SustainaWeekly - Positive tipping points could supercharge rise of renewables

In this edition of the SustainaWeekly, we first discuss how developments in transition technologies are non-linear. Based on a new report, we discuss the existence of tipping points, the point at which new solutions cross a threshold of affordability, attractiveness or accessibility leading to mass adoption. What is more, a tipping point for one solution can have cascading effects on other solutions by bringing their tipping points closer as well. This may explain the structural underestimation in the rise of renewables. We dig in to one example of these cascading effects. We then go on to review the new EU Green Bond Standard, where a final text was recently agreed. We assess the main features of the regulation and the implications for green bond markets. Finally, we assess the push by some EU countries to exempt cars with internal combustion engines fuelled by synthetic fuels from the 2035 new sale ban. We zoom into the pros and cons of synthetic fuels.

Economist: Past assessments have underestimated the speed of capacity increase of renewable energy. One reason is the existence of positive tipping points, the point at which new solutions cross a threshold of affordability, attractiveness or accessibility leading to mass adoption. There are solutions that are not only close to a tipping point, but also have cascading effects on other solutions by bringing their tipping points forward in time as well.

Strategy: A final text regarding regulation of the EU Green Bond Standard has been agreed and could become effective in the second half 2024 or early 2025. The EU GBS is likely to result in more fragmentation than harmonisation at the start. But over time, fragmentation is likely to diminish, as EU GBS should support investments in taxonomy-aligned activities, while we see larger greeniums for green bonds aligned with the EU GBS.

Sector: One of the key measures to achieve the EU’s emissions target is to end new sales of internal combustion cars and vans by 2035. However, the vote at the European Council was delayed because some countries proposed an exemption for cars with internal combustion engines fuelled by synthetic fuels. Synthetic fuels are not currently the most viable or efficient solution for cars, though there are some advantages as well.

ESG in figures: In a regular section of our weekly, we present a chart book on some of the key indicators for ESG financing and the energy transition.

Underestimating the impact of tipping points

The IEAs annual assessment is that renewable energy growth will be strong but insufficient for a net zero scenario

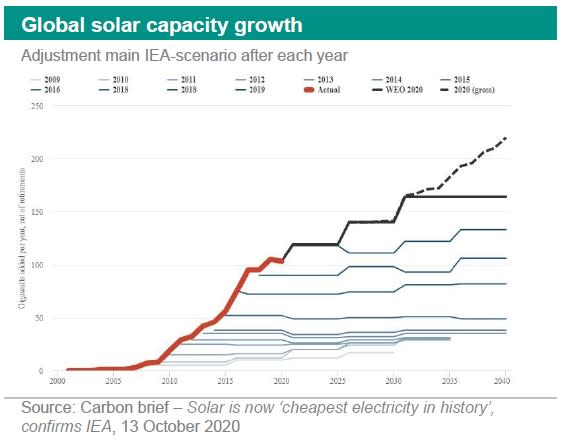

However, earlier assessments of the speed of capacity increase of renewable energy shows that there is a material underestimation of the actual growth of renewable energy capacity

One reason for this is the existence of positive tipping points, the point at which new solutions cross a threshold of affordability, attractiveness or accessibility leading to mass adoption

There are solutions that are not only close to a tipping point for mass adoption, but also have cascading effects on other solutions by bringing their tipping points forward in time as well

When trying to assess the speed of the energy transition, the IEAs annual assessment of renewable energy growth for the coming decade is an important variable. Unfortunately the projection shows that the growth in renewables is unlikely to be sufficient to get us to the pathway of IEAs Net Zero scenario. Even the latest projections of 2022, which shows the largest ever increase in renewable energy growth projection, is insufficient for a net zero pathway. Should we worry? Maybe not. Earlier 6-year assessments of the speed of capacity increase of renewable energy shows that there is a massive underestimation of the actual growth of renewable energy capacity. Particularly for Solar energy, the annual 20 year ahead estimation fails to capture the remarkable growth in solar energy capacity every year since 2009.

