SustainaWeekly - Deconstructing Air France-KLM’s SLB framework

In our first SustainaWeekly of the new year, we start by looking at the Sustainability-Linked Bond (SLB) Framework of the French-Dutch airline group Air France-KLM, which is also the first one from the aviation sector. In particular, we analyse Air France-KLM’s proposed target and how it fits within the decarbonization strategy of the aviation sector in a net zero scenario. We go on to assess trends in global electricity demand and some of the structural forces at play. Finally, we look at recent trends and the outlook for greeniums in the covered bond market. We wish all our readers a Happy New Year!

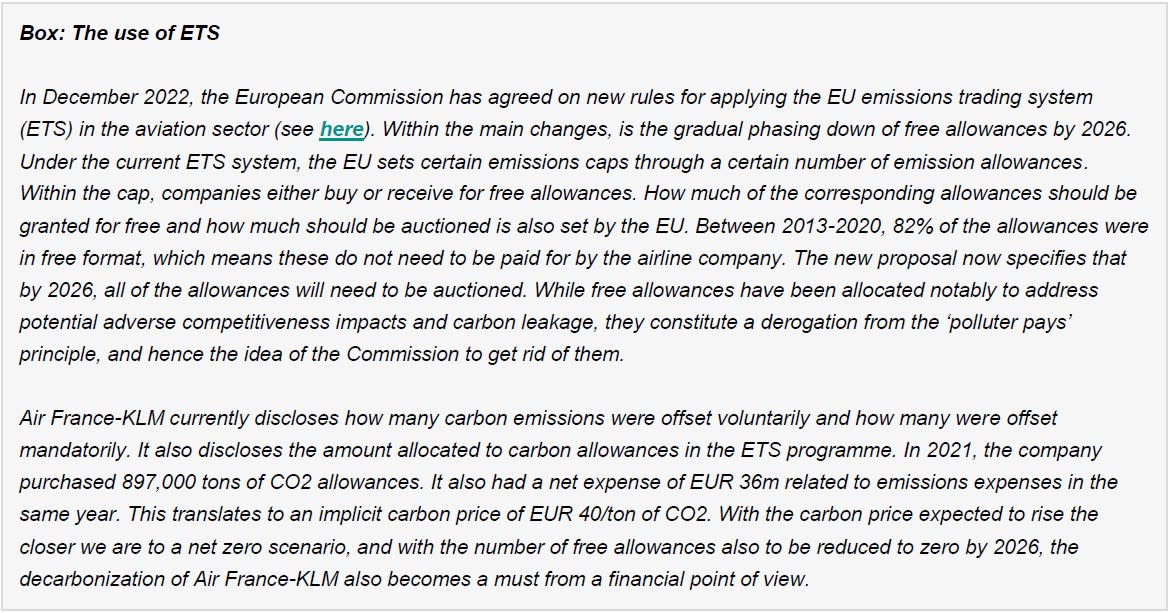

ESG Bonds: Air France-KLM published a Sustainability-Linked Bond (SLB) Framework, where it commits to reduce emission intensity by 10% by 2025 and by 30% by 2030. Using different estimates for revenue ton-km and revenue passenger-km, our analysis shows that Air France-KLM’s targets translated into an absolute emission figure could potentially not be aligned with the Paris Agreement.

Economist: Electricity demand has been flat in OECD countries despite GDP growth and new sources of demand. By contrast, demand has been rising in emerging economies. Several factors explain the divergence. These include, structural changes with advanced economies turning away from heavy industries, increased energy efficiency and catch-up in the adoption and use of electrical appliances in emerging economies.

Strategist: Our total covered bond greenium index shows that the greenium more than doubled last year, with Norwegian and French covered bonds having the largest greenium. We see potential for greeniums to rise further this year, as we expect covered bond spreads to widen, providing more room for differentiation, supporting green covered bonds

ESG in figures: In a regular section of our weekly, we present a chart book on some of the key indicators for ESG financing and the energy transition.

