Key views Global Monthly 26 March 2025

US tariff threats have surprised even our pessimistic expectations, with the most important announcement still to come on 2 April. China, the EU and the US’s neighbours are expected to bear the brunt. For the eurozone, a new upside risk comes from likely significant increases in defence spending, and in Germany new infrastructure spending. This will blunt the impact of tariff rises. Global trade and growth are also initially benefiting from a frontloading ahead of tariff rises, but a sharp slowdown is expected later in 2025. Domestic demand is in the meantime recovering in the eurozone and China, helped by falling interest rates, and in China, targeted fiscal measures. Inflation in the US is expected to reaccelerate, but to fall below target in the eurozone. This is likely to drive a divergence in Fed & ECB policy, with Fed policy staying on hold from here, and the ECB continuing to cut rates.

Macro

Eurozone

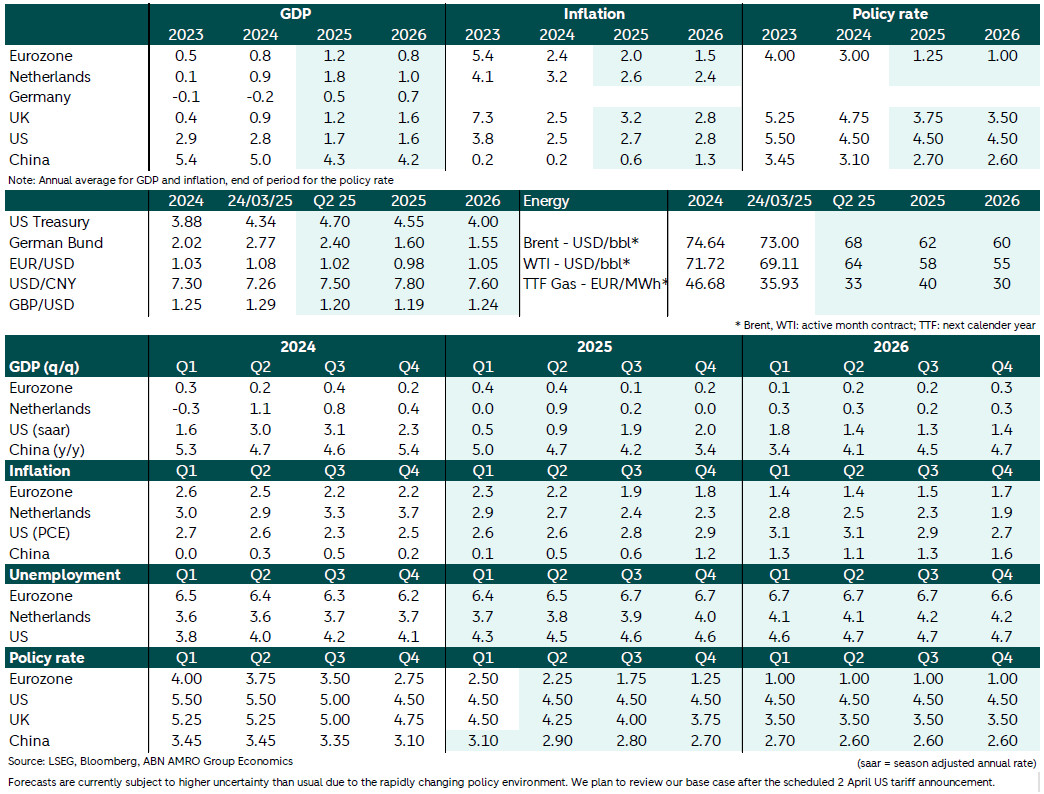

The eurozone recovery is continuing, helped by rate cuts and real income gains supporting consumption. Tariff threats suggest the downside risks have grown, but upside risks are coming from expansionary fiscal policy. We will update our forecasts once trade policy changes become more concrete in early April. In the first half of 2025 frontloading effects are likely to boost quarterly growth, and we are seeing some early signs of this in the PMIs. Afterwards, we see growth and inflation negatively impacted, as tariffs are implemented, and in 2026 inflation is expected to undershoot the 2% target.

