US: Labour market points to some easing in inflationary pressure

Upside risks to inflation remain significant, which will keep the Fed hiking aggressively this year. However, there are tentative signs of an easing in medium-term inflationary pressures. Inflation will still be a major challenge, but provided these trends persist, it might well be peaking.

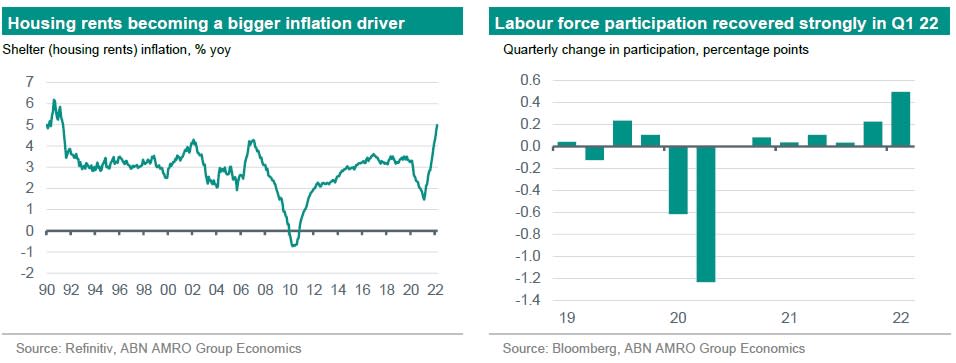

Inflation continues to be by far the biggest risk to the outlook. In March, we had another uncomfortably high inflation reading, with the passthrough from higher gasoline prices pushing headline inflation to a new four decade high of 8.5% y/y. Gasoline prices have eased a touch in recent weeks, tracking the move in global oil prices, and suggesting we may have seen the peak in headline inflation, provided we do not get a renewed sharp rise in commodity prices. The bigger medium term risk continues to come from core inflation, which strips out volatile food and energy components. Core inflation decelerated from recent readings, with prices rising 0.3% m/m compared with 0.5-0.6% rises in the five months prior. However, the details were less encouraging: services inflation accelerated, driven by continued sharp rises in housing rents, alongside a rebound in medical and transportation inflation. This was offset by a decline in used car prices, which was expected given that demand for cars is finally cooling. In our view, the bigger story here is the rise in services inflation, which tends to be much stickier and harder to bring back down once it has accelerated. Alongside continued near-term pipeline pressures in the form of exceptionally high producer price inflation, this will keep pressure on the Fed to raise rates sharply over the coming months. We continue to expect two 50bp hikes in May and June, followed by 25bp hikes in each subsequent meeting until the fed funds rate reaches 2.50-2.75%, in early 2023 (from 0.25-0.50% currently).

A major driver of services inflation – in particular housing rents – is the labour market, and it is here that we had some more positive news. While employment continued to grow robustly in March, with 431k jobs added and unemployment falling to 3.6%, participation in the labour market also continued to rise, with wage growth showing some signs of moderation (on a 3m/3m basis, wage growth cooled to 5.1% annualised from 6.1% in January). For the first quarter as a whole, labour force participation rose by half a percentage point – the biggest rise since the pandemic began. The recovery in participation has been stronger than we expected, with ISM surveys reporting that the easing of the Omicron wave is improving the availability of labour. Indeed, surveys for both manufacturing and services quote hiring managers as saying they are finding it easier to source staff than before. While labour force participation is still some way short of pre-pandemic levels (by around one percentage point), the unexpectedly strong improvement is encouraging for the medium term inflation outlook.

Further comfort can be drawn from an easing in other domestic supply-side pressures (see this month’s Global View), as well as declining goods consumption. March retail figures suggest a continued real-terms fall in goods consumption, once adjusting for inflation, although in level terms retail sales remain around 3pp above trend. Falling goods consumption is consistent with the sharp declines in consumer confidence, itself likely a result of the significant hit to real incomes, which as of March have fallen c.5% from their May 2020 peak as a result of high inflation. Thus, while the US is nowhere near out of the inflationary woods, to some extent at least, inflation could still prove to be a self-correcting problem.