Air France-KLM’s SLB is a landmark for the industry, but misses absolute targets in KPI

Air France-KLM has published a Sustainability-Linked Bond (SLB) Framework, where the company commits to reduce emission intensity by 10% by 2025 and by 30% by 2030

We evaluate whether these targets are also ambitious from an absolute emissions point of view

Our analysis shows, by using different estimates for revenue ton-km and revenue passenger-km, tht Air France-KLM’s targets translated into an absolute emission figure could potentially not be aligned with the Paris Agreement

While Air France-KLM’s SLB Framework and SBTi validation of its targets is a positive step towards the decarbonization of the aviation sector,…

…we would like to have seen also absolute targets being included in the Framework.

The French-Dutch airline group Air France-KLM has published a Sustainability-Linked Bond (SLB) Framework, which is also the first one from the aviation sector. In this piece, we quickly analyse Air France-KLM’s proposed target and how it fits within the decarbonization strategy of the aviation sector.

Air France-KLM’s proposed targets

The company has naturally chosen an emission reduction target as a KPI. More specifically, the KPI is calculated by dividing the company’s scope 1 and 3 (direct and indirect, respectively) emissions, by the sum of amount of one ton of freight transported over a distance of one kilometre (or RTK) and the amount of one paid passenger transported over a distance of one kilometre (or RPK) converted into a RTK measure (hence resulting in a ‘RTK equivalent’ figure). Both RTK and RPK are standard measures in the industry. The company also discloses that the RPK figure, which is relevant as a starting point for the SLB, considers only flights operated by the Air France-KLM group, while the RPK figure currently being reported in the annual report of 2021 contains all ticket sales including bus, train and codes shares operated with other airlines. Furthermore, although the KPI does not include scope 2 emissions, these represent less than 1% of the company’s emissions. In terms of emissions, Air France-KLM has also disclosed that the emissions currently set out in the annual report do not use the Science-Based Targets initiative (SBTi) emission factor (whereas the ones reported in the SLB Framework do), which means that the reported figures will likely be restated in the annual report of 2022.

Looking at the target itself, Air France-KLM has committed to a reduction in emissions per RTK of 10% by 2025 compared to a 2019 baseline, and a 30% reduction by 2030.

The Air France-KLM target is therefore an emission intensity target. While these type of targets allow for a better peer-to-peer comparison (companies with larger scale will automatically emit more carbon emissions), IEA net zero scenarios (as well as international pledges) are based on absolute targets (that is, absolute emissions). Especially in the case of Air France-KLM, this allows the investor to properly de-attach the larger efficiency (resulting in lower emissions), from emission reductions due to lower passenger and cargo numbers. Furthermore, if both targets would have been included in the SLB Framework, this would have allowed investors to better capture (i) if Air France-KLM’s estimates on RTK and RPK growth are aligned with the IEA’s scenarios (see more on this below), and (ii) to what extent are Air France-KLM’s emission trajectory reducing accordingly to new efficiency measures (such as improvements in the development of sustainable aviation fuel, whose availability can still be uncertain).

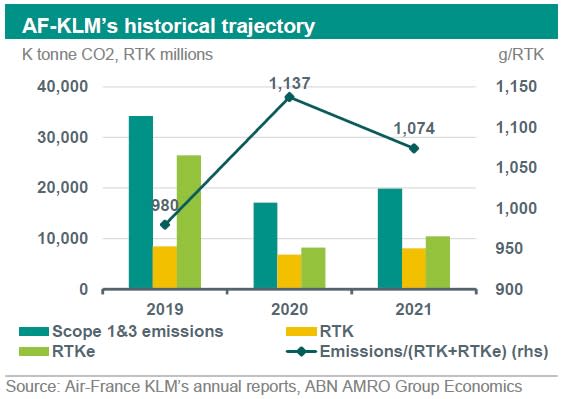

Based on this, we have tried to estimate whether in absolute terms, the Air France-KLM’s targets could also be seen as ambitious or whether the decarbonization could be solely due to an increase in the RTK and RPK figures. For that, we first use the available information (as per the annual report, which does not completely match the methodology applied in the SLB) to try to replicate Air France-KLM’s decarbonization pathway. The chart on the next page shows the historical emissions as well as the RTK and the RPK (translated into a RTK equivalent – or RTKe - figure assuming one passenger has 90kg) using annual report figures.

