NL Update – Q2 contraction pushes the Netherlands in a technical recession

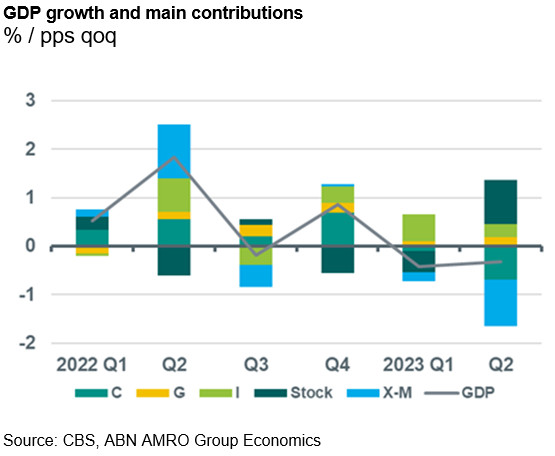

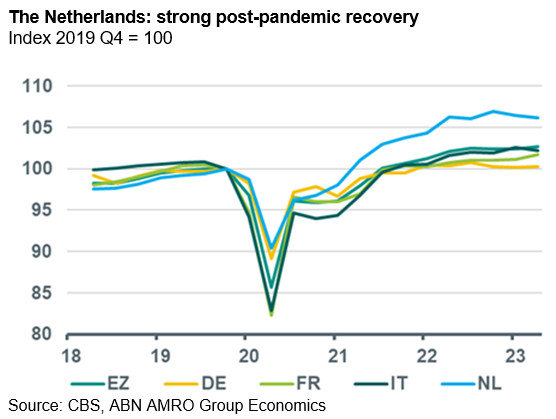

The Dutch economy contracted by 0.3% qoq in Q2. Following the 0.4% contraction in Q1, this means the Netherlands officially was in a technical recession in the first half of the year. The Dutch economy underperformed the eurozone total (+0.3%) in Q2, and the contraction in Dutch GDP was driven by weak private consumption and slumping exports. Despite the technical recession, the Dutch economy remains resilient; the labour market is still tight and bankruptcies – although increasing in recent months – are still below 2019 levels.

The Dutch economy contracted by 0.3% qoq in Q2. Following the 0.4% contraction in Q1, this means the Netherlands officially was in a technical recession in the first half of the year. The Dutch economy underperformed the eurozone total (+0.3%) in Q2, and the contraction in Dutch GDP was driven by weak private consumption and slumping exports. Despite the technical recession, the Dutch economy remains resilient; the labour market is still tight and bankruptcies – although increasing in recent months – are still below 2019 levels.

Weak external demand tipped the change in the trade balance into negative territory, with net exports contributing -1% pps to qoq GDP growth. The Dutch industrial sector, accounting for a large share of exports, has been struggling on the back of lower external demand, particularly for chemical goods. Indeed, goods exports drove the overall decline in exports while services exports continued to recover from pandemic lows. The trend of weak demand for Dutch exports is not likely to reverse course soon as the eurozone growth outlook remains subdued.

Inflation has weighed on private consumption causing it to contract by 0.2% qoq in Q1 and 1.6% in Q2. Contrary to declining goods spending, resilience in services spending prevented a stronger drop of overall consumption. Some services might still be benefitting from post-pandemic catch-up spending. We expect private consumption to grow mildly over the rest of the year with high wage growth expected to average 5.6% this year but high inflation partially offsetting this nominal gain

Despite weaker growth prospects and higher financing costs, fixed investment stood out, expanding by 1.3% qoq in Q2. Infrastructure investment, transport and machinery and sustainability related investment such as isolation, solar panels and heat pumps drove this investment robustness. Housing investment on the other hand contracted on the back of a cooling housing market.

We continue to expect growth to remain sluggish during the rest of the year as domestic demand will be increasingly hit by past and upcoming interest rates hikes by the ECB and weak eurozone growth prospects imply that external demand remains weak. We are currently revising our growth forecasts and will include them in our monthly at the end of this week. (Aggie van Huisseling, Jan-Paul van de Kerke)