SustainaWeekly - Financing green hydrogen

The financial sector has a crucial role to play in boosting the energy transition by allocating and steering the funds towards clean and climate- friendly technologies, one of which is green hydrogen. However, private investments to boost the rollout of green hydrogen still fall short. In this SustainaWeekly, we first focus on the obstacles limiting the potential to finance green hydrogen and propose potential remedies to reduce these risks. We then go on to assess the key results of the ECB’s stress test for corporates and banks. Finally, we zoom in on alternative heating technologies to reduce greenhouse gas emissions.

Economist: Green hydrogen could play an important role in the transition towards a low carbon economy. However, the uncertainty of renewable power supply, the technological immaturity, the lack of clarity about demand, and the absence of associated infrastructure weigh on the business case for green hydrogen. PPA usage, the alternative purposes of green hydrogen, and government intervention are among the remedies.

Strategist: The ECB stress-tested the economy under different transition scenarios over an 8-year horizon. Corporates are affected by transition risks through lower profitability and higher leverage, which result in higher credit risk. This increased risk ultimately feeds into banks’ own credit risk, which could lead to significant expected losses. Transition risk for the banking sector in the euro-area is very much concentrated within a few large banks.

Sector: Reducing emissions and reaching net zero for heating is a complex task. One option is to burn fuels or mass but these need to be sustainably resourced. Heat can be absorbed from other sources such as the sun, ground, air, water or rest heat. Renewable electricity can also be converted into heat. So there are several options but these options are currently more expensive than just burning fossil fuels.

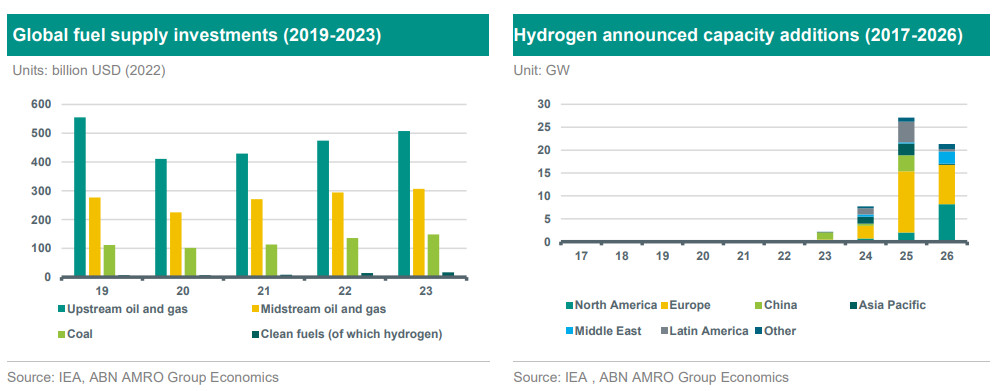

ESG in figures: In a regular section of our weekly, we present a chart book on some of the key indicators for ESG financing and the energy transition.

Financing green hydrogen

Green hydrogen could play an important role in the transition towards a low carbon economy…

…But the uncertainty of renewable power supply, the technological immaturity, the lack of clarity about demand, and the absence of associated infrastructure are the main risks weighing on the business case for green hydrogen

PPA usage, the alternative purposes of green hydrogen, and government intervention are among the remedies to ameliorate the business case for investors

The current risk-return profile for green hydrogen is best suited for institutional investors such as development banks, along with oil and gas companies

Introduction

Within the financial sector, the last few years have witnessed a shift from a profit-driven paradigm towards incorporating social and environmental aspects in the investment decision making. When it comes to climate change, most investors acknowledge physical and transition risks and incorporate them into investment decisions. At the same time, the financial sector has a crucial role to play in boosting energy transition by allocating and steering the funds towards clean and climate-friendly technologies, one of which is green hydrogen. With its multiple advantages, green hydrogen is set to have a prominent position among the set of possible fuels of the future (see our note on green hydrogen ). In this direction, Europe has put in place a strategy for green hydrogen with a goal of reaching 10 million tons of domestic production by 2030, while importing an equivalent amount. Such a goal entails huge funding requirements both public and private. However, private investments to boost the rollout of green hydrogen still fall short even though the needed funds are readily available (read more ). Motivated by this observation, this note aims to answer the following question: what are the obstacles limiting the potential to finance green hydrogen? We answer this question from an investor perspective by exploring the risks along the value chain of green hydrogen and propose potential remedies to reduce these risks and ameliorate the business case for green hydrogen.

