Carbon Market Strategist - Market is stable as the heating season approaches

EUA prices witnessed a decrease since August as risks of supply disruptions for European gas subdued. Allowances demand from main sectors remains low on the back of high renewable energy output and weak industrial recovery. The market may still witness a temporary surge in demand around the coming surrender date… But the bearish sentiment is still dominating the market with the current supply surplus. Our outlook for October is neutral, where we expect the EUA price to range between 62 and 68 €/tCO2.

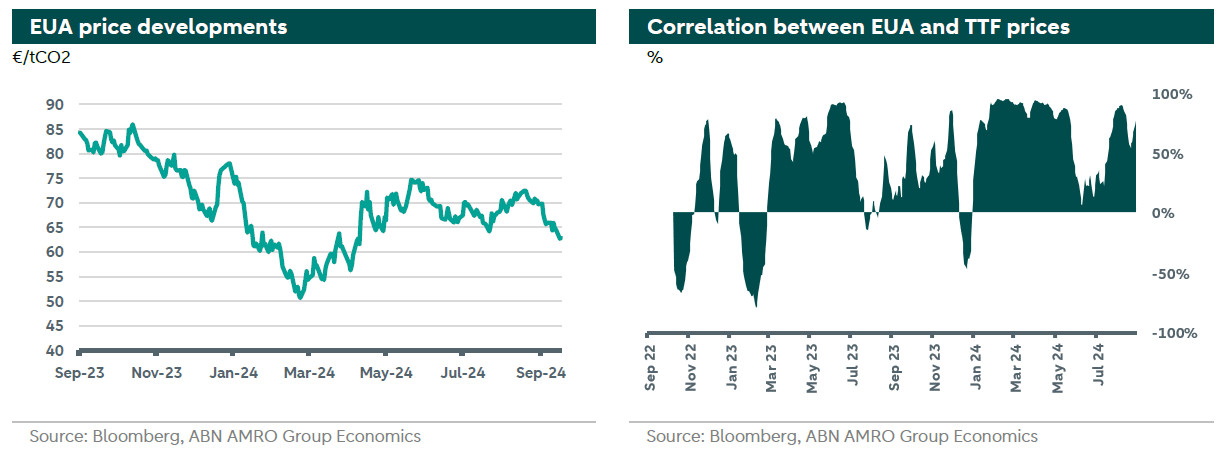

EUA prices averaged 68.8 €/tCO2 since the beginning of August. The market witnessed a downward trend last month as fears of supply disruptions in the gas market weakened following a subdued geopolitical uncertainty. Demand from main sectors remains weak because of reluctance in economic recovery, mild weather, and high renewable energy output. The bearish sentiment is still dominating the market, while speculators show less interest in participating in it. EUAs are trading around 64.9 €/tCO2 at the time of writing.

EUA price drivers

EUA prices remain highly driven by European gas prices. The correlation stems from the role that gas plays in power markets, where gas is the main marginal fuel determining power prices, and its price further determines whether coal power plants are dispatched or not. The EUA and TTF (European gas) correlation stays at high levels (above 54% most of August and early September), as shown in the right hand chart below. Gas markets have been witnessing some relief as fears of supply disruptions from main suppliers (Norway and the US) dissipated and Geopolitical uncertainty subdued.

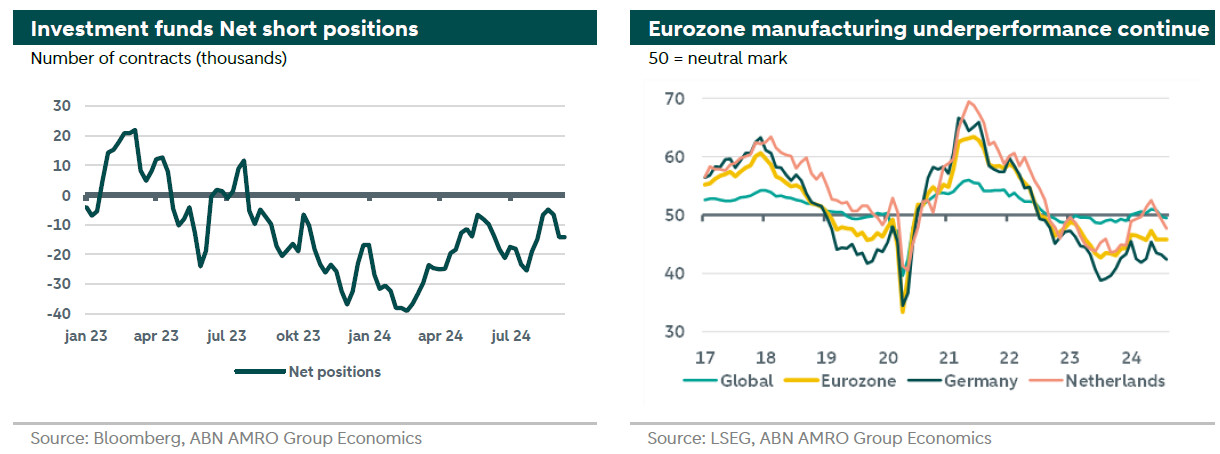

Demand from industry also remains weak. The Eurozone manufacturing sector is still an underperformer (manufacturing PMI was stable at 45.8 in August), with Germany’s PMI falling back to a five-month low of 42.4, as illustrated in the right hand chart on the next page. That being said, also the French PMI is at low levels (43.9), while the index for the Netherlands has fallen back by almost five full points since May, to an eight-month low of 47.7 (see more in our note here).

So far, the coming surrender date on the 30th of September has not yet induced a noticeable increase in demand. This could be explained by the relatively low 2023 emission levels from both power and industrial sectors, and a forward looking behaviour by covered installations, which bought their allowances in advance of the deadline. However, there might be still the possibility of a surge in demand around the surrender date, inducing a temporary rise in EUA prices.

From the supply side, the market is experiencing a surplus driven mainly by the front-loading of allowances to fund the REPowerEU packages and the additional allowances put in the market following the extension of EU-ETS to the shipping sector. Accordingly, the total supply of permits for the year is shrinking by just 1%, which is way lower than the linear reduction factor of 4.3%. We note that the current frontloading implies that stronger reduction in circulated permits is expected between 2025 and 2030. This, in turn, indicates that higher EUA prices can be expected coming years.

Open interest has been witnessing a decline recently, reflecting a reduction in speculation in the market. All in all, market sentiment is still bearish on the outlook for EUA prices as illustrated in the left hand chart below where net short positions by investment funds have been dominated by short contracts.

Outlook

Given the above mentioned developments, we think that market fundamentals are stable in the coming month, while prices will remain responsive to geopolitical developments affecting the gas market. As we approach the heating season, weather conditions become more relevant to the carbon market through their impact on renewable energy output and gas demand. We further expect that a recovery in demand from the manufacturing sector on the back of central bank rate cuts will take more time to gain momentum. Accordingly, our outlook for the EUA price in October is neutral, where we expect the EUA price to range between 62-68 EUR/tCO2.