The ESG Economist – A practical carbon border adjustment mechanism

The European Commission has proposed a carbon border adjustment mechanism (CBAM) as part of a package of measures to help meet its ambitious emission reduction goals. The mechanism aims to make sure that the imported goods face the same cost of carbon emissions as domestically-produced goods do, in order to prevent carbon leakage.

The scheme is limited in the products it covers, which means that it is not a comprehensive equalisation of carbon costs, but it does avoid the complexity that a wider scheme might create. The phasing out of free Emissions Trading System allowances should mean that CBAM will likely be World Trade Organisation compliant.

Introduction

As part of a package of energy and climate laws aimed at reaching the EU’s 2030 goal of cutting emissions by 55%, the European Commission (EC) has proposed a carbon border adjustment mechanism (CBAM). The basic aim of the mechanism is to make sure that the imported goods face the same cost of carbon emissions as domestically-produced goods do, in order to prevent ‘carbon leakage’. This note sets out the rationale behind the proposal, the details of how it would work, as well as some of the drawbacks and limitations of the scheme.

Preventing carbon leakage

The EC’s case for proposing CBAM is that the EU has more ambitious policies to tackle climate change than many of its international trading partners. Specifically, the price applied to green house gas emissions in Europe is higher than elsewhere, which raises the risk of carbon leakage. Carbon leakage occurs when in response to (higher) charges on emissions in the EU, businesses transfer production to other countries or imports from these countries replace products (which are responsible for lower emissions) produced domestically. The concern is that carbon leakage would offset the impact of the EU’s climate policies on global emissions by increasing emissions in other countries. CBAM is aimed at addressing this issue, but also creating incentives outside the EU to step up their efforts to reduce their carbon emissions.

The EU has had an Emissions Trading System (ETS) in place since 2005 to limit emissions. Yet the evidence of significant carbon leakage up until now has not been very convincing (see a Bruegel study from last year here for an overview of some of the evidence). However, this might be because of existing carbon leakage protection mechanisms. In particular, ETS sectors that are most vulnerable to carbon leakage are granted free emission allowances as well as state subsidies to compensate for higher electricity costs. While addressing the risk of leakage, the Commission notes that the system of free allowances also dampens the incentive to invest in greener production at home and abroad. Meanwhile, the EC reasonably makes the case that the divergence in climate policies, and hence the risk of carbon leakage, will likely increase going forward, given the EU’s accelerated efforts. Emission reduction targets have been made more ambitious, while the free allocation of allowances will decline over time (see our note ‘Stricter ETS to accelerate emission cuts’ – here)

The way CBAM will work

The EC considered a number of different options of how to design the CBAM. Ultimately it is proposing a system that mirrors the ETS regime. In particular, as with ETS allowances, importers will need to surrender CBAM certificates that reflect the carbon emissions of the products. The certificates will be purchased at a price that corresponds to that of the ETS allowance (as determined by the weekly average auction price in EUR/t CO2 emitted) at that time, but would be eligible for a reduction equivalent to any (unrebated) carbon price paid in the country of production. While the ETS sets an absolute cap on emissions, the CBAM will not set import limits.

The importer is charged with reporting the actual emissions embedded in the product (direct emissions during the production process of the products covered) and would then hand in the number of certificates that correspond to those emissions. A back up system will be available for cases where the importer does not have sufficient data on emissions. In these cases, the carbon emission intensity of the products would be based on default values, but the importer will have the opportunity to demonstrate better performance on the basis of evidence of actual emissions. For electricity, the Commission’s preference is to employ a reference value for emissions embedded in imported electricity based on the average emission factor of the EU electricity mix, but importers will have the option to demonstrate lower emissions at their installation level. The emission declaration and certificate handover would take place annually and would cover the previous year’s import volumes. The system would be administered by national climate authorities.

The scheme will be applied gradually over a 10 year period starting in 2026, though there will be a transition period between 2023 and 2025 where the system is applied without financial adjustment. At the end of that period, free ETS allowances will be reduced by 10 percentage points each year and the CBAM will be phased in. As a general principle, the EC states that at no point over the transition period should imports receive less favourable treatment than domestically-produced goods.

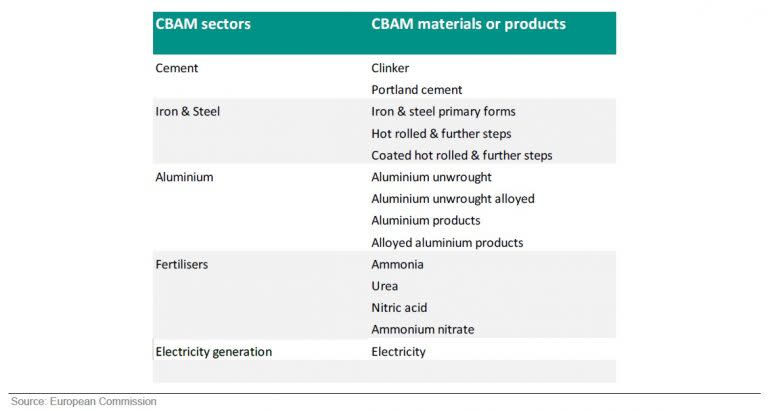

The scope of the scheme

The EC’s ultimate ambition is for a broad product scope of the CBAM that would ensure that the treatment of imports is equivalent to that of domestically-produced goods. However, it deems that it is prudent to start with a more limited number of sectors. The initial product scope is set out in the table below.

