US - Cooling, but not quickly enough

The US economy is cooling, but only very slowly. Financial buffers are likely a key factor. Our base case continues to be for contracting output in Q2-Q3. Any further delay to the downturn raises the risk that inflation becomes entrenched at a higher level than the Fed’s 2% target. Fed officials are sounding more cautious given the tightening in lending standards. We see a risk of more rate hikes if tighter lending standards prove to be temporary.

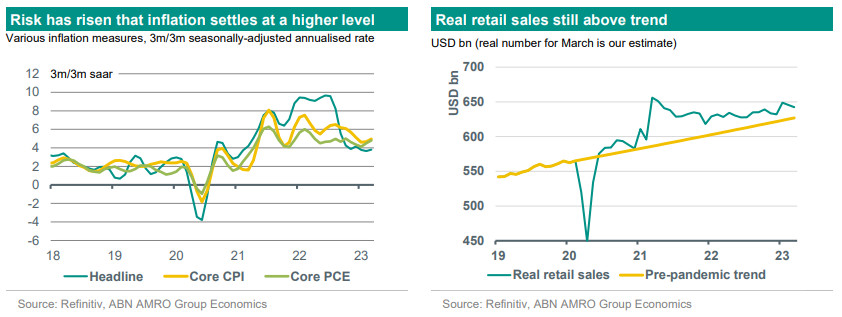

The US economy continued to cool over the past month, but at a snail’s pace. Nominal retail sales fell by 1% m/m in March, though the bulk of this was driven by falling gasoline prices (which fell 4.6% m/m, according to the CPI data). ‘Core’ retail sales, i.e. excluding gasoline & autos, fell by a much more modest 0.3% m/m. The March decline was a drop in the ocean following the 2.8% surge in core retail sales over January and February. Indeed, the details showed continued solid growth in online sales with only modest declines in some categories, such as apparel, which is normalising from the post-pandemic catch-up phase. Eating out (which is reported alongside retail sales) also remained strong, suggesting resilient demand in the face of significant price rises at restaurants recently. All told, we estimate that real retail sales (adjusting for inflation) are still around 2.5pp above the pre-pandemic trend, suggesting persistent excess demand for the time being. A key support for consumption has been continued solid jobs growth. Here, too, although the pace of growth has slowed, it has not been enough to push the unemployment rate any higher. We now expect the unemployment rate to begin rising in earnest in Q3, later than our previous Q2 expectation.

A key reason for the delayed slowdown in the US is likely the significant financial buffers of households and corporates (see Global View). While the household saving rate has picked up from the lows, suggesting somewhat less willingness to rely on buffers, that willingness is still there. We expect this effect to gradually diminish as the year progresses, as the headwinds from tighter monetary policy intensify. For now, Q1 GDP is likely show solid growth of 2-2.5% when the advance estimate is published in the coming week, but we continue to expect mild contractions in output in Q2-Q3. Any further delay to the downturn will likely keep inflation higher for longer, raising the risk that it settles at a higher rate than the Fed’s 2% target. Indeed, while on a range of measures inflation momentum has definitely cooled, recent monthly readings suggest that inflation has settled at around 4% – double the Fed’s target. We expect monthly core inflation to remain stubbornly high for at least the next 2-3 months on the back of rebounding used car prices, continued pass-through from higher housing rents, and elevated unit labour cost growth.

Given the persistent risks around inflation, we continue to expect the Fed to hike rates by another 25bp at the 2-3 May FOMC meeting, and money markets have now mostly priced out any probability of a pause. Fed officials have sounded more cautious on the chance of any further rate rises, given the uncertainty over tighter lending standards, which could do some of the Fed’s tightening job for it in terms of bearing down on demand. Should the tightening in lending standards prove ephemeral, we see a risk the Fed could raise rates further over the summer to be sure that inflation falls sustainably back to target. For now, we expect the fed funds rate to peak at 5.00-5.25%, and for the Fed to start cutting rates in December.