China Outlook 2024 - Navigating between cyclical and structural headwinds

Beijing steps up property support; risks being shifted to banks, longer-term downsizing to continue. Support measures should help a broader recovery in domestic demand, but this may take time. Structural drags remain: we expect annual growth to fall below 5% in 2024 and 2025.

Looking back at 2023, the tailwind from the Zero-Covid exit that benefited consumer services proved insufficient to offset the intensifying headwinds from property sector woes and the slowdown in external demand. Ongoing piecemeal monetary easing and the stepping up of targeted support helped the economy to bottom out in the second half of the year, but the recovery is uneven and growth momentum remains fragile. The unambitious growth target for 2023 of 5% is within reach, but with structural headwinds remaining we expect annual growth to fall below 5% in 2024.

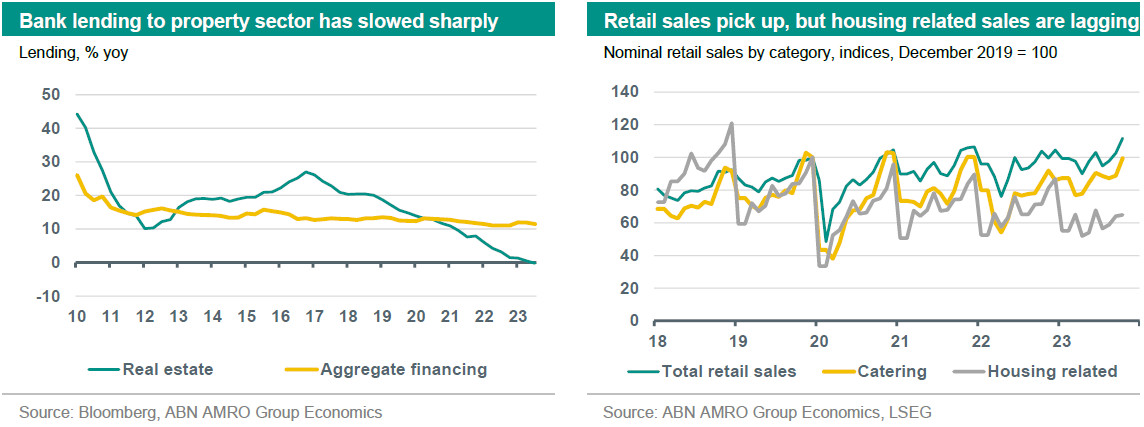

Beijing steps up support for property sector, but structural downsizing will continue while risks are shifted to banks

In the course of 2023 the property sector downturn increasingly led to systemic risks, threatening growth prospects. The stalling of new home sales added to financing problems for property developers, who already faced a retreat in bank lending. Repeated signs of distress at major developers such as Evergrande and Country Garden, rising loan defaults and signs of contagion to local governments, banks and trust funds did not help to stabilise sentiment either.

The property downturn also affected the land finance development model, in which local governments raise cash from land sales and use that to fund infrastructure projects via local government financing vehicles. As a result of all of this, Beijing was forced to change course. In the second half of this year targeted support to the property sector was stepped up materially, also to safeguard growth in 2024. Mortgage rates were reduced, downpayment requirements were eased, and state banks were asked to extend loans to ensure the completion of existing construction projects. In November, the PBoC presented a CNY 1bn lending facility to support housing renovation/affordable housing aimed at reviving home sales, and drafted a list of 50 developers eligible for special financing support including unsecured bank loans.

These measures make clear that Beijing’s pendulum is shifting again, away from containing moral hazard towards preventing systemic risks, although the longer-term goal of reducing the size of the property sector will be maintained. Recent measures also make clear that the risks are being transferred from property developers to state/policy banks, who are already facing weak profit margins and a deterioration in asset quality.

Support measures should also facilitate a broadening of the recovery in domestic demand, but this may take time

The scarring from previous stringent policies (Zero-Covid, crackdown internet platforms, three-red-lines policy in real estate) contributed to cautiousness amongst consumers and private firms (see also our October Monthly, Six urgent questions on China). During the pandemic years, China’s private consumption was lagging in the recovery, a completely different picture compared to for instance the US. Following the Zero-Covid exit, consumption has recovered to some extent, but the rebound is still concentrated in sectors that were hit the most by Zero-Covid (transportation, tourism and entertainment). Also, the auto sector has done well this year, with car sales benefiting from discounting practices and a shift towards EVs. By contrast, housing-related retail sales (furniture, decoration, construction) are still in the doldrums.

