US GDP strength won't last

The US economy has been unquestionably strong, but the strength in Q3 is exaggerated by one-off factors. Volatility in GDP growth is the norm, historically speaking, and we expect significant payback in the Q4.

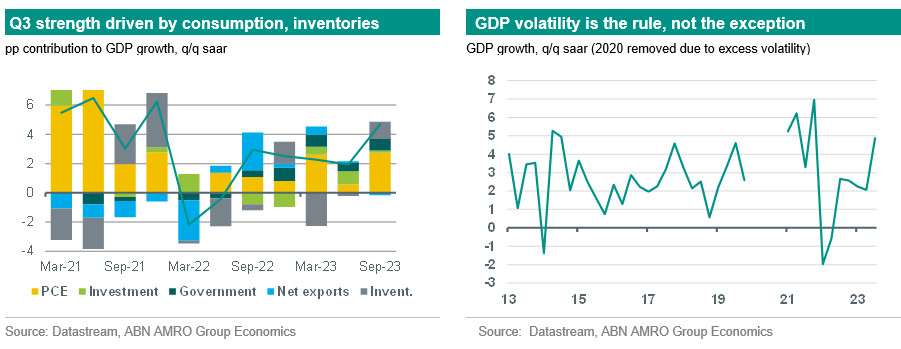

US economy is doing unquestionably well, but Q3 strength is exaggerated

Q3 GDP came in stronger than expected at 4.9% q/q annualised, above our (4.3%) and consensus (4.5%) forecasts, and well above the trend growth rate of around 2%. The bulk of the strength was driven by private consumption, which grew 4% and added 2.8pp to growth, but significant contributions came from higher inventory accumulation (+1.3pp) and government spending (+0.8pp). This more than made up for the notable weakness in fixed business investment, which registered a flat reading on the quarter. While the strength of consumption is a clear and unquestionable bright spot for the economy, the weakness in investment shows the economy cannot entirely avoid the impact of tighter monetary policy, and at least to some extent is likely down to reduced credit flows – and this is even before the recent jump in bond yields. Meanwhile, government spending has been higher than expected for much of the past year (driven in Q3 particularly by higher defence spending), and is expected to remain relatively high in level terms for the time being. However, spending is unlikely to continue growing at the current very elevated rates.

Q4 slowdown still likely, with high likelihood of a negative quarter…

Strong growth in one quarter says little about what is likely to occur in the next quarter, and that applies especially to GDP which is highly volatile at the best of times (and even moreso in the post-pandemic world). As such, we expect significant payback in Q4 following the exceptional strength in Q3, with a high likelihood of an outright decline in GDP. First and most importantly, the strength in consumption looks unsustainable in light of headwinds from falling wage growth, the oft-cited student loan repayment restart, and tighter credit conditions (which are now pushing loan delinquencies higher, albeit from relatively low levels). Jobs growth also looks set to come down, with continuing jobless claims moving higher again following a period of declines; this is more consistent with more qualitative evidence from the Fed’s Beige Book of a significant cooling in the labour market (and is out of kilter with the apparent strength in September’s payrolls report – see here for more). Second, the large positive contribution from inventories is likely to go into reverse and to subtract from GDP in Q4. Finally, the recent jump in bond yields represents a significant tightening of financial conditions that is likely to drive renewed weakness in housing and fixed business investment.

…but strong buffers are shielding the economy from rates impact

With that said, while we continue to expect a slowdown in the economy, the recent (and significant) upward revisions to disposable income and excess savings in the BEA’s updated national accounts data suggests that households have even bigger financial buffers than we thought, and this is likely shielding them to some extent from the pain of higher rates. This helps explain the resilience we have seen in the economy so far, despite the unprecedented jump in interest rates of the past two years. We are currently reviewing our growth scenario ahead of our Global Outlook 2024 and will communicate our updated view in the coming weeks.