US core inflation remains stubbornly high

Core inflation for March was in line with consensus expectations at 0.4% m/m, but below our forecast (0.5%). The strength in core inflation was driven by continued pass-through of housing rents to the shelter component as well as a pickup in core goods inflation.

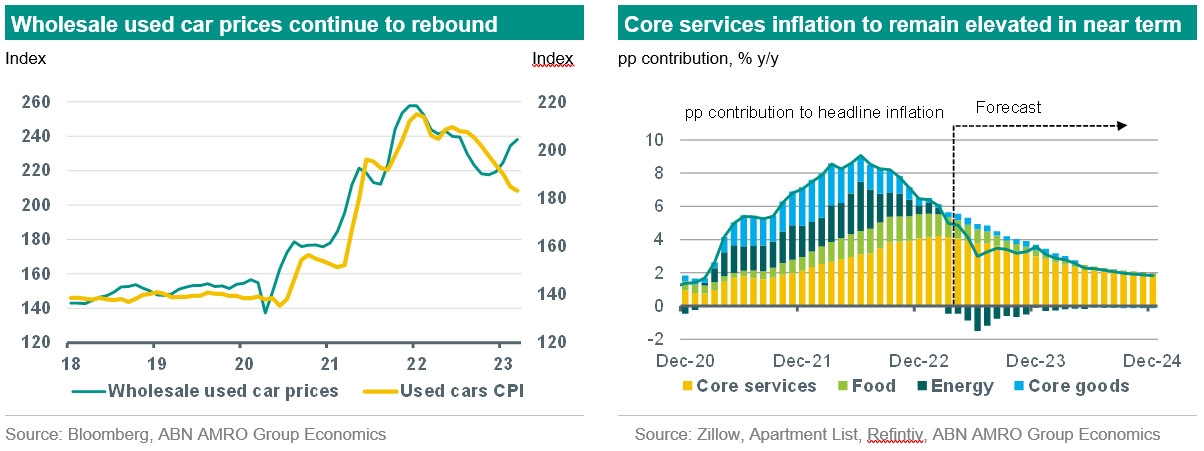

The downside surprise relative to our expectation was due to a further decline in used car prices, which has come despite the c.8% rise in wholesale prices in the year to date so far. Historically, wholesale and consumer used car prices move in tandem (with a lag), so we would assume this pass-through is merely delayed (see chart below).

Headline inflation continued to be more benign, for now, as prior falls in petrol and utility gas prices continue to offset upward pressure from core inflation. A fall in food prices also helped dampen headline inflation, although restaurants and take-out prices accelerated to a 0.6% m/m pace. All told, annual headline price growth slowed to 5.0% y/y (down from 6% in February), while core inflation edged back up to 5.6% y/y (from 5.5%).

Sticky core inflation to maintain pressure on the Fed

Looking ahead, while annual headline inflation is expected to continue to decline – largely on the base effect in energy prices – we expect core inflation to remain high over the coming months. Core goods inflation is expected to continue rebounding as higher wholesale used car prices pass through, while services inflation is expected to remain high as employers pass on higher unit labour costs, amid continued resilient services demand. Our base case is that the Fed hikes one last time, by 25bp at the May FOMC meeting. This assumes the impact of the banking turmoil on lending to the real economy will be limited. Comments by some FOMC voting members in recent days suggested a preference to hold fire at the coming May meeting, as officials monitor the impact of tighter financial conditions on lending. If the impact on lending turns out to be bigger or longer lasting than we expect, there is a risk that the Fed holds fire at the May meeting.