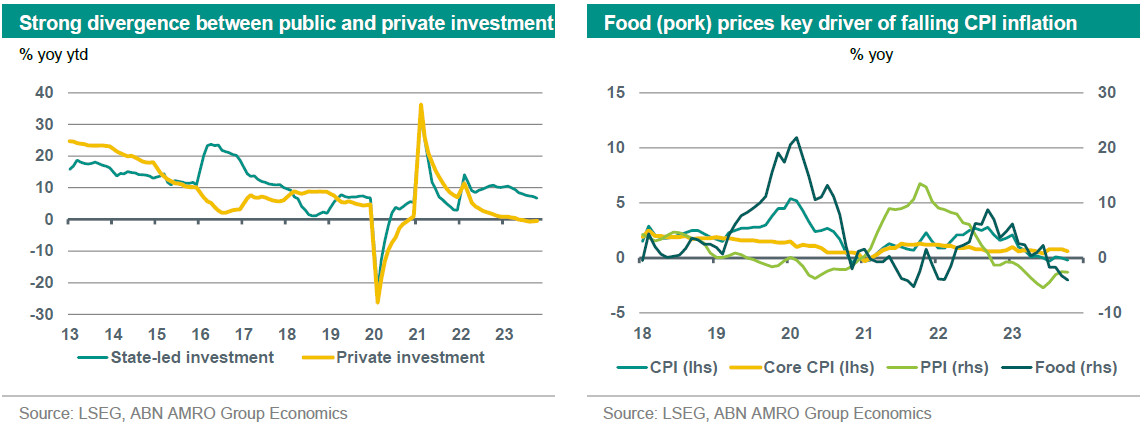

We expect the measures taken to stabilise the property sector to contribute to an improvement in consumer confidence and a broadening of the consumption rebound, but this may take time and is also dependent on improvements in the labour market and household income. Meanwhile, on the investment front, there is a strong divergence between relatively solid public investment and weak private investment, with property investment still deeply in contraction territory. Going forward, it is likely that stronger government support initiatives will lead to a re-acceleration of public investment, and help private investment to bottom out.

Exports and manufacturing should benefit from a bottoming out in the global industrial cycle next year

China’s export strength evident in the pandemic years is over, with annual export growth in negative territory for a large part of 2023. Besides base effects, this reflects the cooling of global demand on the back of sharp monetary tightening, and a post-pandemic rotation in global demand back to services. Even so, Chinese car exports have shown a remarkable surge over the past few years, and the rise of EV exports to Europe has even triggered a EU probe.

Moving into 2024, on the cyclical front we expect Chinese exports to benefit from a bottoming out in global industry and trade (with early cyclical sectors like electronics/semiconductors already showing a turnaround), although we do not expect a sharp rebound. Import growth should also recover further, on the back of the a broadening recovery in China’s domestic demand.

On the structural front, while a certain degree of tech decoupling between China and the West has become the new normal, we expect this process to remain gradual in nature given the large interests at stake. However, we see a few potential stumbling blocks (Taiwan/US elections, EU EV probe) that could accelerate this process (see global part of this report).

Deflationary spiral not likely; targeted fiscal support being stepped up alongside piecemeal monetary easing

Weak inflation prints over the past few months have added to negative sentiment, but we do not think that China is on the brink of a deflationary spiral. Food and particularly pork prices have been driving the fall in CPI inflation, but these effects will fade: we expect average CPI inflation to rise to 1.7% in 2024 from 0.3% in 2023. The drop in core inflation in the course of this year to relatively low levels is indeed partly a reflection of subdued domestic demand, but assuming a recovery in domestic demand on the back of ongoing support we expect a turnaround next year. Meanwhile, the easing of deflation in producer prices will likely continue.

All in all, from an inflation perspective, there is ongoing room for further piecemeal monetary easing, but there are constraints from weak bank profit margins (partly impacted by a policy initiative to lower rates on existing mortgages). Therefore, additional mini cuts in lending rates will likely be accompanied by cuts in deposit rates. Further cuts in bank RRRs are also likely, and we expect the PBoC to continue safeguarding bank liquidity through its lending facilities. Still, given the constraints, we expect the recent shift to targeted fiscal support to continue next year, with the focus having clearly shifted to putting an end to the distress in the property sector at the expense of state/policy banks.

All in all, we expect annual growth to fall below 5% in 2024 and 2025

All told, the Chinese economy will continue to be faced with headwinds from the structural downsizing of the property sector and related debt issues (amongst property developers, local governments, banks, trust funds). Longer-term challenges also relate to (tech) decoupling from the west, private sector confidence issues, demographics (ageing, a shrinking population/labour force), and climate change. Coupled with Beijing’s policy shift away from growth maximalisation towards goals related to national security and self-sufficiency, we expect China’s structural slowdown to continue and annual growth to slow to 4.7% in 2024 and 4.6% in 2025.

This article is part of the Global Outlook 2024