The Netherlands - Consumer holds the key

Solid growth in 2024 is expected to continue in 2025, but external risks tilted to the downside. Inflation edged up in recent months and is expected to remain higher than eurozone inflation. Dutch house prices are expected to rise by 7% in 2025 and 3% in 2026, down from 8.7% in 2024.

At the start of 2025, the growth outlook for the Dutch economy is solid. The economy is recovering from a period of lower growth due to inflation, and in recent quarters has outperformed the eurozone aggregate. Growth typically originates externally, with increasing exports gradually benefitting households and boosting domestic demand. In the coming two years, we expect the reverse to take place. Risks on the external side are tilted to the downside, with an extended stagnation in main trading partner Germany and potential Trump tariffs clouding the outlook later in 2025. The first half of 2025 will likely see a small boost to activity from a front-loading of exports to the US. Despite this, it will be internal demand driving growth. Households are benefiting from rising real incomes on the back of high wage growth, which is expected to outpace inflation in the coming years, while the government is also supporting growth with an expansive fiscal stance. The lagged pass-through of rate cuts will provide support to investments, although the impulse might take longer to materialize due to capacity constraints and bottlenecks, while companies are not eager to increase production capacity. All in all, we estimate a y/y growth figure of 1.5% for 2025 and 0.8% for 2026.

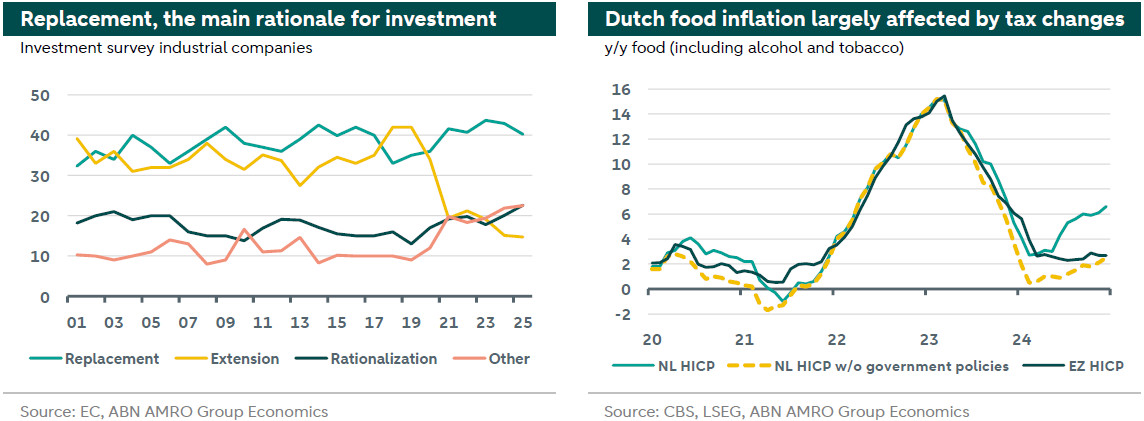

The final quarter of 2024 is expected to show GDP growth of 0.3% q/q following two strong quarters. Generally, consumption will be supported by the continued rise in real incomes from higher wage growth, as well as a normalizing savings rate. Investments are expected to have gained some momentum, particularly in road transport due to the changed tax regulation to vehicles which has been implemented since the start of 2025. The external side is expected to benefit from a gradually improving eurozone economy, while German underperformance puts a lid on export growth.

The last month of 2024 showed the highest inflation figure of the year, coming in at 3.9% y/y (HICP). The high December figure was particularly driven by firming services inflation and less favourable energy base effects. The former is largely affected by higher housing rent indexation. Similarly, food prices have contributed substantially due to higher levies on tobacco and drinks. Absent these tax changes, the December figure would have come in at 3.0%, so roughly 1pp lower. Generally, we expect inflation to ease in the coming months, and average 2.9% in 2025 and 2.4% in 2026 (HICP). But given still-elevated wage growth, a tight labour market, and the expansive fiscal stance of the Dutch government, inflation will stay above the eurozone average throughout 2025.

2024 was generally a strong year for Dutch house prices, with an increase of 8.7% y/y. For 2025 we expect price growth of 7%, given still-rising household incomes on the back of high wage growth, lower mortgage rates, and a persistent supply shortage. Looking ahead, as inflation normalizes and wage growth slows, we expect a 3% rise in house prices in 2026. Through the wealth effect – homeowners feel wealthier due to the increased value of their assets – increasing house prices can support consumption. Additionally, the higher number of expected transactions boosts housing market-related purchases, such as furniture.