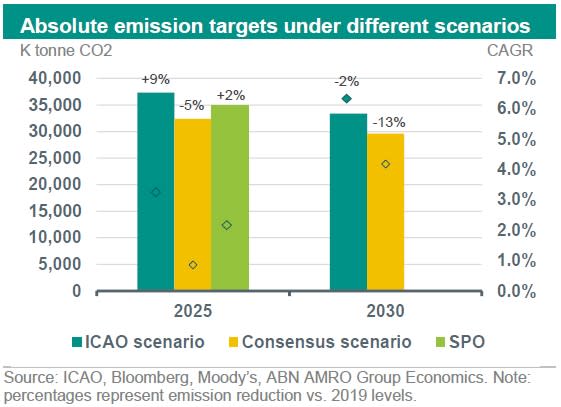

We start our analysis by using the International Civil Aviation Organization (ICAO) estimates for annual compound growth (CAGR) for RTK and RPK in order to arrive at a RTK and RTKe figure for the target years. ICAO currently estimates an annual growth of 2.6% and 3.5% for RPK and RTK, respectively, during the period of 2018-2028. For the period of 2018-2038, it predicts a growth of 3.3% and 3.4%, respectively. We use the same figures for our 2025 and 2030 estimate. This leads us to a CAGR for a combined RTK and RPK of 3.3% and 6.3% for the years of 2025 and 2030, respectively. Based on our findings for RTK and RTKe, we can therefore translate this figure to an emission estimate assuming Air France-KLM’s emission intensity targets as per the SLB (10% and 30% reduction targets for 2025 and 2030, respectively, applied to our estimates of 2019 emission intensity as shown in the graph above). Hence, under such scenario, the company’s emissions could still stand a whopping 9% above 2019 levels for 2025, easing thereafter for a 2% decline by 2030 (see chart below). This ultimately means that under these growth estimates, Air France-KLM’s targets could not necessarily involve operational efficiencies, but rather increase in RPK and RTK figures due to more flight movements. For example, if flight occupancy increases, then RPK should also increase, but emissions would stay the same.

Another potential scenario we can run is by using Air France-KLM’s equity analyst’s consensus for RTK and RPK in 2025 and 2028 (there is no consensus for 2030). In this case, analysts seem to be more conservative than the ICAO, and estimate a CAGR of 0.9% for 2025 and 4.2% for 2028, from 2019 levels. Using again Air France-KLM’s reduction targets, this would lead to an emission reduction of 2% by 2025 (vs 2019 levels) and of 13% by 2030. Clearly, under this scenario, the market is not expecting the company to easily meet their 2025 and 2030 targets, and to do so, the company would need to significantly reduce emissions and apply therefore strong operational efficiency measures.

Finally, we note that the Second Party Opinion (SPO) states that “in the case of Air France–KLM Group, the absolute greenhouse gas emissions are still likely to be 2% above 2019 levels by 2025”. Translating that back to a CAGR figure, this would mean that Air France-KLM is itself predicting a CAGR of 2.1% by 2025 from 2019 – which is lower than the ICAO figure but also significantly higher than the consensus.

Below, we try to assess whether these absolute targets fit within the IEA’s net zero estimates.

Decarbonization of the aviation sector as per IEA

The aviation sector is important for the ambition to reach net zero by 2050. It accounts now for only around 2.5% of global CO2 emissions, but this share is expected to increase as other sectors decarbonize. Hence, in a net zero scenario, aviation is expected to remain one of the main net emitters. Emissions are hard to reduce in the sector given the lack of alternative technology and the limited availability of sustainable fuels.

