Housing Market Monitor - Lower interest rates, higher wages; housing market back on track

The affordability improves this year due to higher wages and falling mortgage rates. The number of homes for sale remains low and falls again as homes sell faster. New construction sales recover and could potentially help flow and transactions. Starters and singles are helped in part by new lending standards and fiscal changes.

ABN AMRO Group Economics

Author has left Group Economics, see text

This article was written by Bram Vendel

The housing market is rebounding. The outlook and expectations for price development are a lot more positive. Prices have been on the rise again since last summer as mortgage rates have come off after a period of stabilization and incomes are rising fast. Falling inflation is putting less pressure on disposable income. We expect mortgage rates to fall over the course of this year as a result of expected central bank interest rate cuts. Combined with further increases in wages, this will help improve affordability. In a tight market, with improved affordability, home prices can continue to rise. We raise our estimate for 2024 from 2.5% to 4%. In 2025, house prices are expected to rise further by 3.5%.

We also adjust our estimates for the trend in the number of transactions upward from -2.5% to 0.5% in 2024. In 2025, transactions are expected to increase by 3%. With rising home prices and lower interest rates, unlike last year, sellers will be more inclined to buy a new home before selling the old one. This will ensure a faster selling time and, as a result, a higher number of transactions. The increase is limited, however, because few new homes are being built. Continued problems in new construction are keeping supply behind demand. The number of new homes completed this year and next will remain well below the ambition of 100,000 homes targeted by the government. As a result, more households will struggle to find suitable housing. The lack of new construction pressures the flow-through of housing, which keeps the number of transactions low on balance.

