US inflation has peaked; downtrend to continue

Core inflation surprised once again to the downside in November, with the index rising 0.2% m/m, and headline inflation also came in lower than expected at 0.1% m/m. This took annual core inflation down to 6% y/y from 6.3% in October, with headline inflation dropping even more sharply, to 7.1% from 7.7% – an 11 month low.

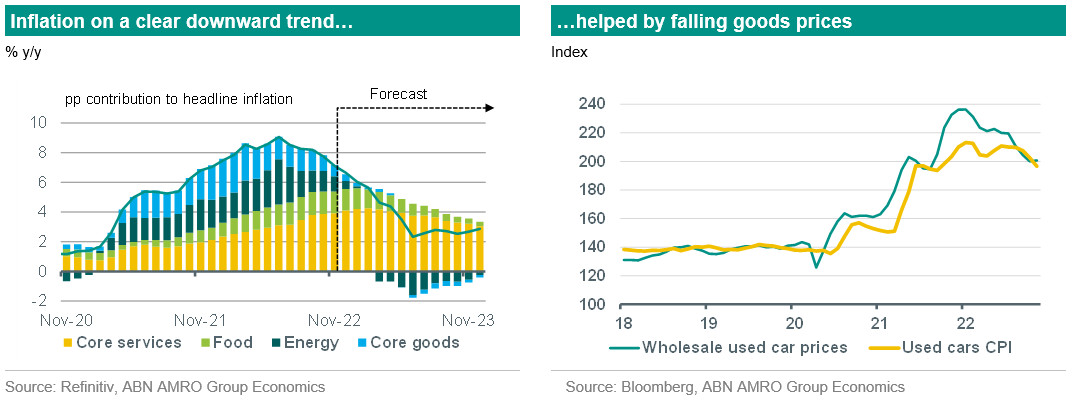

Pipeline inflationary pressures have eased significantly over the past few months, and that is increasingly visible in core goods inflation, which posted another m/m decline in November (-0.5%), once again driven by falling used car prices. Services inflation has also eased, although this has largely been on the back of a significant decline in the medical services index, which reflects a statistical quirk related to the pandemic, as well as pass-through from lower oil prices to airfares. Other services components (for instance recreation, eating out), as well as shelter (housing rents) remain elevated and are likely to stay so for the near term.

Falling inflation supports our call for significant Fed rate cuts in late 2023

While there may be some temporary factors flattering inflation at present, there has been a clear trend change in US inflation over the past few months, and we expect this downtrend to continue. The rolling over in a range of commodity prices and other supply side pipeline pressures – coupled with cooling demand – should mean a continued drag from goods disinflation (and occasional deflation) over the coming months. This will give the Fed ample reason to continue slowing the pace of rate hikes and to ultimately stop raising rates following the expected March hike. However, the Fed will also need to see a further cooling in labour market conditions to be convinced that risks to the medium term inflation outlook have receded. We expect unemployment to begin rising in earnest from early 2023 onwards, and for this to drive a fall in wage growth and in turn core services inflation as the year progresses. This is a key underpinning for our counter-consensus call for significant Fed rate cuts in late 2023. See our and our publications for more.