Key views Global Monthly February 2024

The global economy is likely to grow at a subdued pace in the near term, as high rates continue to bear down on demand in advanced economies, while China continues to face both cyclical and structural headwinds. Global trade and industry looks to be bottoming out, but a sharp rebound is unlikely while rates remain restrictive. On the positive side, inflation has fallen significantly and is now within touching distance of central bank targets. The Red Sea disturbances are unlikely to meaningfully impact inflation, but a major escalation in the Middle East could change matters. Further falls in inflation will enable central banks to pivot to rate cuts by mid-2024, and financial conditions are already easing in anticipation of this. Still, monetary policy will remain relatively tight for some time yet, and this will keep a lid on the recovery.

Macro

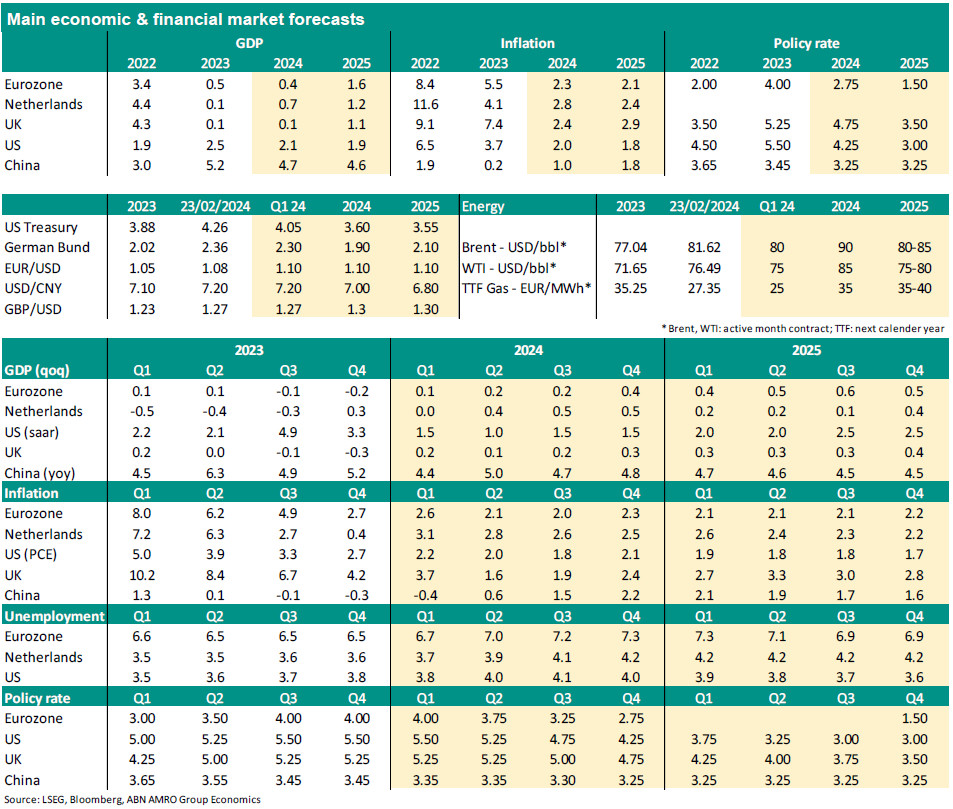

Eurozone – GDP stagnated in 23Q4. Growth has been close to zero now during five consecutive quarters, and the expectation is for another stagnation in 24Q1. GDP should expand moderately during the rest of the year, among other things because fiscal policy will be tightened. Labour market conditions have deteriorated, which will limit wage growth going forward and reduce underlying inflationary pressures. Headline and core inflation have remained on a downward trajectory moving into 2024. We expect headline and core inflation to be close to the ECB's 2% target around the middle of this year.

The Netherlands – The Dutch economy expanded by 0.3% qoq in Q4, bringing an end to three consecutive quarters of contractions. We raised our GDP forecasts to 0.7% in 2024 (was 0.5%) and 1.2% in 2025 (was 1.1%). Labour market tightness remains, but the unemployment rate will marginally rise to 4.0% in 2024. Inflation (HICP) continues trending downward to average 2.8% this year, down from 4.1% in 2023. Formation talks recently stalling, which delays the forming of a new government and adds to policy uncertainty.

