Key views Global Outlook 2024

The global economy is likely to grow at a subdued pace in the near term, as high rates continue to bear down on demand in advanced economies, while China continues to face both cyclical and structural headwinds. Global trade and industry looks to be bottoming out, but a sharp rebound is unlikely while rates remain restrictive. On the positive side, inflation has fallen significantly and is now within touching distance of central bank targets. Further falls in inflation will enable central banks to pivot to rate cuts by mid-2024, and financial conditions are already easing in anticipation of this. Still, monetary policy will remain relatively tight for some time yet, and this will keep a lid on the post-slowdown rebound.

Macro

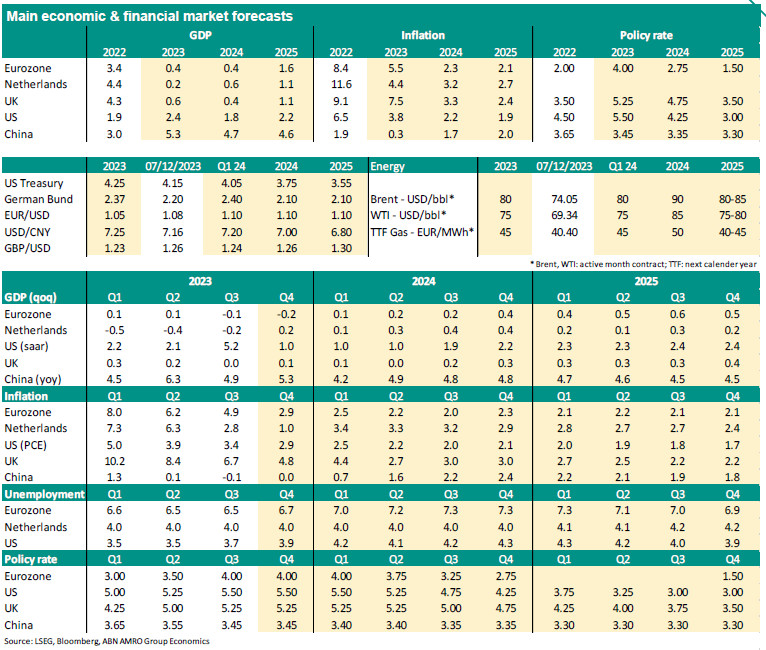

Eurozone – GDP contracted by 0.1% qoq in 2023Q3. Economic data and surveys published so far for September-November indicate that GDP probably contracted moderately again in Q4. Subsequently, we expect GDP to roughly stabilise in 2024Q1 and grow moderately, at below the trend rate, during the remainder of 2024. Only toward the end of 2024, we expect growth to strengthen and rise to above the trend growth rate. Disinflation has gained momentum, with the headline and core rate both declining markedly in the past few months. Despite somewhat higher energy inflation, HICP inflation is expected to continue to decline this year and the next. Core inflation should fall to around 2% by mid-2024.

The Netherlands – GDP contracted in the first three quarters of 2023 which means the Dutch economy still is in a technical recession. We expect growth to resume over the course of 2024 but remain sluggish in the coming quarters on the back of higher rates and lower external demand. Dutch GDP growth is expected to average 0.2% in 2023 and pick up slightly to 0.6% in 2024. The Dutch economy remains resilient; the labour market is still tight and bankruptcies – although increasing in recent months – are still below 2019 levels. We expect inflation (HICP) to average 4.4% in 2023 and 3.2% in 2024.

UK – Disinflation has continued, providing some relief to the Bank of England, but upside inflation risks remain significant given that wage growth is still elevated and well above levels consistent with the 2% target. At the same time, unemployment has started rising, and we expect a softening in demand to dampen wage growth over time. The economy is expected to broadly stagnate over the coming year or so, weighed by tight monetary policy.

US – Growth was exceptionally strong in Q3, but there is likely to be payback in Q4, with inventories set to be a drag, while consumption strength is unsustainable. We expect growth to then stay weak for the following two quarters, before easing financial conditions sets the stage for a recovery in the second half of 2024. We expect a sharp slowdown in Q4, with the risk of a contraction. Wage growth has peaked, and inflation is moving in line with expectations back to the 2% target. A recovery next year hinges on a timely pivot to rate cuts by the Fed in response to falling inflation.

China – The unambitious growth target for 2023 of 5% is within reach, but with ongoing structural headwinds we expect annual growth to fall below 5% in 2024. Beijing is stepping up support for the property sector, while shifting risks from developers to banks, but the sector’s structural downsizing will continue. Support measures should also help broadening the recovery in domestic demand, but this may take time. Exports and manufacturing should benefit from a bottoming out of global trade/industry next year. We do not expect China to enter a serious deflationary spiral.

Central Bank & Markets

ECB – The ECB kept interest rates unchanged in October. According to the central bank, policy rates now are at levels that, maintained for a sufficiently long duration, will make a substantial contribution to inflation returning to its 2% target. Although macro data continues to point in the direction of a start of a rate cut cycle over the next few months, we think it will take the Governing Council time to form consensus and change its communication Therefore, we now expect a first rate cut in June 2024, which is one quarter later than our earlier forecast. We see the deposit rate at 2.75% by the end of 2024 (2.25% previously). We think the deposit rate will eventually reach 1.5% in the course of 2025.

Fed – The FOMC has kept rates on hold since its last rate hike in July. Committee members have expressed openness to further tightening, but we think the risk of further hikes now is very low given the data flow. We now expect the Fed to start cutting rates from June, with the risk that the Fed could pivot sooner given the softening labour market and continued falls in inflation. Even with rate cuts starting next year, monetary policy is expected to remain restrictive throughout 2024 and even into 2025. We expect the upper bound of the fed funds rate to reach 4.25% by end-2024, and 3% by mid-2025.

Bank of England – The MPC kept policy on hold at the September and November meetings. We now think Bank Rate has peaked at 5.25%. However, we would not rule out one last rate hike if inflation springs another upside surprise. The BoE is in full data-dependent mode, and UK macro data has been erratic over the past year. We do not expect rate cuts until next August, and there is a risk that rate cuts get delayed even further, if inflation proves to be more persistent.

Bond yields – The ‘’higher-for-longer’’ theme have now been fully priced out by the market. Bund yield reached its lowest level since May and US treasury also continue its decelerating trend. Given our macro and central bank view, this was indeed the turn we were expecting. Looking ahead, we still forecast further weakness in economic data which should push bond yields even lower. Although, the path is unlikely to be linear. Markets are now pricing rate cuts earlier than us and we think the move in rates has come a bit too far too fast. As such, an upward revision on rates can be expected in the coming weeks.

FX – For 2024, we expect the same amount of interest rate cuts by the Fed and the ECB. In both cases, our base case calls for more substantial rate cuts than markets currently expect. The difference between our forecasts and market pricing is around the same for both central banks. So, if our views on both Fed and ECB policies play out, EUR/USD should stay near current levels. For 2025 we think that the ECB and Fed will continue to ease in 2025 by the same amount. Therefore, we expect EUR/USD to stay in a 1.05-1.10 range waiting for another driver to present itself to cause a more directional move.