PPAs…a key piece in the transition puzzle

Power Purchase Agreements (PPAs) are instrumental in mitigating the market risk for renewables development and pushing the transition forward. PPA contracts can be differentiated in term of the off-taker type and the party baring the output volatility risks.

Cumulatively, corporations have announced 220 gigawatts of clean energy PPAs since 2008 globally

Contracted PPAs increased in the EU by 40% in 2023 compared to 2022. In total, the EU contracted 16 GW of PPAs in 2023, Spain and Germany lead this increase, supported by demand from the IT industry

The European average PPA price for 10-15 years contracts is around 76€/MWh

PPAs can help ameliorate the international competitiveness of EU. However, the European PPA market still lags behind that in the US partly due to differences in financial conditions

Several regulatory measures could help the EU PPA market reach maturity. Those relate to standardization of PPA contracts, pooling supply and demand, the development of hybrid PPAs, and the minimization of market distortions by subsidy programmes

Introduction

A key pillar of the transition is the rollout of renewables and alternative fuels such as green hydrogen. However, investment decisions in these technologies are associated with uncertainties that weaken the viability of their business case, inducing lower investment levels and threatening the timely achievement of transition goals.One of the important uncertainties for any investment is the stability associated to future revenues needed to recover initial and operating costs. For renewable investments, the volatility of electricity prices is a prominent uncertainty to tackle as it affects adversely the financing costs of these projects. Alleviating or mitigating this uncertainty would increase the bankability of renewable investments and reduce borrowing costs. In that regard, governments could provide subsidies or guarantees that target merchant risk which would help in boosting the transition going forward. This could be in a form of Contracts for Difference (CfD), where the government provides a guarantee for a minimum electricity price for a certain period of time, ensuring the profitability of renewable investments. Alternatively, Power Purchase Agreements (PPAs), by which a potential off-taker (buyer) agrees to buy the generated electricity (partially or completely) from a developer at a certain agreed price, which alleviates the exposure to spot electricity markets. Accordingly, PPAs are instrumental in mitigating the market risk for renewables development and pushing the transition forward.

In this note, we discuss the structure of European electricity markets, the different types of PPAs, their current market, and their role boosting competitiveness and in catalysing renewable investments.

European electricity markets

Most European electricity markets have switched from a vertically integrated structure, with one company owning and managing the production, transmission, and distribution of electricity, towards a decentralized specialized structure, separating the market into generation, transmission, and distribution. Generators uses different technologies to produce power and sell their output in a wholesale market. Transmission is usually governed by one entity for the high-voltage network, called Transmission System Operator (TSO), while low voltage networks are usually operated via several regional companies, so-called Distribution System Operators (DSOs). Finally, the retail market is normally highly competitive with several utilities buying power from the generators, paying gird fees, and offering electricity to final consumers.

The wholesale market is chartered by different types of generators that bid their output at a certain price. Dispatched generators usually follow a merit order based on the cost of generation. The plant with the offer at which total supply meets the demand in a certain time is called the marginal plant. The price offered by the marginal plant become the clearing price, which is received by all dispatched plants.

Gas power plants are usually the main setters for electricity prices in many European countries. Indeed, 63% of the hours in 2022 were actually set by natural gas generators. Accordingly, during the recent energy crisis, electricity prices witnessed high volatility following the disruptions in gas supplies to the EU. The EU responded to the crisis by relying more on LNG imports, along with diversifying gas suppliers and investing more in renewable resources. Accordingly, with the absence of sufficient flexible capacity, fluctuation in power prices are expected to stay as the share of intermittent resources in the power mix increases, natural gas will keep playing an important role in electricity spot markets. Furthermore, with the current bottlenecks in the limited grid capacity, negative prices and curtailment rates for renewable power are increasing, which in turn reduces the viability of new investments. Additionally, as the share of renewable resources in the power mix increases, renewables could become more and more the marginal setting plants in the electricity markets, driving the electricity price downward. This would represent good news for consumers who suffered from high energy prices the last couple of years, but less so for renewable investors who are faced with lower profitability, making these investments less attractive to invest in.

From an investor or a financier perspective, the exposure to market risk reflected by the volatility in electricity prices represents a major uncertainty weakening the viability of the business case of such investments. Power Purchase Agreements (PPA), with potential off-takers, limit the exposure to electricity price volatility and increase the bankability of these projects.

Types of PPAs

Developers of renewable projects in Europe are starting to face the phasing out of subsidies needed to guarantee the revenue that is required to finance new projects and hedge against price and volume volatility. Signing PPAs with potential off-takers is an alternative way to secure revenues and deal with price volatility. In a PPA, a fixed price per megawatt hour (MWh) is agreed on for the electricity generated by the renewable asset. We distinguish between two main types of PPAs based on the off-taker type: utility PPAs and corporate PPAs. Utilities could enter in PPAs with renewable generators guaranteeing the purchase of output at either a fixed price or at a price indexed by the spot market. These utilities make a profit as long as the PPA price is lower than the spot price. Big corporates are widely entering into long term PPAs, so-called corporate PPAs, in order to hedge against price increases, improve budgetary planning, and meet their carbon reduction targets by satisfying their power needs via new renewable energy projects. Utilities and corporates may also enter into PPAs with existing renewable power installations. Those PPAs are especially attractive for project developers approaching the phase out of their subsidy schemes.

