US - Is inflation heating up again? We think not

Activity and jobs growth have slowed to a more trend-like pace in recent months. A couple of hot inflation prints have reignited market doubts over the disinflation path. We see little reason to think this will persist; on the contrary, pipeline price pressures remain benign. We continue to expect the Fed to begin lowering rates from June.

The US economy continues to grow at a more trend-like pace, after backward revisions suggested activity slowed more sharply in January than preliminary data suggested. Both retail sales and industrial production modestly increased in February, but this followed deeper contractions in these measures in January. Meanwhile, jobs growth remained strong in February at 275k, but January’s blockbuster 353k reading did after all prove to be a mirage, as it was revised sharply lower to a 229k rise. Below the surface, the labour market is showing some signs of weakness, with for instance the hiring rate now below the pre-pandemic level, while the household survey shows a slight rise in the unemployment rate. But big picture, we think the labour market is continuing to normalise rather than weakening in an alarming manner.

Indeed, financial markets appear more worried about inflation than about downside risks to the growth outlook. Near-term market-based measures of inflation expectations have risen sharply since the start of the year, and markets now expect three rate cuts from the Fed this year, compared to almost six cuts back in January (we continue to expect five rate cuts). Inflation in January-February did come in on the firm side, although this followed some especially weak readings at the tail-end of 2023. The core CPI, for instance, rose 0.4% m/m in both January and February, which is around double the normal rate of price growth (though still far below the 0.7-8% readings at the height of the inflation surge). We did not see anything in the reports to suggest these firm inflation readings would persist. The strength was driven by three main factors: 1) pass-through from the recent jump in oil prices to some core components, such as airfares; 2) lumpy pass-through of earlier rises in housing rents; 3) possible residual seasonality in the m/m data (as Fed Chair Powell also ).

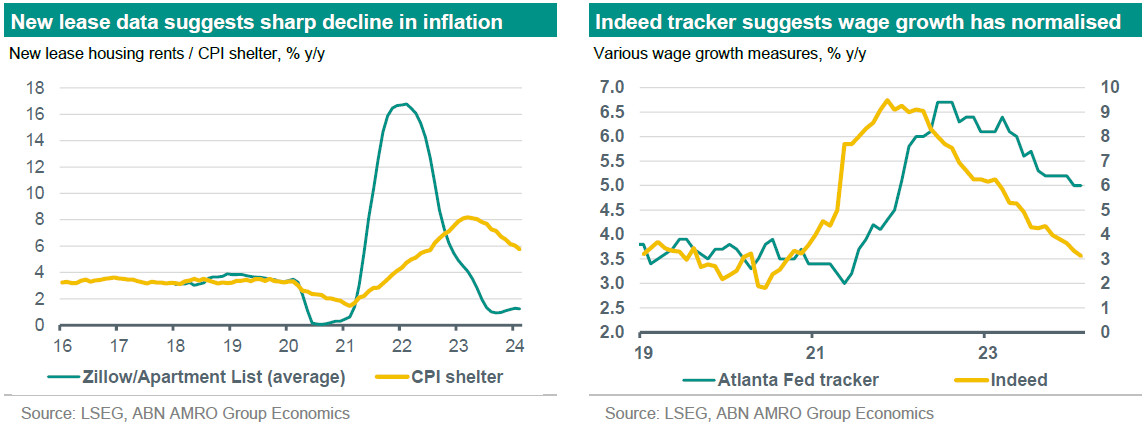

The bottom line is that pipeline price pressures still point to significant disinflation to come, especially from housing rents, with rents for new leases growing at rates below the pre-pandemic trend already for the past half year. This takes time to feed through to inflation, with past relationships suggesting a lag of around one year. The other key pipeline pressure is wage growth, but this also looks relatively benign: February’s average hourly earnings rose just 0.1% m/m, while the Indeed monthly tracker for job switchers showed wage growth of just 3.1% y/y – back in line with the pre-pandemic norm, and the lowest reading since September 2020. The Atlanta Fed wage tracker is still a little on the high side, but this indicator is very lagging. Inflation is forecast to be somewhat higher in the near-term (see forecast table at the end of this publication), but this largely reflects the earlier rise in oil prices than we anticipated; our year-end forecast for inflation is essentially unchanged. With disinflation in our view very much on track, we therefore think the Fed remains on course to start lowering rates from June. See our latest for more.