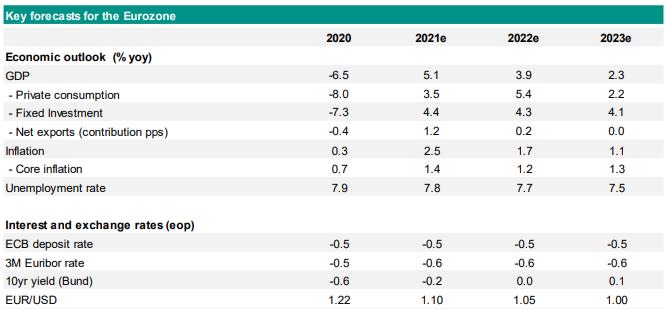

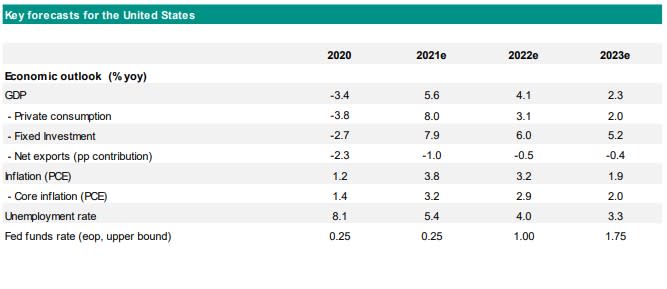

Central banks and markets Outlook 2022 - Fed policy tightening to leave its mark

The Fed is set to speed up its tapering of asset purchases and embark on a significant rate hike cycle. Its tightening is focused on getting ahead of an inflation problem, which makes this time different . The ECB faces different macro conditions and will keep policy accommodative, while ending the PEPP. US Treasury yields will rise significantly, especially the short end, leading to curve flattening. Euro yields will be pulled up modestly by the US move; Policy divergence will see EUR/USD decline. Omicron is unlikely to trigger new stimulus, unless financial conditions tighten severely

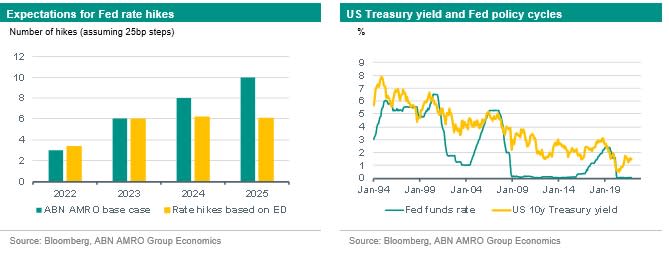

Fed will go faster than markets currently expect

Against the background of a broadening rise in inflation, consumer goods spending that has sky-rocketed, subdued labour supply and rising wage growth, the Fed will likely remove accommodation at a faster rate. Although the Fed has set out a timetable for tapering asset purchases at a gradual pace through to June, it seems likely that it will shorten the taper period to March. This will set up an early start to a rate hike cycle. With the Fed having already met its average inflation goal, and the labour market likely at full employment, we judge that the Fed will start to hike the fed funds rate in June 2022. In total, we expect the Fed to raise the fed funds rate three times in both 2022 and 2023. Thereafter, we expect a more gradual pace of two hikes per year, until the fed funds rate reaches 2.50-2.75% by the end of 2025. This is around the FOMC’s neutral rate estimate of 2.5%. The graph below shows the cumulative number of rate hikes we expect in our base case, and what market expectations are based on Eurodollar futures and the US swap curve. As can be seen, our base case is for faster and more significant Fed rate hikes, especially 3-4 years ahead.

