UK - Rates to stay higher for longer, despite falling energy prices

Reduced shock to real incomes has led us to significantly raise our 2023-4 growth forecasts. Still, the economy remains weak, and faces major fiscal and monetary headwinds. The Bank of England is likely to significantly raise its growth projections on the easing energy crisis, and we now think interest rates will stay on the high side for somewhat longer.

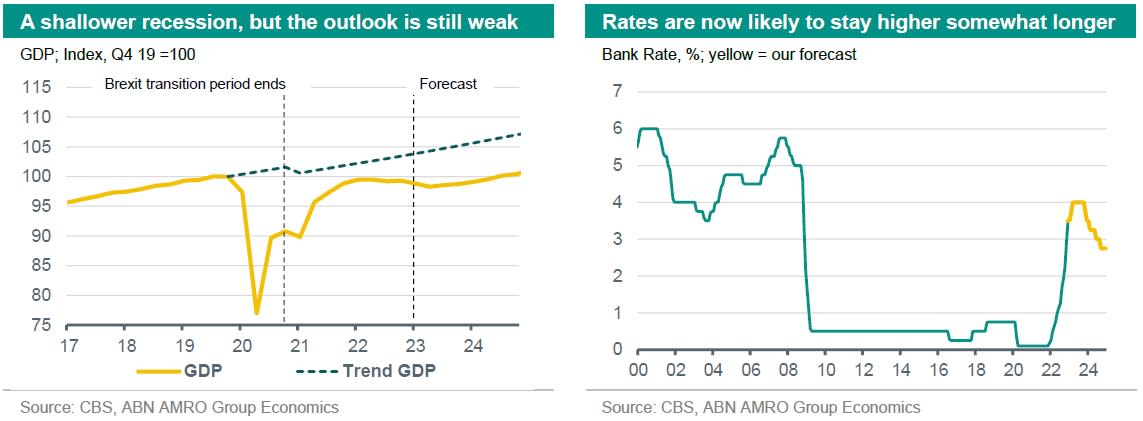

The collapse in energy prices of recent weeks has led to a remarkable improvement in the outlook. As we describe in this month’s Global View, while energy prices are expected to remain above pre-crisis norms, the falls in prices are likely to lead to an earlier recovery in real incomes than we previously expected. As such, we now expect the recession to be concentrated in the first half of 2023, with a gradual recovery expected in H2, as lower energy tariffs start to feed through to household energy bills. Still, the recovery is expected to be a sluggish one to begin with, given the many headwinds facing the economy. As we described in more detail in our Outlook 2023, the tax burden is set to rise significantly from April onwards, and much of the impact of interest rate rises is still to come. All told, we now expect a contraction of -0.8% in 2023 (-1.3% previously), and a somewhat stronger recovery in 2024 of 1.2% (up from 1.0% previously).

Indeed, the easing energy crisis could be a double edged sword for monetary policy – a shallower recession is likely to mean less of a rise in the unemployment rate. While inflation expectations should come down on the back of lower energy prices, this will be offset by stronger worker bargaining power given what is likely to still be a tight labour market. It remains to be seen how these forces net out, but on balance, we think somewhat higher wage growth means the Bank of England is now likely to cut rates at a slower pace than we previously thought. Bank Rate is still expected to end 2023 at 3.5%, from an expected 4% peak in March, but we expect rates to fall more gradually in 2024, to 2.75% (up from 2% previously).

Alongside an expected 25bp rise in Bank Rate, the MPC will publish its latest economic forecasts on 2 February. We expect it to raise its GDP growth forecast, lower its inflation forecast and signal a somewhat more hawkish policy stance. Much has changed since the last forecast update in November, when the BoE projected a two-year long recession. Externally, eurozone growth prospects have improved because of lower gas prices and the resurgence in car production. We have also upgraded our forecasts for China and the US. Domestically, wholesale gas prices have fallen sharply, and these lower prices will feed-through to final users over the course of the year, supporting business activity and household incomes (we expect Ofgem to lower the market-based price cap in July). Another UK-specific development since the November Monetary Policy Report is the restoration of calm and stability in the political and policy landscape (see our Outlook for more).

Set against this is the ongoing dispute between the government and public sector workers which has resulted in numerous strikes across the transport, health and education sectors. The direct impact of the strikes on the economy is judged to be relatively small, with the main risk to inflation and monetary policy from higher wage settlements. A negotiated settlement will most likely result in higher public sector pay with upside risks for inflation and interest rates.

This article is part of the Global Monthly of 23 January 2023