The products were selected on the basis of:

(a) Products that are relatively homogeneous with increased risk of carbon leakage

(b) Relevance in terms of carbon emissions

(c) Limited complexity and administrative burden

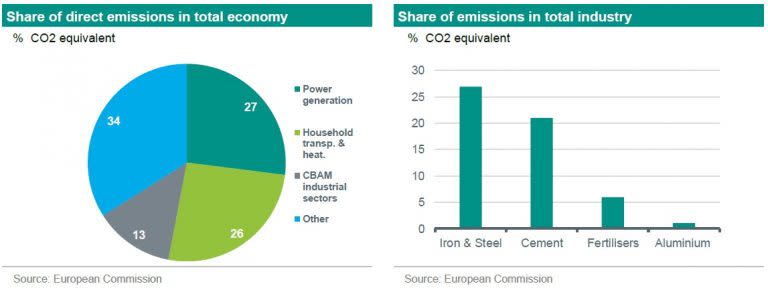

The industrial sectors in scope account for more than half of total emissions in total industry. Taken together with electricity generation, they account for around 40% of total CO2 equivalent emissions.

Impact of CBAM

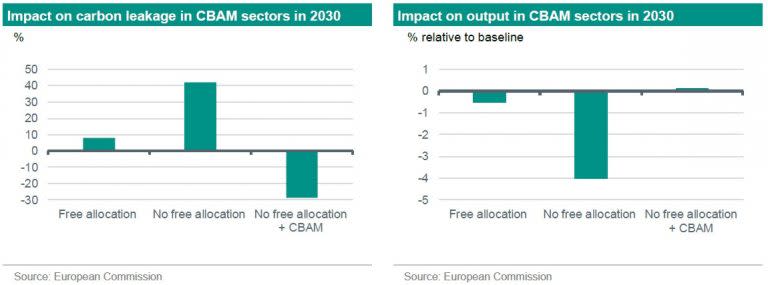

The EC made projections of the impact of various scenarios and policy options on carbon emissions and on the economy as part of its impact assessment. We show a selection of outcomes below under three of these scenarios and policy options. The ‘free allocation’ scenario is one of increased climate ambition to meet the 55% target, free allowances under the ETS continuing and no CBAM. The ‘no free allocation’ scenario is the same but removes free allowances. The final scenario also removes free allowances but introduces the CBAM. As can be seen in the charts on the next page, the introduction of the CBAM leads to a significant reduction in carbon leakage (defined for a particular sector(s) as the change in emissions in non-EU divided by the change in emissions in the EU). In addition, the CBAM would prevent the fall in output that would take place in scenarios with no border adjustment and a stepped up climate ambition.

Drawbacks and limitations

The CBAM’s initially limited product scope raise the risk of carbon leakage in other sectors along the value chain. Luis Garicano – member of the European Parliament and Professor at IE Business School – makes the case (see here) that intermediate or end products, which use the basic materials covered by the CBAM, could be produced using those materials sourced outside the EU before being imported into the EU. The degree of carbon leakage would be higher, the higher the value share of the basic material and vice versa. The EC estimates that on aggregate the risk of carbon leakage downstream is quite low, but also admits that this may change as carbon prices rise.

Another limitation of the CBAM is the potential for ‘resource shuffling’. This refers to the practice of steering the products resulting from less emission-intensive production towards the EU, while the overall carbon intensity of production in the importers domestic market remains unchanged. The estimates shown above, do not make any allowance for resource shuffling. This is a risk that would be difficult to mitigate without moving to a system of measuring emissions based on a reference value rather than on actual values.

Finally, the CBAM has the potential to result in a political backlash from the EU’s international trading partners and could potentially result in trade disputes. Indeed, the Russian government has already been very vocal in its opposition. Our understanding however is that the CBAM in its current form is very likely to be judged as WTO compliant, given that the phasing out of free allowances allows for the equal treatment of imports and domestically produced goods.

A practical scheme

All things considered, the CBAM seems to have been designed in a practical way, which will limit carbon leakage in the sectors covered, while allowing the ETS to become more effective by reducing allowances. Although the scope is limited in the first instance, a wider scheme may have been very complex and difficult to administer. There are caveats. The final shape of the proposal from the EC could change following what are likely to prove long negotiations between member states. In any case, following the transition period, the EC will evaluate the scheme, including whether to extend its scope.