The Netherlands

After recovering in 2024, growth is expected to recover further into 2025, before slowing on the back of US import tariffs. Given external uncertainty, growth will be domestically driven and will average 1.8% in 2025, and 1.0% in 2026, compared to 0.9% in 2024. Unemployment will increase slightly, but the tight labour market remains a constraining factor. Inflation is expected to stay above the 2% target in the coming years, mostly driven by still-high wage growth, rent increases, and product-specific tax changes.

UK

The government’s expansionary fiscal stance, alongside rising real incomes, is likely to keep the economy on a recovery path for now, but structural challenges remain. The UK is less vulnerable to potential US tariffs than the eurozone as it is less export dependent, and the US administration has hinted that the UK may get an exemption from tariffs. Services inflation is stubbornly high, with wage growth still well above levels consistent with 2% inflation. A sustained return to 2% inflation will take longer than elsewhere, due to historically higher inflation expectations in the UK.

US

Growth and consumption are likely to slow down on the back of a strong decline in consumer sentiment, caused by significant policy uncertainty. A gradually cooling labour market and pockets of financial stress among households are likely to contribute to a slowdown in growth into 2025. Tariffs will be a further drag on growth in the course of this year, whilst also raising inflation. On the basis of current developments, our 2025 growth is downgrade to 1.7%, with a further revision likely following the April 2nd tariff plan. The tariff impact implies average PCE inflation of 2.7% in 2025, rising to 2.8% in 2026.

China

The economy shows some resilience, just as new US tariffs have been levied. February PMIs and the latest monthly activity data came in stronger than expected. However, the supply side remains stronger than the demand side, property is still a drag on growth, deflationary pressures remain, and the unemployment rate picked up. Beijing reaffirmed its commit-ment to step up fiscal stimulus, and announced new plans to support consumption. We see both upside (resilience so far, more stimulus) and downside (more tariffs in April) risks to our growth forecasts, which we will review next month.

Central Banks & Markets

ECB

We expect the ECB to hold rates steady in April as uncertainty over tariffs as well as policy rates approaching the ECB’s assessment of neutral are reason to adopt a wait-and-see approach. A pause has also been signaled by some on the Governing Council, though market pricing suggests it is a close call. As tariffs hit growth and inflation, we see the ECB resuming its easing cycle at the June meeting, and cutting rates by more than markets currently price. When we have updated our macro projections after trade policy changes become concrete, we will also update our view on the ECB.

Fed

After the December rate cut, the Fed’s upper bound on fed funds rate stands at 4.5%. With relatively hot inflation readings in the start of the year, inflation is unlikely to come down sufficiently to ease , especially considering a new impulse from tariff policy. Risks to inflation and the labour market are currently roughly in balance, but likely to tilt to inflation in the second half of the year. Therefore, the Fed keeps rates at the current, restrictive, level indefinitely, hedging against politically sensitive policy mistakes.

Bank of England

The MPC kept Bank Rate on hold at 4.5% in March, in line with our expectations. Incoming data suggests stubbornly high underlying inflationary pressure, and sticky wage growth. The government’s expansionary fiscal stance, alongside continued elevated wage growth, poses upside risks to medium-term inflation. This is likely to keep rate cuts at a more gradual pace than for the ECB. We expect three more 25bp rate cuts in 2025 with the next cut expected in May. Bank Rate is expected to settle at 3.5% in early 2026.

Bond yields

Trump’s statements continue to weigh on European rates. Over the past weeks, EU defence spending has become the new investors’ concerns in the EGB market. This development suggests that EU countries may need to increase government spending, likely financed through higher deficits and, consequently, increased borrowing requirements. As a result, higher bond issuance anticipation shifted the longer end of the curve higher, and this may continue if no joint EU debt debt issuance deal is found by the EU member states.

FX

In recent weeks the US dollar has weakened and the euro has rallied. EUR/USD rallied to a high of 1.0955. The main reasons behind this move have been 10y rate differentials between Germany (after the budget announcement) and the US moving in favour of the euro and the market shying away from the US dollar due to policy uncertainty. Our forecast for EUR/USD at the end of 2025 stands at 0.98 based on monetary policy differences between the Fed and the ECB.