The last Fed hike?

The Fed is expected to hike rates one last time on Wednesday, but we could be in for some further rate rises if the economy doesn't cool more quickly.

Fed likely to pause after May, but keep a tightening bias

This coming Wednesday, the Fed is widely expected to raise rates perhaps for the final time in this tightening cycle, which would take the target range for the fed funds rate to 5.00-5.25%. This level has some symbolic importance in that it is also roughly the peak the fed funds rate reached in 2006-8, prior to the global financial crisis. With no update to the ‘dots’ projections at this meeting, the focus for markets will be on any changes to the policy statement, and Chair Powell’s remarks at the press conference. With regards the statement, the Fed typically does not explicitly signal an end to the tightening cycle given that it is difficult for the Committee to know with any confidence whether it has reached the end. Indeed, in both the most recent tightening cycles, the final hike was accompanied with a statement suggesting an openness to further rate hikes. For instance, in , the statement included the line: “The Committee judges that some further gradual increases in the target range for the federal funds rate will be consistent with sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee's symmetric 2 percent objective over the medium term.”

“Although the moderation in the growth of aggregate demand should help to limit inflation pressures over time, the Committee judges that some inflation risks remain. The extent and timing of any additional firming that may be needed to address these risks will depend on the evolution of the outlook for both inflation and economic growth, as implied by incoming information.”

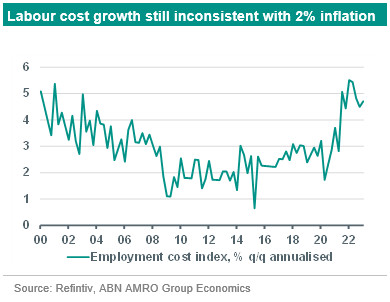

We expect similar language in the May policy statement, perhaps even repeating verbatim the language of the March statement. Given the persistence in underlying inflation – confirmed by the elevated Employment Cost Index reading for Q1 released last Friday – we think it is unlikely the Fed would completely remove the tightening bias and shift to more neutral language at this stage. Instead, we think it will wait for clearer signs that the economy is weakening, and that underlying inflationary pressures are cooling.

Risk is still tilted towards some further hikes

Our base case is that May will indeed herald the last Fed hike of this cycle, but we see the risk tilted toward the Fed continuing to hike through the summer. The macro drivers have been conflicting of late. Consumption has surprised to the upside, suggesting resilience in the face of headwinds, but the trend since the pandemic has been for strength to be revised away, while recent high frequency data points to a rapid cooling in momentum. Meanwhile, the banking sector turmoil does look to have driven a tightening in bank lending standards, but it is still unclear whether that tightening will persist; a key input in this regard will be the results of the Fed’s Senior Loan Officer Survey, due out over the coming week (there is no official release date, but precedent suggests it will be out around 8 May). Given the significant uncertainty, we expect the Fed to shift to full data-dependent mode from the June meeting onwards. For now, our base case is that rates will hold steady at 5.00-5.25% for much of this year, with the Fed starting a rate cutting cycle from December. This assumes that a unfolds over the coming months. See our for more.