Corporate PPAs are usually smaller in size compared to those signed with utilities. Some corporates could also pool their demand and sign large contracts, but in general, utilities are more flexible and able to sign larger deals. Technology companies, manufacturing and communications are among the main corporates to sign PPAs, this is because of their high power demand and long term investment horizon.

On the other hand, project developers could enter in “pay as produce” or “baseload” contracts. In the former contract, the off-taker would be the one to bare the volatility in output associated to the intermittency of renewable power plants. While the generators would need to buy electricity from the market (at the spot price, which is likely to be higher than the PPA price) to deliver the agreed volume in the baseload contract, in case the renewable asset does not produce according to schedule. Alternatively, the generator could pay financial compensation of the difference between the PPA price and the spot price in case of non-delivery. Thus, under the pay-as-produce PPAs developers usually enjoy a discount in comparison to baseload contracts.

PPAs could also be differentiated by their duration. For example, PPAs could range from 6 months, for operating projects, and up to 20 years, for new projects, giving companies the flexibility to opt for the contract that match their investment timelines.

European PPA market

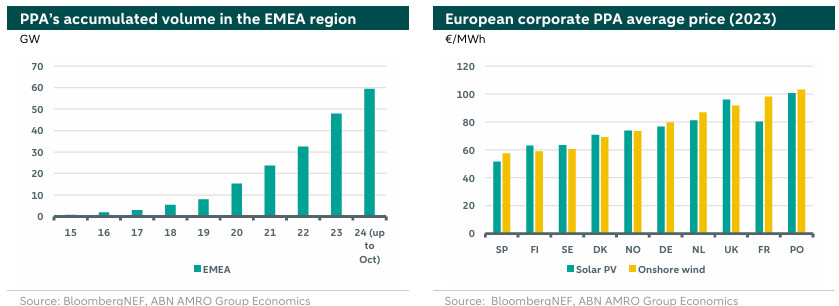

The PPA market has been around for several years now. The global volume of PPAs has been growing, with the largest increase in the Americas. Cumulatively, corporations have announced 220 gigawatts of clean energy PPAs since 2008, globally. The European market flourished after the energy crisis and the wave of European climate regulation prioritizing energy security and aiming for a smooth and fast energy transition. Accordingly, the yearly additions for PPAs have been increasing driving the accumulated volume in the EMEA (Europe, middle East and Africa) region to around 59.5 GW, as illustrated in the left hand chart below. Contracted PPAs increased in the EU by 40% in 2023 compared to 2022. In total, the EU contracted 16 GW of PPAs in 2023. Spain and Germany lead this increase supported by demand from the IT industry.

PPAs prices differ across the technologies that are used to produce renewable power. Prices differ across countries depending on the share of renewable power in the electricity mix and the level of electricity prices. Across European countries, Spain has the lowest PPA prices for Solar PV contracts, while PPA onshore wind prices in Poland are among the highest in Europe, as illustrated in the chart above. Currently, the European average PPA price for 10-15 years contracts is around 76€/MWh.

Spain has been witnessing a high penetration rate of renewables, which has been a main factor for lower PPA prices. However, declining merchant revenues pose a risk of a lower developer appetite for renewable energy development. This issue is most evident in Spain which has one of the highest share of renewable energy in its energy mix worldwide, which, along with limited grid capacity, was the main driver for a fall in power prices to a record-low day-ahead baseload average of €20.3/MWh in the second quarter of 2024.

Corporates are attracted to regions with lower PPA prices. They often choose the deals where the economics make most sense rather than the places where PPAs would have the greatest impact. This does not help the development of renewable capacity in regions already facing struggles to finance these investments. However, as expectations from corporate decarbonization increase, scrutiny on corporate PPAs will increase as well, which could result in a shift in corporate purchases toward more impact-driven PPAs.

PPAs and EU competitiveness

Mario Draghi’s report () on EU competitiveness identified high volatility and unpredictability of prices in the EU as one of the main sources of uncertainty that weaken the EU international competitiveness vis a vis its trading partners. The channel is simple: high volatility induces uncertainty, which in turn requires higher hedging costs that affect adversely investment decisions and induce supply uncertainty, raising the costs of energy transition. PPAs can help reduce these uncertainties and ameliorate the international competitiveness of the EU.

However, the European PPA market still lags behind that in the US which started earlier and is consistently at higher levels. The lag in the pick up of PPAs in the EU can be partly due the differences in financial conditions. For example, the lack of financial guarantees for counterparty risk, along with limited market risk appetite, and the absence of standardisation are some of the factors limiting the use of PPAs in the EU.

According to Draghi’s report, several regulatory measures could help the EU PPA market reach maturity. Those relate to standardization of PPA contracts, which will help in decreasing transaction costs and give accessibility to wider group of potential off-takers. Also, the mitigation of price risk, and allowing tailored structure, by pooling supply and demand and the development of hybrid PPAs, that incorporate assets flexibility. Finally, the minimization of market distortions by subsidy programmes on the PPA market.