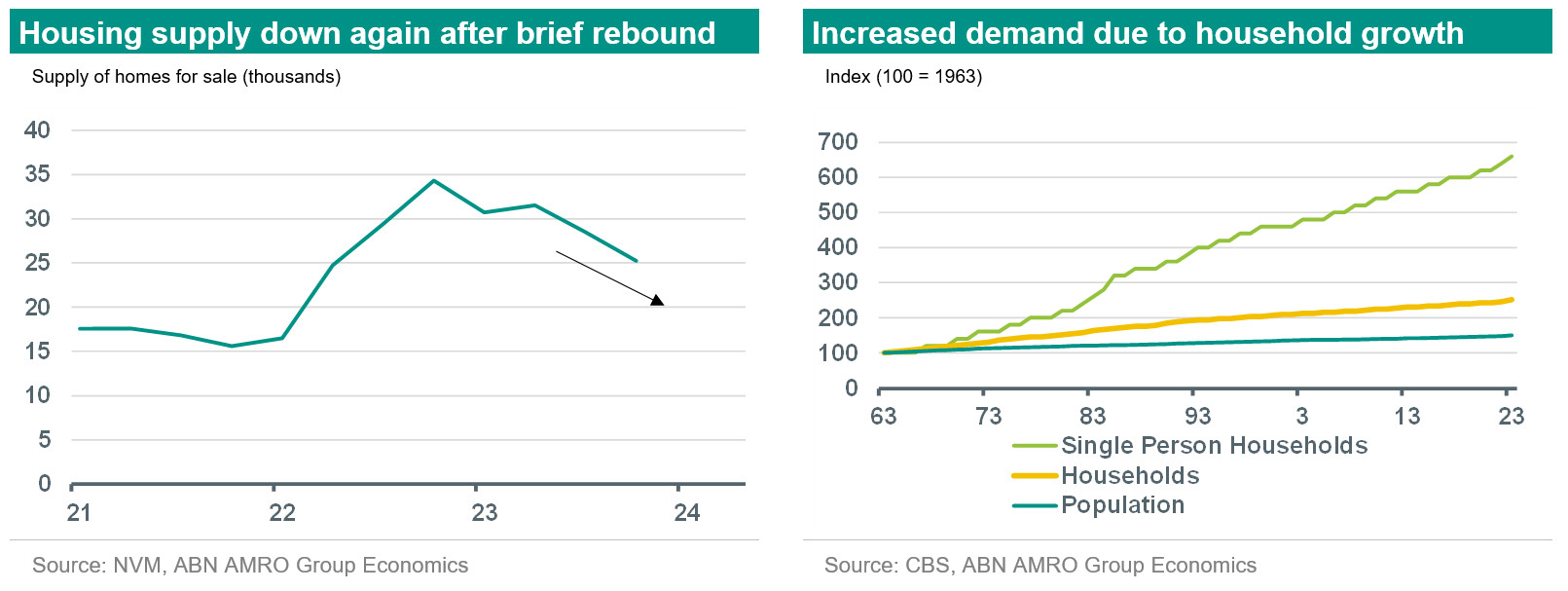

The number of homes for sale is falling again. Interest among buyers has increased and is manifesting itself in firmer competition. As a result, selling time is decreasing and the inventory of homes for sale is shrinking. In a tighter market, potential buyers may take less time to consider buying a home and will be more likely to bid up against each other. With increasing tightness, potential buyers have fewer choices in the housing market. Also, homes will again more often be sold above the asking price and, in the deflected process, the average selling price will also continue to rise.

Number of homes for sale drops again

The housing market has turned around. There are fewer and fewer homes for sale and it is becoming increasingly difficult for home buyers to secure a suitable home. According to the , there were 25,232 homes for sale in the fourth quarter of 2023. This is 9,088 (26%) fewer than in the last quarter of 2022. Compared to the historical average supply since 1995, of 73,000, the current supply is very limited, but not yet as low as at the end of 2021 when there were only 15,000 homes on offer. In 2022, supply rose as buyers took a pass because of the combination of rapidly rising mortgage rates and high inflation. Since then, the situation has changed.

One reason there are fewer and fewer homes for sale is that those who want to move on to another home are more likely to dare to buy a new home before selling the old one. When house prices fell, the risk arose that the old house would not sell quickly enough, or for a lower amount than previously estimated. This led to uncertainty among move-up buyers about the cost of the bridging period and the sale price of the home. Now that competition among buyers has increased again and the price trend is positive, sellers are more confident and more likely to purchase a new home. Partly as a result, the average home selling time has also been declining for . In the last quarter of 2023, homes were sold within an average of 30 days.

The number of homes for sale continues to decline due to increased tightness in the housing market. The tightness occurs because the population is growing rapidly, but also because the total number of households has been growing faster than the population for a long time. In 60 years, the total number of households more than doubled, while the population only grew by 50 percent. This was mainly due to the increase in the number of single-person households. With an ongoing aging population, less couple formation and an increased risk of divorce, the number of single-person households has increased more than sixfold. Annually, the number of single-person households grows by a factor of 10 higher than the population. This so-called household thinning leads to a structural shortage of housing if new homes cannot be built at the same rate. by ABF Research show that the housing shortage will reach 390,000 homes in 2025 and that the shortages will persist until at least 2050.

