Cooling US labour demand augurs well for Fed pivot in 2023

Steep decline in job vacancies suggests rate hikes are starting to dampen pipeline inflationary pressures.

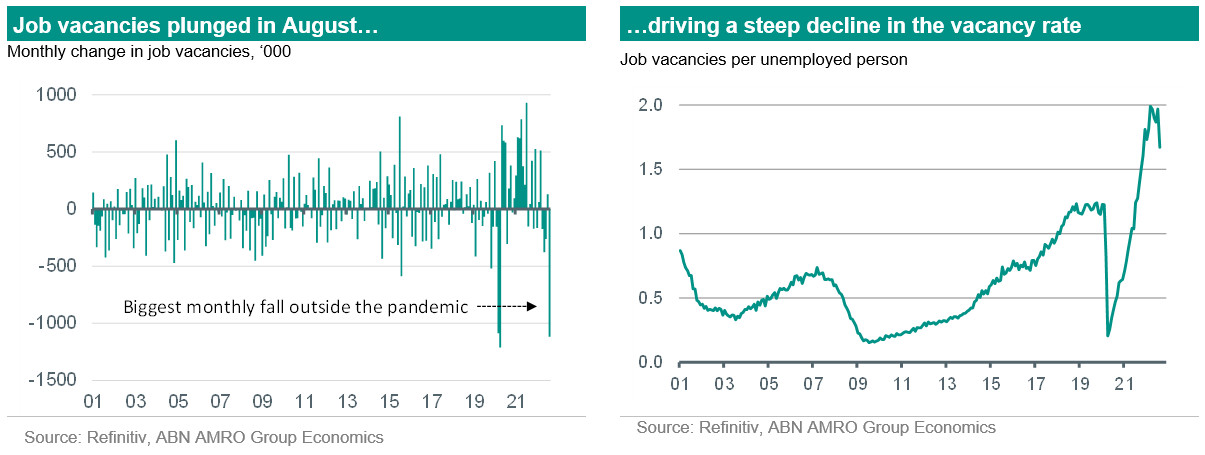

Job vacancy ratio sees dramatic fall

Job vacancies fell by a massive 1.1mn in August to c.10mn – the biggest decline in a single month outside of the depths of the pandemic period in April 2020. The decline is consistent with a softening in other indicators of labour demand, such as the PMI and ISM employment indices, as well as softening jobs growth itself (particularly evident in the household employment survey, which is less prone to revisions than the establishment survey). The decline in job vacancies, combined with the modest rise in unemployment seen in August, led to a sharp fall in the job vacancy ratio – from 2.0 vacancies per unemployed person in July to 1.7 in August. At this monthly pace, the job vacancy ratio would already be back at the pre-pandemic level of 1.2 by November. Granted, job vacancies are prone to being revised (the July data was revised up somewhat), and so the current data probably overstates the true extent of the softening in labour demand. But the weaker growth environment, driven by declines in real incomes and rising interest rates, is likely to mean a continued softening in labour demand over the coming months – our base case is for the job vacancy ratio to fall back to the pre-pandemic level of 1.2 by March 2023, and to fall further below that level in the course of the year.

Softening labour demand supports our expectation for Fed cuts in 2023

The extremely high job vacancy ratio has been a key cause for concern among Fed officials over the past year, with Chair Powell regularly citing it in post-policy decision press conferences as an indication that labour demand is out of balance with supply, and the risk this therefore poses to medium-term price stability. Given this, the significant decline in the ratio in August will surely come as a relief to FOMC members – and is a strong signal that the tightening in monetary policy is beginning to have the desired effect in terms of dampening pipeline inflationary pressure. Indeed, wage growth has already cooled from the elevated levels seen earlier this year, which bodes well for core services inflation easing in the first half of 2023.

All told, the softening in labour demand is consistent with our view that we are approaching the peak in the Fed’s hiking cycle – our base case continues to be for the upper bound of the fed funds rate to reach 4.5% in December, and to stay at that level for around 6 months subsequently. It also supports our expectation for more significant rate cuts as we move into the second half of 2023. We think by mid-2023 the Fed will have seen enough evidence that inflation is moving back to its 2% target, and we therefore expect 100bp in rate cuts in H2 23 – significantly more than the 31bp in cuts priced by money markets, and the 25bp cuts expected by the Bloomberg consensus. See our latest US macro update from the Global Monthly here for more.