Spotlight - Oil and gas update

Impact of events in the Middle East on oil prices will depend mainly on reaction OPEC+.

The effect of the conflict in the Middle-East on the oil and European gas prices remains limited, however potential escalations could evoke large geopolitical risk premiums

Effects on oil prices depends mainly on OPEC+ reaction to any emerging developments

Given the large deal of ambiguity, we adopt ‘no-escalation’ scenario until we have more clarity

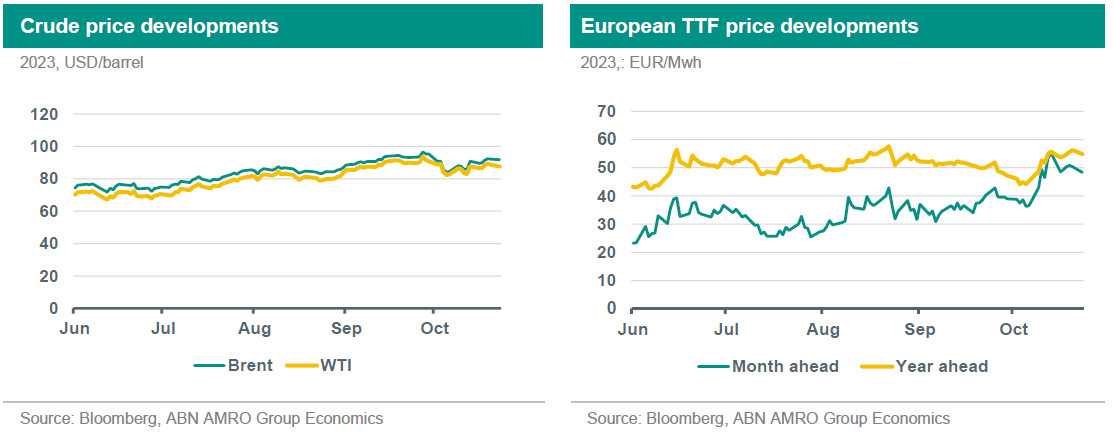

In the oil market, the 3-month upward trend in oil prices encouraged by the extension of voluntary cuts by Saudi Arabia and Russia was ended by the market reaction to the “higher for longer” monetary policy and demand erosion in Europe and the US. Prices were back to well below 85 USD/b for Brent. However, the geopolitical risks from the rise of the conflict in the Middle East between Israel and Hamas triggered a renewed rise in oil prices, which was initially small, but as the escalation continues the risk premium is getting larger. The premium is fuelled by fears that the conflict could spread to other countries in the region, such as Iran, which could lead to supply disruptions of Iran’s oil supply either directly or through the reinforcement of US sanctions. If Iran got involved in the war, oil markets will not only witness a supply reduction, but there is also a risk of a potential retaliation attacks or sabotage to cargos in the Persian gulf. In any scenario, final effects on prices would rely mainly on whether there would be any cuts revisions by OPEC+ leading members or not. Therefore, a key aspect to watch in the coming weeks is how Saudi Arabia would react to the emerging developments.

European gas markets remain tight and sensitive to any development in LNG markets even with storage reaching 98% of full capacity, as the heating season arrives. The TTF price witnessed a weekly increase reaching 40% driven by three simultaneous events, namely: the reiteration of union strikes in Australia, damages to the undersea pipeline and communication cables between Finland and Estonia in the Baltic sea, and the ongoing conflict in the Middle East. The co-occurrence of these events makes it hard to single out the driver having the biggest impact.

Israel has two main gas fields, Tamar and Leviathan, that serve the domestic market and export to neighbouring countries, such as Egypt. Egypt in turn exports LNG to Europe, which accounted for 4% of EU LNG imports in 2022. Since the start of the conflict, Israel halted production in the Tamar field, which accounts for half of its production according to IEA data, on the back of safety concerns. The causal link and impact on the TTF price will be dependent on the conflict duration. The short term impact are hard to single out because Egypt has its own fields that could be used to maintain the flow of LNG exports to Europe. However, the effect in the long term is to put more upward pressure on prices as winter demand starts to rise.

We think that there is a large deal of ambiguity on the situation will evolve in the Middle-East to infer any change in our outlook. Thus, we adopt the no-escalation scenario until we have more clarity of the situation. Accordingly, our outlook for Brent remains to average around 90 USD/barrel for the rest of 2023, and 95 USD/b for 2024. For TTF, the average year ahead price of 55 EUR/MWh for the second half of 2023, and 60 EUR/MWh for 2024.

This article is part of the Global Monthly October 23