Risks along the value chain

There are multiple bottlenecks along the value chain for green hydrogen, which constitute different sources of uncertainties that weakens its business case and deter investments. The value chain for green hydrogen can be split into four broad categories: renewable power production, the electrolysis process, the associated infrastructure, and the final utilization of produced hydrogen.

Renewable power production

In order for hydrogen to gain the green label, it should be produced using renewable power. Thus, from the supply side, green hydrogen production is tied to the availability of renewable power supply. However, the uncertainty surrounding the time schedules for renewable capacity deployments is increasing the risks of insufficient power supply to run the electrolysis process, thus weakening the business case of green hydrogen. The delays in investments are tied mostly to long permitting times, rising capital costs (increase in interest rates and production inputs), and the lack of supporting infrastructure. Moreover, as the capacity is taking more time to be built, coupled with a rising demand, renewable power will be expensive, which translates into a higher cost of green hydrogen production, along with lower competitiveness against its fossil counterparts, which in consequence worsens its business case even further.

The electrolysis process

From the technology side, green hydrogen is mainly produced through a water electrolysis process that separates the water molecules into hydrogen and oxygen. There are currently three types of electrolysers, and each has its (dis)advantages. Alkaline electrolysers are relatively cheap, but their performance is sensitive to any interruptions. Proton Exchange Membrane (PEM) electrolysers, on the other hand, are more flexible and can handle interruptions better, but this comes with higher cost tag. The third type is Solid Oxide electrolysers, which are a less mature type of technology and still need more time to be commercialized. Green hydrogen that relies on Alkaline or PEM electrolysers is on a demonstration-early adoption phase, while green hydrogen produced using Solid Oxides electrolyser is at large prototype/demonstration phase. Accordingly, the scalability of these technologies is still to be proven. Additionally, the electrolysis process relies on different components, produced by different parties, that may not be compatible or work well together, which result in the absence of performance guarantees by manufacturers. This in turn increases the technological risk of investing in electrolysers and weakens its business case.

The final use of produced hydrogen

Green hydrogen is envisioned to be the transition solution for hard to abate sectors where electrification is not possible. However, these sectors need to invest in adjusting their processes in order to incorporate green hydrogen into their production mix. But for these investments to take place, clarity on the timeline for green hydrogen availability is needed. At the same time, absence or uncertainty of green hydrogen demand, as the transition in industry is stalled, weakens the business case for green hydrogen. Accordingly, there is a “chicken-egg” dilemma: transition in industry depends on the availability (the supply) of green hydrogen, while green hydrogen investments require demand certainty.

Associated infrastructure

Green hydrogen projects require a supporting infrastructure to roll out. From the upstream of the value chain, there is a need for high voltage grid extensions that facilitate the delivery of renewable power to the hydrogen premises, which are not (yet) always readily available. For example, there are currently many challenges with regards to bringing back energy generated from offshore wind farms to the shore Additionally, after green hydrogen has been produced, there is also a need for transportation and infrastructure to the final user. The type of final user will also ultimately determine the most appropriate form for this hydrogen to be carried. For example, delivering hydrogen as a fuel for ships is done best by transforming it to ammonia especially for long distance international trips, while using it in industrial process can be in a gaseous or liquid form. Each form requires a different type of infrastructure and associated investments, which translate into different regulation, permitting procedures, and technical burdens. Needless to mention, the scale of funding needed for these infrastructural investments is huge. These complex interrelated aspects compromise additional uncertainty that undermines the feasibility of green hydrogen projects.

Is regulation helping the business case of green hydrogen?

