Key views from the Global Monthly February 2022

The post-pandemic recovery is regaining momentum, with above trend growth to resume in the eurozone and the US following the Omicron-induced soft patch. However, uncertainty over the economic outlook remains the highest it has been since the start of the pandemic in early 2020. While economic growth has been strong, as economies have largely opened up, the supply-side has struggled to keep up with resurgent demand, with the consequence being inflation. This has brought forward the timing of interest rate rises in the US, with the Fed expected to begin raising rates in March. The ECB has meanwhile signalled a pivot to policy normalisation, and we now expect rates to start rising in December. Europe will also continue to feel the global spill-over effects of tighter US monetary policy over the coming year, pushing bond yields higher and ultimately dampening growth.

Macro

Eurozone

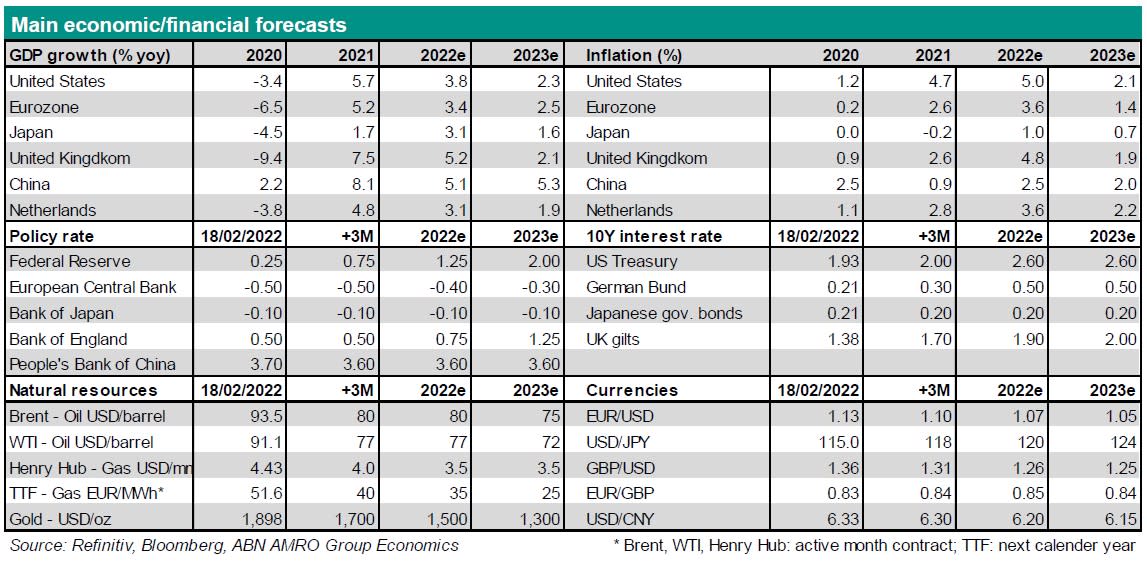

The economy is going through a soft patch, with modest growth in 2021Q4-2022Q1. Supply side bottlenecks and record-high (energy price) inflation are restraining growth, even after the lifting of Omicron-related restrictions. Growth is expected to rebound sharply in 2022Q2-Q3, but should return to a more normal cyclical path thereafter. It should slow down toward the trend rate in the course of 2023. Inflation is likely to stay elevated in the first half of 2022 but should drop below the ECB target in the final months of the year. Wage growth at the eurozone level is still subdued. It is expected to strengthen during this year and the next, but the impact on underlying inflation should be buffered by rises in labour productivity.

Netherlands

Q4 growth surprised to the upside. Instead of our expectation for a mild contraction, GDP expanded in Q4 by 0.9% qoq. Annual growth therefore came in at 4.8%. The strong Q4 reading carries over to 2022 growth. Together with the government’s announcement to lift all restrictions, we have upgraded our growth forecasts for 2022 from 2.6% to 3.1%. This above trend growth however faces several constraints. Most notable are the notoriously tight labour market and supply bottlenecks. Inflation is expected to average at 3.7% in 2022, with upward price pressures from energy and supply bottlenecks gradually fading over the coming year.

US

Above trend growth is resuming after the Omicron soft patch of late 2021. However, elevated goods consumption and tightness in the labour market is continuing to put upward pressure on inflation. Wage growth has surged in recent months, raising the risk of a wage-price spiral taking off. While we expect above-trend growth to continue throughout 2022, growth is likely to slow to below-trend rates in 2023, on a combination of fading post-pandemic catch-up effects, weaker government spending following the failure of Biden’s Build Back Better plan, and tighter monetary policy.

China

We expect qoq growth to fall back in Q1, with drags from real estate and strict covid-19 policy remaining. Due to Omicron, the shift from 'zero cases’ to 'dynamic clearing’ has been less supportive for consumer services than was hoped for. We expect qqq growth to pick-up in the course of 2022. We think yoy growth bottomed at 4.0% yoy in Q4-21 and will accelerate to around 5.5% yoy in 2H-22. That would leave full-year growth for 2022 at 5.1%. Our expectation of improving momentum is partly based on the assumption that Beijing will continue with targeted, piecemeal monetary and fiscal easing and a relaxation of macroprudential regulations, including for real estate.

Central Banks & Markets

ECB

After the February Governing Council meeting, ECB President Lagarde sounded surprisingly hawkish, signalling that the central bank will reduce policy accommodation this year. As a result of the ECB's pivot we now think that a tapering of the APP will be announced in March, with net purchases ending altogether in September. We expect APP to average EUR 30bn in Q2 and EUR 15bn in Q3. We have also pencilled in a 10bp deposit rate hike in December of this year and an additional one in March 2023. After that, we expect rate hikes to be aborted, or at least put on ice, with the deposit rate at -0.3% by the end of 2023. We think there is a non-negligible probability that the window of opportunity for a rate hike might close before the end of the year.

Fed

Given persistently elevated inflation in the US, and upside risks to the outlook, we expect the Fed to begin hiking rates by 25bp in March. Thereafter, we expect three additional hikes this year and in 2023. This would take the target range of the fed funds rate back to the pre-pandemic level of 1.5-1.75% by mid-2023. The risk continues to be for an even steeper path of rate hikes. Shortly after lift-off, we expect the Fed to begin unwinding its balance sheet in late Q2, initially at a gradual pace, but eventually for this to run at $60bn per month. There is a significant risk that the Fed reduces the balance sheet at a much faster pace, potentially using it as a tool in its fight against inflation.

Bond yields

Given that we forecast the Fed funds rate to be at its eventual peak of around 2.50-2.75% by end 2025, we expect longer term yields will move higher in 2022, with the 10y US Treasury yield settling at around 2.6% at year-end. Once we move closer to the first rate hike, which we have pencilled in for March, we expect the US Treasury curve to bear flatten. Our new ECB forecasts have made us revise our forecasts for 10y Bund yields higher (to 0.5% at end-2022), although we do think that the market is already quite advanced in pricing in two 10bp rate hikes and the ending of APP. The rise in US yields will also put further upward pressure on their European counterparts.

FX/EURUSD

Following the ECB meeting, we changed our ECB view. We now expect a modest rise in the deposit rate from the end of this year We originally didn’t have any hike in the deposit rate in our forecast horizon. Financial markets are pricing in more aggressive rate hikes for both the ECB and the Fed than we have. We think that if our view proves to be correct then that the euro still weakens versus the US dollar this year and next year. But it is likely that the overall size of the move is smaller than we originally had. Therefore, we have changed our forecasts in EUR/USD. Our new forecast for end 2022 is 1.07 (was 1.05) and for end 2023 1.05 (was 1.0).