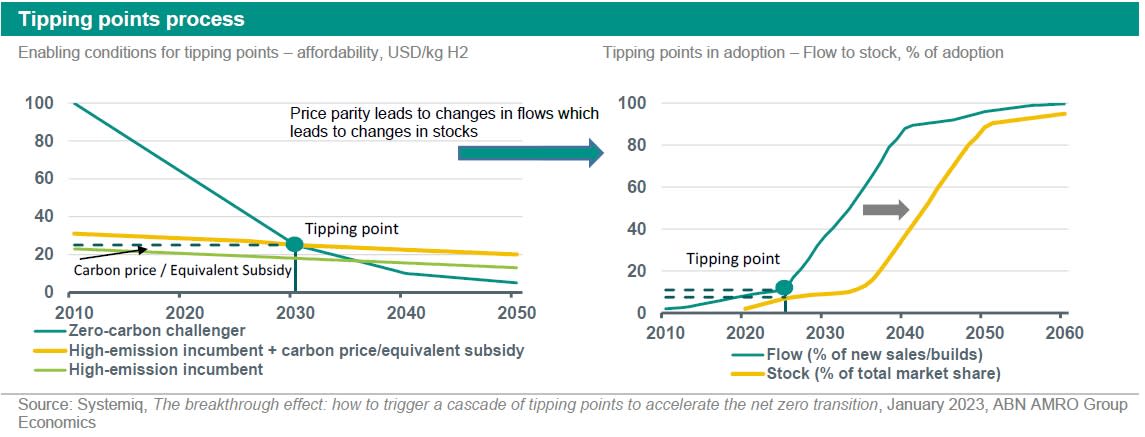

What may partly be driving this underestimation is the existence of positive tipping points that are notoriously hard to predict. A positive tipping point is a point in time at which new solutions cross a threshold of affordability, attractiveness or accessibility in comparison with incumbents. What follows is mass adoption through self-enforcing feedback loops of learning, leading to cost decrease and quality improvements which again create more adoption. When close to such a tipping point, relatively small interventions can push the new solutions into the self-enforcing dynamics. In this week’s Sustainaweekly we look at a recent study in tipping points per sector. We discuss how these tipping points work, what the nearest and most probable tipping point is and what signals to look out for to confirm that a tipping point is near. For this assessment we mainly rely on a by Systems Change Lab, a collective of researchers from academia and consulting.

Conditions for positive tipping points

Affordability is the most important criteria for a new solution to reach a tipping point. As costs fall as a function of cumulative production, the easy of producing large quantities is a key element of a new solution. As such rather small simple products or services with short lifetimes are more likely to speed up production and learn to improve the production process with every new product produced. The tipping point is reached in terms of affordability when price parity is reached between the new solution (price including subsidies) and the incumbent solution (price including carbon tax) as shown in the left picture below. Besides affordability, attractiveness in relation to the existing solution is also important. During the energy crisis, the installing of solar panel and heat pump installation for households was not only financially attractive but it also was a way to refuse gas consumption from a regime that had initiated the war in the Ukraine. For many, the principle of ‘we do not want to make Putin earn money from me to finance the war’ became an attractive argument besides the cost reduction potential.

Finally, adoption also depends on accessibility. What good is a solution if it is affordable and attractive if it is not accessible? Often it is the infrastructure that creates accessibility but also labour shortages or other capacity constrains in execution could hamper or enable accessibility and hence adoption.

Fight for dominance: reinforcing versus balancing feedback loops.

Once the conditions mentioned above are in place, the reinforcing dynamic starts (right hand picture). Deploying an innovation creates learning effects and scale effects. As such, the product and the production processes improve, the fixed costs are spread over more products and as the product becomes cheaper and better, the demand increases further. Entrepreneurs observe opportunities for complementary products or new applications for the initial product and this creates more use cases, and greater dependence through network effects. Market participants that are following this development start expecting the pace of adoption to continue and investments start flowing towards the solution enabling even more deployment.

