US - Powell shapes the present, Trump holds the future

Headline macro data returns to goldilocks’ ‘just right,’ just before Trump returned to office. Disinflation to resume; labour market not out of the woods yet. Rate cuts possible and likely in the first half of 2025; second half determined by Trump policy.

President Trump officially entered the White House this Monday, following a notable two-month transition period since his election. In his first days in office, he has signed numerous executive orders, focusing predominantly on immigration, fossil fuels and government HR policy. As the new administration begins, fresh fiscal policies are causing reverberations, but recent data by itself is enough to offer a new perspective on the U.S. economy. The combination of fiscal, and especially monetary policy, over the last four years, saw an economy with continued strong momentum, and an quasi-victory over inflation. The closing month of President Biden’s term saw an inflation report consistent with the 2% target and a seemingly robust labor market. What implications do these developments hold for the economy, the Federal Reserve, and President Trump?

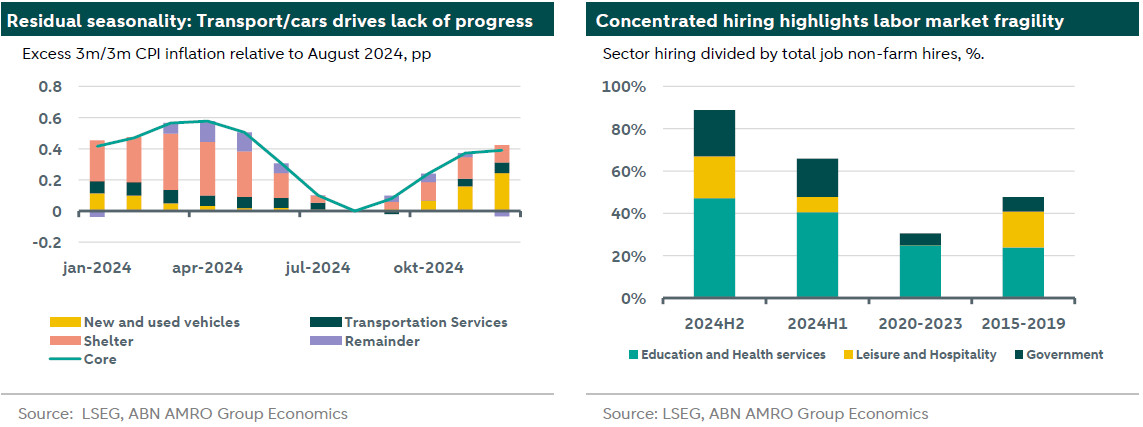

While the December CPI report was surprisingly benign, inflation has resurfaced since the start of the easing cycle. The 3m/3m inflation rate highlights that excess inflation - defined as the component’s rate above to its 2015-2019 average - is predominantly concentrated in the transportation sector. Excess CPI inflation also has a large shelter component, which is notably smaller in the PCE measure due to lower weighting. We are optimistic that disinflation will continue its December impulse in the first half of 2025. Even though shelter inflation has increased again from its August low, it is still significantly lower than in the first half of 2024, and indicators like those from Zillow showing no renewed pressure and even a decline towards the end of 2024. Residual seasonality contributed to the rise in transportation inflation, but we anticipate it will exert a dampening effect in the early months of 2025. Consequently, we expect disinflation to continue at the onset of Trump’s presidency—a development he might claim as a victory.

Our view on the labour market remains less optimistic. While the latest report was strong, the overall trend remains a source of concern. Non-farm payrolls are scheduled to be revised down significantly in the January report, slated for release on February 7th. Moreover, hiring over the past year has become increasingly concentrated, with nearly 90% of employment gains in the latter half of 2024 stemming from just three sectors, which collectively constitute only 42% of total employment. Government, education and health services are noncyclical, while job creation in leisure and hospitality is not necessarily a sign of a strong economy, but rather a consequence of the broader trend towards services consumption. Other sectors have seen minimal hiring, presenting a different picture of U.S. economic dynamics compared to the headline figures. This concentration increases vulnerability to negative shocks, particularly given expectations that government hiring is likely to contribute less positively under the new administration.

Last week we outlined a revised path for the federal funds rate. Inflation data in the last quarter of 2024 was a bump on the path to 2%, but we expect disinflation to resume in the first half of 2025, giving the Fed room to consider easing rates further. We expect the fragile labour, with an overall downward revision, and a number of poor reports to feed concerns about the employment side of the mandate, leading to one or two more cuts by the Fed. In the second half of the year, Trump policy is likely to start to push the economy in a different direction. The tariffs are expected to provide an inflationary impulse, pushing rates up, but changes in immigration policies, and abrupt shifts in federal hiring practices could significantly impact the labour market, pulling rates down. Trump inherits an economy with strong momentum that continues to exceed expectations. The path for his proposed policies to have a positive impact on the economy is narrow, while the downside risks are large. Trump holds the future, but he must navigate carefully to preserve its, and his, promise.