Sometimes certain regulation induces some restrictions and market dynamics that restrict the full potential of a technology and weakens its business case from an investor perspective. For example, the European Union has set relatively stringent rules for the production of green hydrogen. One of which is that the electrolysers should be powered by a newly built dedicated solar and wind power installations, with an initially lenient monthly compliance, that needs to turn into an hourly compliance basis as of 2030. These rules favour the flexibility of electrolysers and by consequence the PEM electrolysers, which are relatively more expensive. At the same time, the intermittency of renewables entails that the production of green hydrogen is vulnerable to weather conditions, which entails that electrolysers may not operate at their full capacity when the wind is not blowing or clouds are covering the sky. This, in turn, increases the cost for green hydrogen production for the EU and makes it less competitive 1). Another example is the adoption of different calculation mechanisms for emissions and carbon credits across countries, which means that the value associated to green hydrogen usage by final sectors downstream the value chain could differ between trading partners, resulting in large discrepancies between companies and countries. As a consequence, the business case for downstream utilisation projects could be compromised and may slow down the offtake of green hydrogen. A third example relates to the conditions associated to subsidies. In the US, the accessibility of subsidies for offshore wind projects is tied to the usage of domestic components. This conditionality, along with rising capital cost, made many offshore projects unprofitable as domestic components are witnessing a supply shortage for needed materials such as steel. By consequence, delays for hydrogen projects can be expected and its business case is adversely affected.

Remedies to boost investments

Due to the aforementioned uncertainties, the risk-return profile for green hydrogen projects is still not attractive for most investors. In this section, we outline potential remedies that can relax some of these risks for investors and boost investments.

With regard to renewable power supply, the usage of Power Purchase Agreements (PPA) can help to improve the business case for renewable power investors and reduce the supply uncertainty for electrolysers investors. At the same time, supplying different components of the electrolysers from the same supplier will be helpful in increasing the compatibility of different components in the electrolysis process and encourage manufacturers to extend performance guarantees that reduce the technological risk for investors.

With regards to demand uncertainty, the diversification of green hydrogen usage could be considered as a remedy here. That is, even in the case of the absence of demand from the final sector, green hydrogen can be used as a medium of storage to stabilize the grid. It can also reduce grid congestion and the need for grid extensions by using alternative off-grid hydrogen networks to transport embodied electricity to where it is needed. Furthermore, produced hydrogen could be exported.

The remaining remedies require government intervention in terms of providing a clearer and compatible vision for green hydrogen, a timeline for infrastructural developments, shorter permitting times along the value chain, and using the proceeds of carbon prices to finance the required infrastructure or speed up the adoption phase where private capital is scarce. Moreover, on different levels, the government can facilitate the coordination between related stakeholders to resolve bottlenecks and boost green hydrogen investments. For example, prioritizing the use of green hydrogen to sectors that are most in need is also key to boost the transition in these sectors in time and with minimal delays. Furthermore, the usage of regulation mandating the use of hydrogen in final sectors, such as transport or manufacturing, would boost demand and reduce uncertainty for investors. Finally, the higher cost of green hydrogen compared to alternative fossil fuel and grey hydrogen require Capex and Opex subsidies that reduce the cost at first stance. Other tools that increase the competitiveness of green hydrogen, such as the usage of grants and the usage of contracts for difference, could also come into play.

The finance sphere

Green hydrogen projects are long-term capital intensive with relatively high risk, which make institutional investors the most appropriate source of finance for these projects. The long term and climate friendly nature of green hydrogen projects fits the mandate of pension funds and insurance companies, but the current risk profile of these projects is higher than these institutions can bear as they are quite risk averse. But, as we get more certainty along the value chain, more finance could be unlocked from these institutional investors. For current risk level however, project finance will be the main financing instrument for green hydrogen. The development theme of green hydrogen is also important along with its international aspect, which make it relevant to development banks, especially in countries abundant in renewable power potential. Furthermore, oil and gas companies aiming at diversifying their portfolio and repurposing the existing fossil fuel infrastructure, along with the associated reputational benefits, make green hydrogen an attractive opportunity for these companies. These companies can invest at the same time in multiple segments along the value chain (renewable power and electrolysis, for example), which reduces many of the aforementioned risks. Finally, diversifying the available funding sources for hydrogen projects could play an important role for large-scale deployment of green hydrogen.

We aim to dive more in the incentives of different stakeholders in the finance sphere in a future note.

1) Different rules have been adopted by China that favours the Alkaline cheaper variant.