Transactions under pressure, but short-term outlook good

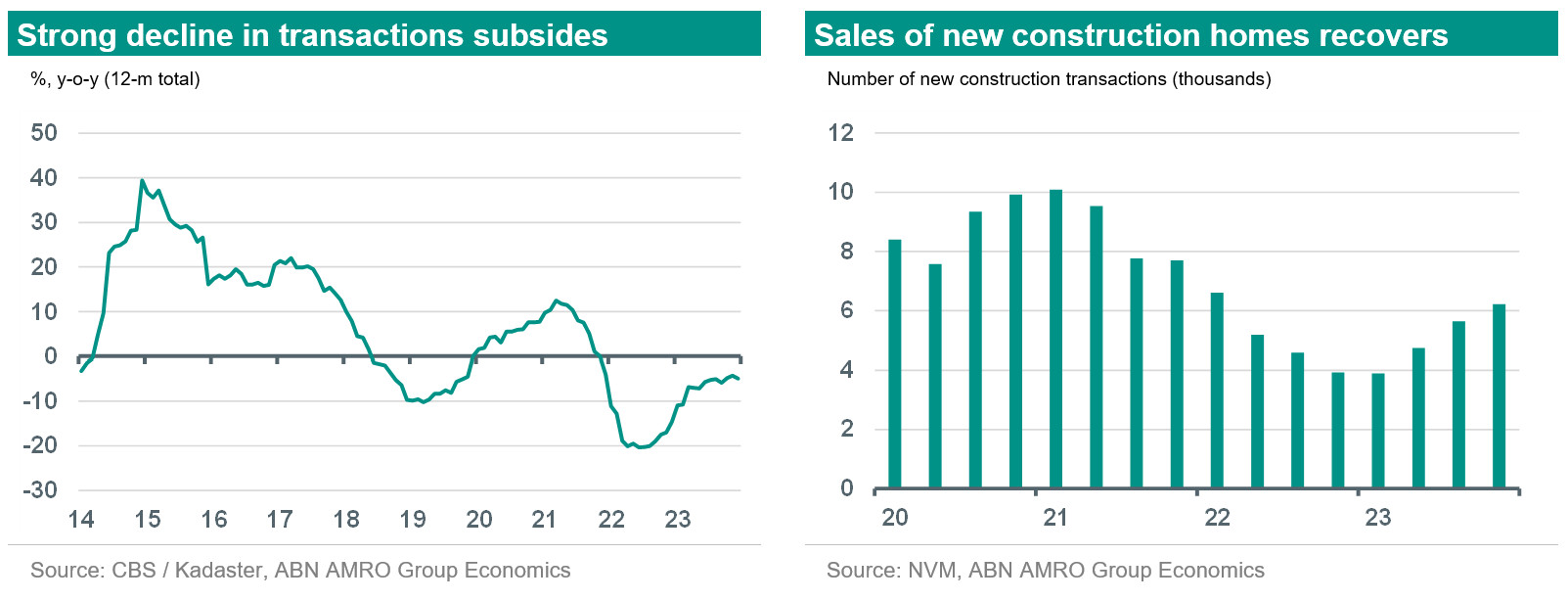

That the stock of homes for sale is shrinking has less to do with the number of transactions of existing homes. Normally, the inventory declines as more transactions take place. Now that does not apply. The number of transactions declined by more than 9,000 annually to 184,000 in 2023. Although the number of transactions of existing homes has been declining for 3 years in a row, the 2023 total number of transactions is at the long-term average from 1995. The decline in the number of transactions was mainly due to deteriorating affordability caused by rapidly rising interest rates and high inflation due to corona and the energy crisis. This depressed sentiment and buyers dropped out. Transactions in newly built homes fell even , as these are more often in the higher price segment and relatively expensive homes became unaffordable for many households due to higher mortgage interest rates. A further factor is the higher construction costs and uncertainty during the bridging period; as construction processes take longer, more financing for bridging is needed.

Partly as a result of deteriorating affordability, new construction projects were delayed. In many new construction projects, the 70% pre-sale limit is not met due to collapsed demand from private individuals and developers have to revise plans. Increased market interest rates are also playing a major role in pre-financing for developers and investors. Added to this is the uncertainty about new statutory rent caps and the impact they will have on revenues. All this led to a sharp drop in the number of new home sales. The total of annual building permits issued has also been declining since early 2022. In October 2023, that number stood at 55,134 which is the same level as the last quarter of 2016. A low number of building permits issued is a harbinger for a lot less new construction in the medium term.

At the same time, in the short term, there are developments that could support housing construction and the number of new construction transactions (and thereafter, existing construction). The new 2024 ensure that more can be borrowed for homes with a good energy label. New construction homes must meet the requirements since January 2021, which means that, in addition to existing homes with a good label, they by definition fall into the group of homes for which more can be borrowed. This will help the sale of new-build homes and thus the flow-through in the housing market. Furthermore, outgoing Minister De Jonge has taken several measures, such as the , to help projects that are already far enough along in terms of planning to start building in 2024/2025, but cannot get out due to the changed economic situation. Lastly, rising house prices may cause project developers' margins to come under less pressure, so that projects can be better off and construction can start earlier.

The first signals of a cautious recovery in the number of new construction transactions are already visible in NVM's figures, which are often a few months ahead of those of CBS / Land Registry. Since the first quarter of 2023, sales of new homes have increased every quarter. In the last quarter of 2023, the number of transactions of 6,111 was more than 25% higher than the last quarter of 2022. This trend may continue in 2024. In 2020, showed that 80% of households who bought a new construction home left an old home behind for new residents. The increase in new construction transactions is helping the flow-through and thus transactions for existing construction.

