The Netherlands - Consumption resilient, despite purchasing power loss

We expect annual growth to slow to 1.2% in 2023 (from 4.5% in 2022). The near-term risks to our view are tilted to the upside, while medium-term risks are to the downside. HICP inflation is expected to average 4.6% in 2023 and 4.1% in 2024.

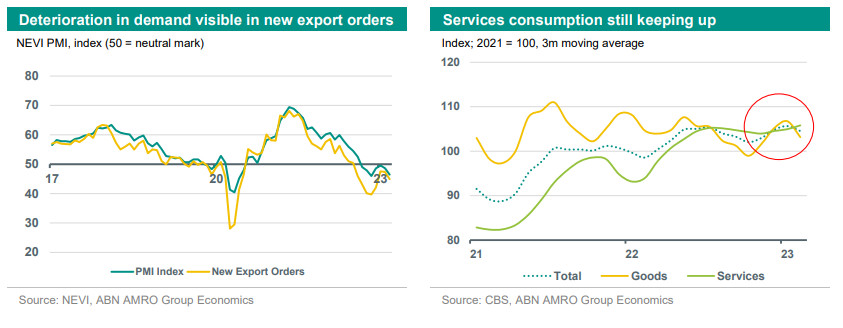

Dutch GDP is expected to grow by 1.2% in 2023 and 1.3% in 2024, cooling down from 4.5% annual growth in 2022. We expect external demand to be lower due to recessions in the eurozone and the US (with both investment and consumption slowing). This weakens the outlook for Dutch exports, which we already observe in the PMI data. The most recent industry PMI showed the new export orders component dropping (read more here). Given the lagged impact of monetary policy – with the brunt of the impact coming around five quarters after the rate hikes – and more rate hikes in the pipeline (we expect the ECB deposit rate to peak at 3.75% in June), monetary headwinds will increasingly be felt over the course of the year. The housing market has already turned a corner on the back of tighter monetary policy and rising interest rates. This means that the support for consumption via the wealth channel effect for new home owners is falling away, which creates a drag on consumption in 2023. In the near term, we expect lower house prices to lead to declines in housing investment. Investment generally is expected to be set for a weak year due to tighter financial conditions and higher rates, but – more importantly – also due to worsening future growth prospects. Finally, the government has stepped in and wage growth is picking up: CLA-wages came out higher than the inflation figure in March. However, the cumulative blow to purchasing power from recent rises in inflation is not fully offset.

Despite the risks to the medium-term outlook mentioned above, recent activity data show that near-term risks are tilted to the upside. Thus far, consumption has proven to be resilient despite the loss of purchasing power. The February figures for consumption show that spending on services remained strong, although aggregate private consumption has slightly decreased (mom). Consumption is supported by an ever tight labour market and government support. We see government support, such as the energy allowance for low income households providing a strong short run impulse for spending. Households are decreasing their rate of additional savings as was shown by the decline in the savings rate in the fourth quarter. The stock of pent-up savings remains a buffer. Moreover, the indexation of pension funds by 7% on average and the 10% rise in the minimum wage (and linked to that, social security) provides support. However, for the remainder of 2023 we still expect consumption to slow, with big ticket items leading the charge. Looking at new passenger car registrations, the first signs of cooling are already apparent.

Meanwhile, headline inflationary pressure is easing, but core inflation is likely to stay somewhat elevated. The NEVI PMI for March showed that the majority of firms in the panel said input prices have decreased (to 46.4 which is below the neutral 50 mark) and suppliers‘ delivery times became shorter. This creates downward pressure on prices. Although headline inflation is pushed down by energy base effects, the broadening of (core) inflation is expected to continue well into 2023.