UK – Disinflation has continued, providing some relief to the Bank of England, but upside inflation risks remain significant given that wage growth is still elevated and well above levels consistent with the 2% target. At the same time, unemployment has started rising, and we expect a softening in demand to dampen wage growth over time. The economy is expected to broadly stagnate over the coming year or so, weighed by tight monetary policy.

US – Growth slowed in Q4 following an exceptionally strong Q3, but remained well above trend. The recent strength in inventory build makes the economy vulnerable to a sharp slowdown in coming quarters. We also expect a slowdown in consumption given the cooling labour market and a reduced tailwind from excess savings. We expect weak growth in the next few quarters, before easing financial conditions set the stage for a recovery later in 2024. Wage growth has peaked, and inflation is moving in line with expectations back to the 2% target. A recovery next year hinges on a timely pivot to rate cuts by the Fed in response to falling inflation.

China – Recent data still paint the picture of an uneven recovery – with ongoing headwinds from property, and with the supply side still stronger than the demand side. CPI inflation turned deeper into the red in January, but LNY holiday data showed some green shoots. In line with our expectations, Beijing continues with piecemeal easing and targeted support. The PBoC cut banks’ RRR and the 5-yr LPR this month; we expect more mini rate cuts to follow. Meanwhile, the expansion of the PBoC’s balance sheet is partly a result of the use of a targeted lending facility.

Central Banks & Markets

ECB – The ECB kept policy rates unchanged in January. Although it struck a more optimistic tone on inflation, we still expect the rate cut cycle to begin in June. Indeed, the account of the January meeting mentions that ‘it was affirmed that further progress needed to be made in the disinflationary process before the Governing Council could be sufficiently confident that inflation was set to hit the ECB’s target in a timely manner and in a sustainable way’. Therefore we still expect a first cut in June. We think the deposit rate will eventually be reduced to 1.5% in the course of 2025.

Fed – The FOMC has kept rates on hold since its last rate hike in July. We expect the Fed to start cutting rates from June, with the risk somewhat tilted to earlier cuts. Even with rate cuts starting next year, monetary policy is expected to remain restrictive throughout 2024 and even into 2025. We expect the upper bound of the fed funds rate to reach 4.25% by end-2024, and 3% by mid-2025. The Fed also looks set to wind down its quantitative tightening somewhat sooner than previously expected, though this will be well telegraphed and gradual.

Bank of England – The MPC kept policy on hold at the September and November meetings. We now think Bank Rate has peaked at 5.25%. However, we would not rule out one last rate hike if inflation springs another upside surprise. The BoE is in full data-dependent mode, and UK macro data has been erratic over the past year. We do not expect rate cuts until next August, and there is a risk that rate cuts get delayed even further, if inflation proves to be more persistent.

Bond yields – Following recent macroeconomic data releases (particularly in the US) and central bank officials’ speeches, the financial market started to retrieve gradually from its extensive policy rate cuts for 2024. The market priced out as much as 60bp of cuts for the ECB and about 75bp for the Fed by the end of this year. Indeed, the market has now delayed its first rate cut to June, which is in line with our rates forecast. Indeed, as we expected, the pricing out of extensive rate cuts occurred which means that we expect bond yields to soon start their way down again. We expect the declining trend to be the steepest as we approach the month of June and to keep this trend for the rest of the year across all maturities.

FX – For this year we expect expectations for Fed/ECB policy to continue to drive the direction in EUR/USD. The market expects both the Fed and the ECB to start its easing cycle in April/May and rates to be reduced to 4% for the Fed and 2.5% for the ECB by the end of 2024. We expect the easing cycles to start later, in June, and the Fed to arrive at 4.25% and the ECB at 2.75% at the end of the year. So, both for the Fed and the ECB we are somewhat less dovish than the market and the difference with the market is roughly the same. Therefore we expect EUR/USD to stay around 1.10 for the time being.