Affordability stabilizes and homes more accessible due to change in lending standards

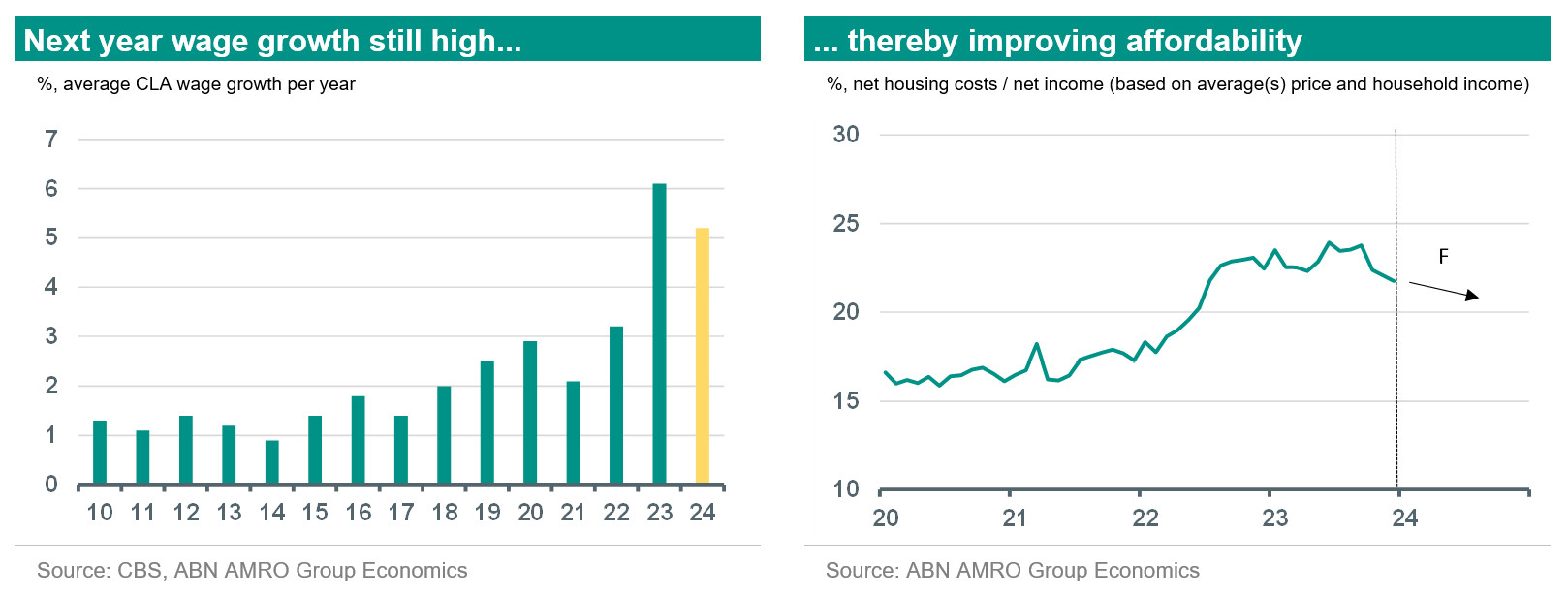

The turnaround in the housing market is closely related to wage trends. Trade unions and employees made good use of high inflation and the associated loss of purchasing power to negotiate for higher wages. In a tight labor market, where only less than 4% of the labor force is unemployed, they succeeded well. CLA wage growth reached 6.9% in the fourth quarter of 2023, the largest increase in over forty years. In 2023, wages rose 6.1%, and our forecast for wage growth in 2024 is more than 5%. A strong increase this year will improve housing affordability.

Furthermore, changes in lending standards will also improve the accessibility of owner-occupied housing. Starting this year, single people with incomes above EUR 31,000 will also be allowed to borrow more. Last year there was a fixed percentage additional borrowing capacity for incomes below EUR 31,000, this year it is a gross mortgage amount of EUR 16,000 for all incomes. Single people are more likely to have lower incomes than two-income earners, making an extra amount a big difference for accessibility. Before 2022, it was that only 1.1% of the entire housing supply was accessible to single starters with a modal income. In addition to singles, former students will benefit from the change in the calculation of student debt. Instead of the original study debt, this year the actual amount of the study debt will be used as a guideline, so former students who have paid off a lot will benefit.

