Central banks caught between a rock and a hard place

Global Macro: Raising the probability of more negative scenarios – We saw a significant further escalation in sanctions against Russia over the weekend, including a partial ban on use of the SWIFT payments system, and the freezing of Russian central bank assets. As yet, it appears the goal of sanctions is still to avoid disruption in gas supplies to Europe, with attempts at a carve-out for the energy sector.

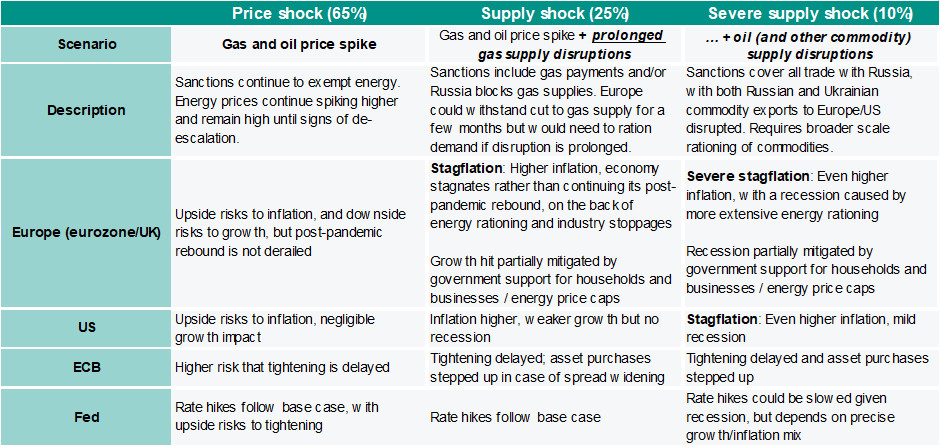

However, given how quickly tensions between Russia and the west have escalated, we see a higher likelihood of supply disruptions than we did previously. We have therefore raised the probabilities of more negative scenarios playing out, and now peg the risk of gas supply shortages in Europe at 25% (previously 20%), and of more widespread commodity shortages – not just from Russia but Ukraine itself – at 10% (previously <5%). We have correspondingly lowered the probability we attach to our baseline scenario of a price shock which eventually dissipates once the conflict de-escalates, to 65% from 75% previously. See table below, and our publication of last Friday, for more on our macro scenarios. In this Daily Insight, we give our views on how we think the ECB and Fed will respond to the evolving conflict.

ECB: Focus may shift to demand fall-out as the crisis escalates

The Russia-Ukraine crisis could make the ECB less hawkish, even though it will significantly add to price pressures in the near term. For the time being it seems, the Governing Council is still minded towards tapering its net asset purchases. At the same time, there is an even greater need now for the ECB to maintain optionality and stress flexibility in its communications. However, as the crisis extends and perhaps intensifies, the ECB’s focus may shift more and more to the demand fall-out.

Traditionally, a central bank should only tighten in the face of supply-driven inflation if the initial price spike leads to (or risks leading to) second round effects, in terms of the impact on non-energy prices and wages. However, the demand fall-out from this crisis reduces the risks of second round effects and indeed could point to lower inflation over the medium term. Declining household purchasing power, a squeeze on company profits, tighter financial conditions and the hit to business and consumer confidence will hurt growth. In the more negative scenarios, we could see a recession. As such, the crisis has increased the chances the ECB’s exit will be slower or even that it will put an ice. In addition, in the more negative scenarios, the central would likely turn from exit to additional policy easing.

Fed: High inflation and limited growth impact leaves little room for rowing back

Fed officials have so far been quiet on the impact of the Russia-Ukraine conflict, and have continued to emphasise the upside risks to inflation as the key concern facing policymakers at present. At the same time, market pricing of Fed rate hikes has only retraced modestly, with around 140bp in policy tightening priced in to December (i.e. 5-6 25bp hikes), down just 6bp from 7 days ago, before the conflict broke out. As we have previously described in our macro scenarios, the US economy is much more insulated from the impact of potential disruptions to Russian commodity exports.

The US is largely self-sufficient when it comes to energy. While there would be some impact from higher energy prices in more negative scenarios, these would have a bigger upward impact on inflation than they would a downward impact on growth. As such, the growth/inflation mix in the US will still likely favour a significant tightening of monetary policy. In our base case, we continue to expect the Fed to raise rates four times this year, with a significant risk that the Fed needs to tighten more. In the supply shock scenario, the risk around this forecast becomes more balanced, given the confidence effects of tighter financial conditions and the spillovers from a weaker eurozone economy. Only in the most negative scenario of more severe widespread commodity export disruptions might the US economy be pushed into a mild recession. Even then, the boost to inflation in an environment of already elevated inflation expectations will make it hard for the Fed to slow down its policy tightening, let alone ease monetary policy. (Bill Diviney, Nick Kounis, Aline Schuiling)