While these reinforcing effects take place, incumbents start getting worried as they see their product declining at the margin. They pull their strength through lobbying, standard setting, and network effects to slow down the speed of the adoption of the new solution. Particularly the network effects of consumer practises, business models and investments that have formed around the incumbent technologies can create powerful slowing of adoption, known as a system lock-in. The Dutch coal mines are a famous example of an incumbent energy that had penetrated into the economic and social fabric of the Limburg region (1). It took a deliberate and active phase out strategy by the government together with stakeholders to open up to the new energy solution of natural gas at the end of the sixties.

Cliff edge moment for incumbents

Once incumbents output goes from slower growth from falling demand into decline of output through production cuts, diseconomies of scale also become self-enforcing. As a result, the price disadvantage grows larger and financial devaluations occur as investors move elsewhere and capital costs increase. When incumbents start slowing their R&D investments, their patent applications and their spending on lobbying, together with higher price volatility and lower ability to recover from setbacks, strong decline may be on the cards (2).

Most likely and most impactful tipping point

According to the Systems change lab study, there are solutions that are not only close to a tipping point for mass adoption, but also have cascading effects on other solutions by bringing their tipping points forward in time as well. We discuss one example, but the has many more highly relevant tipping points for many sectors.

Making emission free vehicles mandatory

Mandating emission free vehicles brings certainty to car producers about their future zero emission vehicle market (ZEV). This triggers rising production volumes which in turn drives down costs and increases demand. Public expenditures need to warrant that sufficient accessible EV charging stations are present. The scale up in the EV market for light duty vehicles triggers at least two new accelerations:

Battery deployment: By 2030, 70 percent of installed battery capacity will come from electric vehicles. If EVs adoption reaches 60 percent of the global passenger vehicle sales (not stock) by 2030, the demand for batteries will be the ten-fold of current levels. Even with learning rates constant (which is a conservative assumption) battery costs would have come down with 60 percent in 2030.

Total costs of wind and solar: As battery costs make up around 30 percent of the total costs of solar and wind, the total costs of these power solutions compared to the costs of coal or gas comes down faster.

Smart grid solutions: Furthermore, the better performing and cheaper batteries provide flexibility for smart grid solutions that could trigger many use cases for dynamic electricity pricing solutions for home owners.

Heavy road transport: Trucks powered by better performing and cheaper batteries start to get closer to the point where they can outcompete petrol or diesel trucks.

What evidence to look out for in the coming years?

Indicators to look out for that provide more certainty of the tipping points approaching are the following:

Obviously the first thing to look out for is the sticker price of EV passenger cars to go below combustion engine vehicle. Expectations are that this is set to happen in 2025 -2026 in EU US and China. With the inflation reduction Act in the US subsidizing the gap to reach price parity, this is rather likely. More doubtful is the presence of sufficient charging stations. In 2021 1.8 million charging stations have been installed globally, and this needs to increase to 5 million stations to support deployment that moves EV adoptions to its tipping point.

For the battery deployment to reach the tipping point such that solar and wind power become stand alone power sources, the levelized costs of electricity generated (and stored) from wind and solar needs to become below the levelized costs of electricity generated from coals or gas fired power plants. Already today, battery costs have come down massively (90% compared to 2010) and are expected to reach 110 dollar/kWh this year. The levelized costs of solar plus storage is currently below 50 dollars /kWh and is expected to be cheaper that the levelized costs of gas power in the US this year.

Also, at least 500 billion dollar investments annually in transmission and distribution of power needs to be put in place to reach the tipping point by 2030. Here are the main uncertainties. In 2022 around 300 billion dollar has been invested in transmission and distribution and this needs to have reached 500 billion in the next few years. Also the planning and permitting timelines are mainly in Europe around 5 times longer than legally established limits.

(1) Geels, et al, 2017 Sociotechnical transitions for deep decarbonizationAccelerating innovation is as important as climate policy. In: Science, climate and innovation policy.

(2) Scheffer et al. 2009 Early-warning signals for critical transitions. In: Nature.