China - A new approach to stabilising property

Domestic demand side remains weak, with property sector still in the doldrums. Beijing comes with new approach to break the negative feedback loop in the property sector. Upside/downside risks still ‘in balance’: property support versus new trade spats on excess supply.

Macro data continue to show a divergence between strong supply and weak domestic demand, still dragged down by property sector woes. Beijing is trying something different now to break the negative feedback loop in property. At the same time, external risks are rising, as China’s overcapacity contributes to a broadening of trade spats with the West.

Domestic demand remains weak, with property sector still in the doldrums

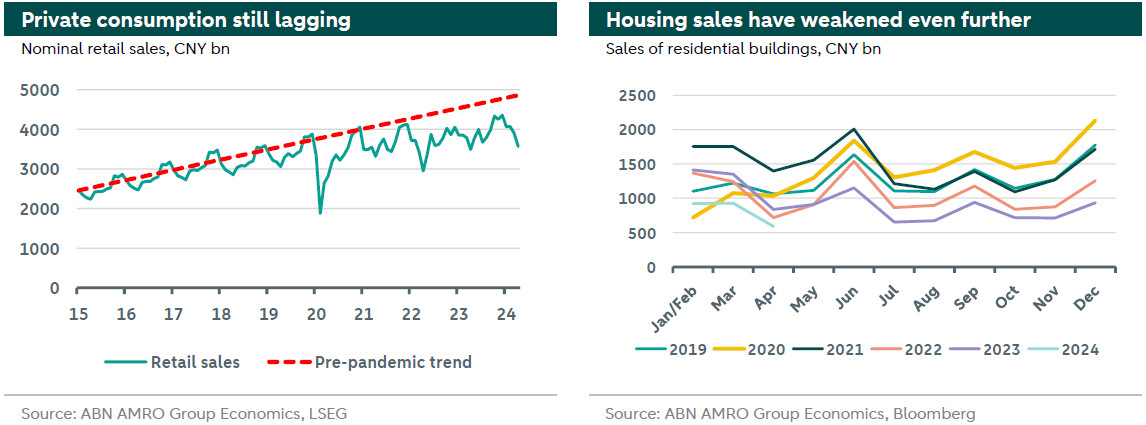

China’s April data clearly point to ongoing macroeconomic imbalances, with the supply side stronger than the (domestic) demand side and the property sector remaining the largest drag. On the supply side, industrial production growth accelerated to 6.7% yoy (March: 4.5%), and by 1.0% mom (a post-pandemic rebound high). This partly rests on improving external demand (despite trade spats), with the export components of both manufacturing PMIs back in expansion territory since March. By contrast, the domestic demand side remains weak. Retail sales slowed to a meagre 2.3% yoy in April (March: 3.1%), falling even further below its pre-pandemic trend (see chart). Fixed investment slowed to 4.2% yoy ytd in January-April (Jan-March: 4.5%), with private investment growth still very weak (+0.3% yoy ytd). April data also show that, despite all kinds of previous targeted measures, the property sector is not out of the woods yet. In April, annual growth of property investment and residential property sales (see chart) fell even deeper into contraction territory, and home prices showed the sharpest monthly drop since 2015.

Beijing’s new attempt to break the negative feedback loop in property

Earlier this month, Beijing took further measures to stabilise the stumbling property sector. Floors for mortgage rates were removed, and minimum downpayment ratios for homebuyers lowered. Moreover, the PBoC introduced a CNY 300bn (± EUR 38bn) relending facility, through which local SOEs can buy completed, unsold property from developers and turn these into affordable housing. And another CNY 500bn (± EUR 64 bn) – aimed at urban reconstruction – will be made available through the Pledged Supplementary Lending facility. In addition, by means of special bonds, local governments are entitled to buy land from developers. The idea of these measures is to mitigate the financing distress of property developers, so that they can focus on the completion of projects. That should bolster confidence amongst potential homebuyers, and boost new home sales. That said, the facilities are small compared to the total outstanding stock of unsold homes, and there are many implementation issues and trade-offs at local government levels. While it is uncertain whether these measures will bring a ‘quick-fix’, they signal Beijing’s increasing sense of urgency to tackle the biggest domestic drag to the Chinese economy, while (implicitly) supporting developers. All told, it remains to be seen whether this will be enough to break the negative feedback loop; if not, more targeted support will likely follow. All in all, we leave our growth forecasts for 2024 (5.1%, slightly above consensus) and 2025 (4.5%) unchanged for now. We still think risks to our growth forecasts are more or less balanced at the moment, as ‘upside risks’ from (more) property support are being (partly) offset by downside risks from the broadening of trade spats – with the US and the EU taking additional measures to shield their (strategic) industrial sectors from Chinese oversupply (also see here and here).