for others, the emission reduction path towards 2030 is a viable option. The sectors responsible for most greenhouse gas (GHG) emissions face a major challenge to decarbonise their processes and products. This is an especially important task for many industry subsectors, some of which are complex and face many obstacles. However, our research also shows that there are not only numerous solutions and opportunities for GHG reduction in all sectors, but that these techniques are sometimes within reach.Decarbonisation is a term used for removing or reducing emissions of carbon dioxide (CO2) in particular. This can be achieved in several ways and the best practice decarbonisation technique varies greatly from sector to sector. For companies in one sector, switching to renewables or fuel substitution is most promising, while companies in other sectors achieve more through electrification and efficiency measures.

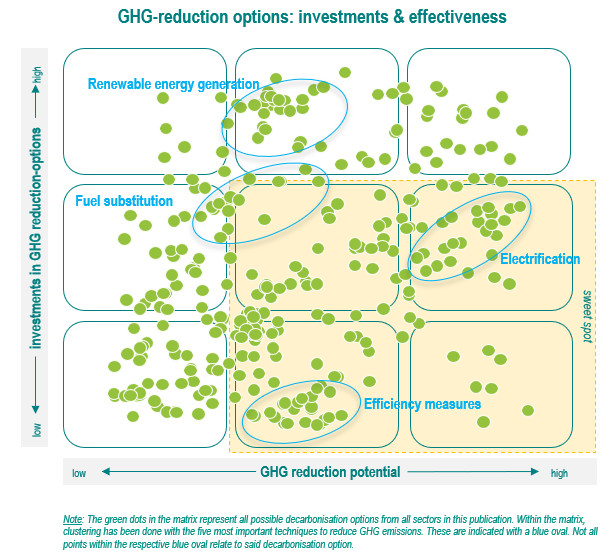

In the matrix, all decarbonisation technologies from all sectors are plotted anonymously (green dots), with on the axes investment level in GHG reduction technology (vertical) and GHG reduction potential (horizontal). This shows that there are decarbonisation options in each spectrum. Once we cluster, three decarbonisation technologies emerge that are in the so-called 'sweet spot' for several sectors of the Dutch economy. This is the position where GHG reduction potential is relatively high and investment in the technology is relatively low. These include electrification, efficiency measures and fuel substitution (renewables instead of fossil). A fourth regular decarbonisation option for various sectors is renewable energy generation (such as from solar, wind, geothermal, etc.). Unlike the previous four options, investment here can sometimes be relatively high. However, this is often actually a lot more profitable both ecologically and economically in the longer term.

GHG emissions in the total Dutch economy decreased by 16% over the period 1990-2020, or only 0.5% per year. At this rate, the 2030 target is unattainable. The question then is: can companies and governments do enough in just eight years? The answer is relatively simple: achieving the 2030 target requires a lot of money and flexible (policy) terms. And public and private efforts also need to be accelerated.

A number of the emission reduction technologies named in this publication require a lot of investment. Not only in the technology itself, but also in infrastructure, for example. A good connection to the electricity grid with sufficient capacity, for instance, is a precondition. Here, the government has an important role to play. In any case, the government is an indispensable conductor in the entire transition to net zero emissions by 2030/50. Through information, knowledge sharing, policy, subsidies and targeted investments, it can give the transition the necessary impulse. What is clear is that only with a well-orchestrated interplay between private and public institutions and strong intervention by all parties will the 2030 target be achievable in the short term.

The European Commission (EC) believes that investing in climate neutrality will ultimately bring many benefits to European economies, provided those economies fully commit to the transition. Think of improved competitiveness and prosperity growth. This means that the Dutch economy has to bite the bullet now in order to benefit from a more innovative, circular and resilient economy in the long run.

This report is an English translation of a Dutch report, which was published in November 2022.