US Treasury yields will rise as markets price in a higher terminal rate

An important driver for the 10y US Treasury yield is expectations for where the Fed’s policy rate will ultimately be 3y ahead. Indeed, the 10y US Treasury yield has a very high correlation with the 12th Eurodollar position, whereas the 2y US treasury yield has a very high correlation with the 4th Eurodollar position as shown in the graphs above. Given that we forecast the Fed funds rate to be at its eventual peak of around 2.50-2.75% by end 2025, we expect longer term yields will move higher in 2022, with the 10y US Treasury yield settling at around 2.6% at year-end. In previous cycles, the 10y US Treasury yield also settled around the eventual peak in the Fed funds rate, although well ahead of that time. Once we move closer to the first rate hike, which we have pencilled in for mid-2022, we expect the US Treasury curve to bear flatten. We expect this will be most pronounced in the 2s10s and 2s30s area of the US Treasury curve, as was also the case in previous rate hike cycles.

ECB to keep policy more accommodative, with divergence weighing on the euro

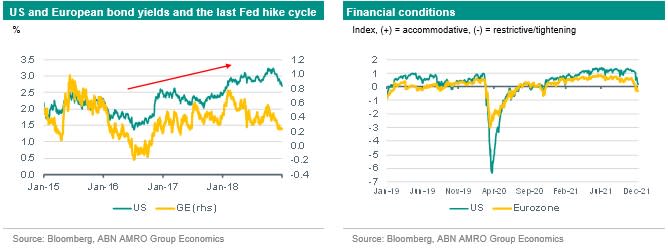

The expected tapering and rate hikes by the Fed and the resulting rise in US Treasury yields should also put some upward pressure on their European counterparts. The divergence between US and eurozone rates is expected to put downward pressure on the euro, which would raise eurozone growth and inflation, all other things being equal. Nevertheless, we think that the euro area is facing a different set of macroeconomic circumstances compared to the US. The rise in eurozone inflation is much more narrowly based, wage growth is subdued and consumer demand is much weaker than in the US. Indeed, we expect an output gap to remain in the eurozone at the end of 2022, despite growth at around 0.7% qoq in 2022, which is well above the trend rate. Therefore, underlying inflationary pressures will remain weak. In combination with the ECB’s new inflation framework, this suggests that policy will remain easier for longer, with purchases under the APP continuing and policy rates remaining on hold during the coming years. Based on our growth and inflation forecasts and considering the fact that the ECB is likely to start hiking the deposit rate 12 to 18 months before it reaches its inflation goal, we judge that an ECB rate hike cycle is still some years away. This points to a significant policy divergence between the Fed and ECB over the coming years, which will see the euro decline significantly against the dollar.

Tug of war in Europe could lead to Bund volatility

Nevertheless, a sharp rise in Treasury yields will also leave its mark on Euro rates. Indeed, this is what we saw during the previous Fed rate hike cycle, despite the ECB remaining on hold. Technicals also become somewhat less favourable. Given the end of the PEPP, we expect higher net adjusted supply of government bonds in 2022 compared to 2021. Overall, we expect longer term yields to move higher, while short term yields are expected to move sideways. This would result in a bear steepening of yield curves in the euro area. Our baseline is for a 10y Bund yield of around 0% at the end of next year, though we could see more significant spikes in between, given a tug of war between the upward pull from the US and a dovish ECB. Despite lower asset purchases overall, the APP will have an important role in this story. We expect the ECB to remodel the APP into an envelope that can be used flexibly to fight against financial conditions tightening too quickly.

Omicron a downside risk to growth but could even be an upside risk to inflation

Investors are digesting what Omicron means for the monetary policy outlook. We have not factored Omicron into our economic, central bank or market forecasts at this stage. However, our current thinking is that central banks will not react to Omicron by easing policy aggressively or even at all. We still think that the Fed is heading for monetary tightening. The ECB will also keep to its previous course of ending the PEPP, while maintaining optionality as well as accommodation via its other instruments. Our unchanged outlook for central banks reflects that the starting point compared to Covid I is different in terms of the supply side and inflation, and Omicron could prove to be at least as much a supply shock as a demand shock (see previous chapter on how Omicron might impact the economic outlook). We do think that a very sharp tightening of financial conditions would be the game changer for central banks, though we are currently nowhere near close to that at this point. (Jolien van den Ende, Bill Diviney, Aline Schuiling & Nick Kounis)