US inflation stays firm, even as recessionary forces build

Inflation remained elevated in April, even as weakening credit conditions point to a looming recession

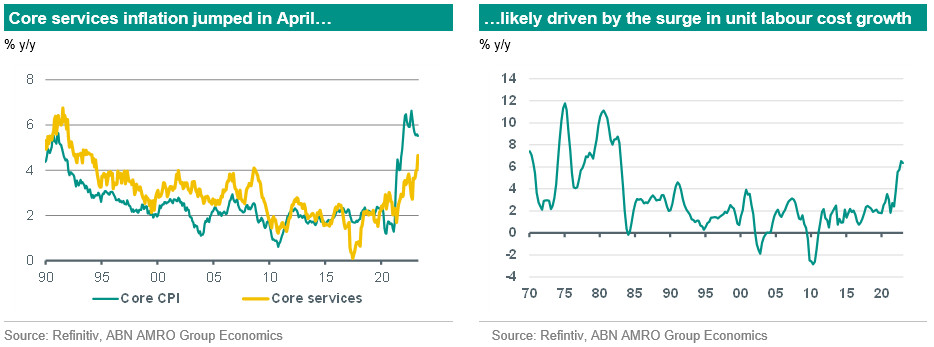

Both the core and headline CPI rose 0.4% m/m in April – still double the pre-pandemic pace of monthly price growth. This left annual inflation just a tenth lower than in March at 4.9% y/y for headline inflation and 5.5% for core inflation. Looking at the details, shelter inflation showed the first sign of cooling following nearly a year of extremely elevated readings, with the pass-through from the jump in housing rents during the pandemic beginning to recede. Offsetting this was a rebound in used car prices – and more important for the medium-term inflation outlook – a jump in core services inflation (which excludes shelter, medical and transportation services) to a new three decade high of 4.7% y/y, up from 4% in March. The rise in core services inflation likely reflects pass-through from the surge in unit labour cost growth over the past half year, and this poses risks to the medium-term inflation outlook given that services inflation tends to be more sticky.

All told, we expect inflation to remain on the high side for the next couple of months, and although inflation is expected to fall, we see a significant risk that high labour cost growth keeps inflation at a persistently higher level than the Fed’s 2% target. We therefore expect the Fed to remain open to further rate hikes over the coming months, depending on how the data evolves, although our base case is that the Fed will keep rates on hold at the current 5.00-5.25% range.

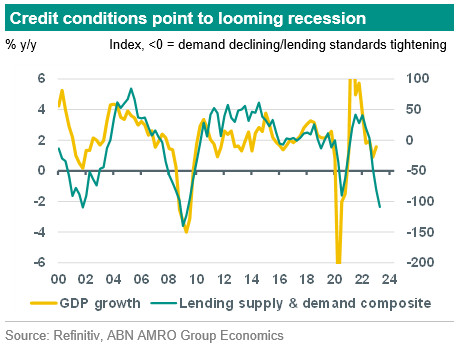

Credit conditions point to looming recession

Against the still-inflationary backdrop, recessionary forces have continued to build. The Fed’s Senior Loan Officer Survey (SLOOS) for Q1 was released on Monday, and showed a more pronounced tightening in lending standards on the part of banks, as well as declines in loan demand on the part of businesses. Lending standards have now been tightened for four consecutive quarters, while demand for credit has contracted for three consecutive quarters. Our composite credit supply/demand indicator is now weaker than the pandemic trough of Q2 2020, and the lowest it has been since the height of the Great Recession in Q2 2009. As we describe in our April Global Monthly, the SLOOS is a strong leading indicator for GDP growth, and the Q1 readings suggest that if anything, the coming recession could be deeper than we currently forecast. Based on the historic relationship, and excluding the extreme swings of the pandemic, it suggests GDP growth will fall to around -2% y/y, whereas our forecast trough in GDP growth is -0.4%.