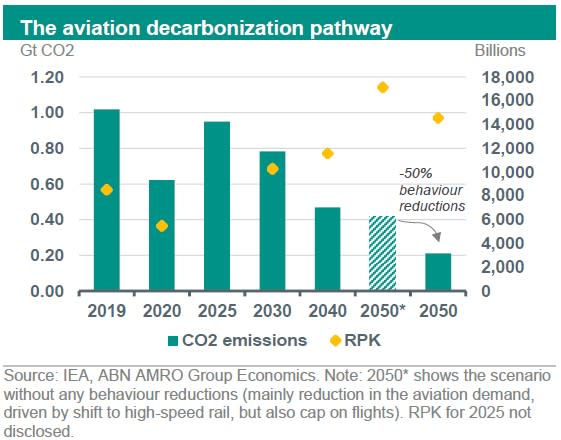

As a result, for a net zero scenario where emissions are aligned with the 1.5 degree temperature rise as per the Paris Agreement, the aviation would also have to heavily rely on a reduction of demand growth. As shown in the chart below, even if all potential efficiency measures are in place by 2050 (such as sustainable aviation fuel), demand would still need to shrink to ensure that the sector performs accordingly to the 1.5 degree pathway. Without such demand shrinkage, emissions in 2050 for the aviation sector would be around 50% higher than what is required under the 1.5 degree scenario.

Based on the chart above, we can estimate that according to the IEA, (i) CAGR for RPK between 2019-2030 needs to be around 1.7%, which is significantly lower than ICAO (6.3%) and equity analyst (4.2%) estimates, and (ii) emissions need to reduce by around 7% by 2025 and by 23% by 2030 (vs 2019 levels). While Air France-KLM’s targets are aligned with a well-below 2 degree pathway, but not a 1.5 degree pathway (as verified by SBTi), clearly the SLB’s targets translated into an absolute emission figure does not seem to align with the Paris Agreement.

All in all, we would like to reinforce the importance of having more KPI target transparency in terms of what part of the carbon intensity reduction is being driven by behaviour changes (lower demand growth rates) and what is being driven by lower absolute emissions. Within KLM’s action plan to achieve the pre-defined targets, the company focuses mainly on (i) renewal of fleet towards more lower emitting aircrafts; (ii) the use of sustainable aviation fuels, and (iii) operational efficiency, through favouring direct trajectories and applying limit fuel consumption. As all measures are exclusively focused on the efficiency measures rather than behavioural changes (which we acknowledge might not be in the company’s control), we would particularly deem an absolute target to be perhaps more appropriate.

Finally, we would like to mention that there is an urgent need for decarbonization of the aviation sector, and Air France-KLM’s SLB Framework and SBTi validation is a positive step towards airline companies taking more responsibility. Both should also trigger more transparency in terms of emission reporting. Clearly, the SLB indicates a landmark and we hope it encourages other airline peers to follow Air France-KLM’s steps.

Air France-KLM’s proposed SLB: a 25bps step-up or 75bps premium at maturity could not be enough

The company currently has 5 (sub)benchmark size euro bonds outstanding, being two in convertible format and 3 are callable bonds. The new SLB is expected to be in a dual tranche format, with maturities in 2026 and 2028. Air France-KLM’s existing 2026s callable bond currently trades at z+410bps credit spread, which would translate to an estimated coupon of between 7-7.5%. Hence, if we assume a 75bps (=0.75%) of premium at maturity for the 2026 bond in case the issuer does not meet the KPI, this would imply a mere 10% of the total annual coupon or 3.5% of the total coupon paid over the lifetime of the bond, which seems to be a low penalty for not meeting emission targets. Our calculations show that the average of potential penalty over the annual coupon rate for euro SLBs is currently 16%, which would imply that the ‘standard’ 75bps of premium at maturity (and correspondingly the 25bps as coupon step-up for the remaining 3 years of the 2026 SLB) could not be seen as ambitious enough. We therefore believe that since Air France KLM’s new bonds are expected to carry a high coupon, investors should demand also a higher financial penalty (such as a step up) in the new SLBs.