Mortgage rates fall due to the pricing of future central bank interest rate cuts

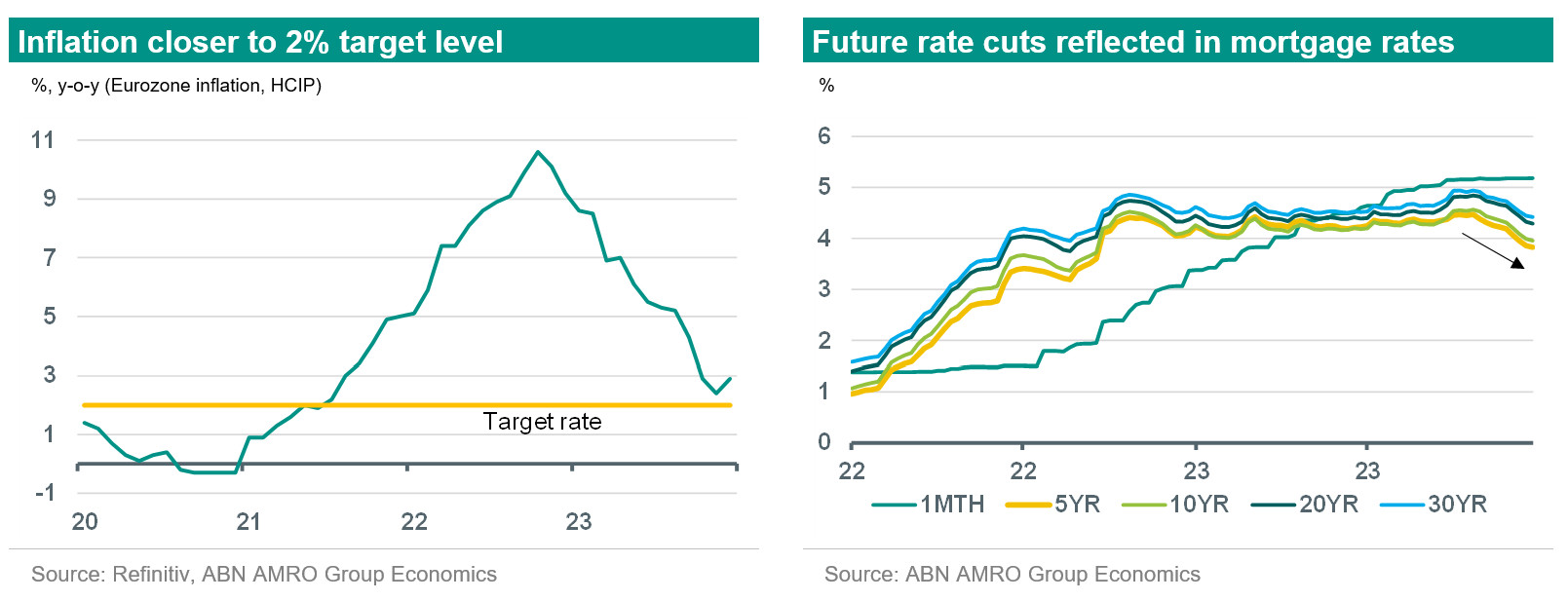

Unlike the housing market, the economy is currently in worse shape. Inflation has fallen sharply over the past year. Due to a sharp drop in energy prices, the general price level in the Netherlands in December 2023 is "only" 1.2% higher than a year earlier. High inflation reduced purchasing power, allowing consumers to spend less and businesses to invest less. As a result, economic growth slowed. Since the first quarter of 2023, the Dutch economy has contracted for three quarters in a row.

The European Central Bank (ECB) raised official interest rates to, for a short time, unprecedented levels. The deposit rate rose from -0.5% in July 2022 to 4% in September 2023. This has put a firm brake on lending and spending. In the Eurozone, inflation stood at 2.9% in December. That is close to the ECB's medium-term target level of 2%. This means that the ECB's task of bringing down inflation is almost complete and the ECB can again move toward interest rate cuts to support the economy. We think the ECB will start doing so from June onwards.

Investor expectations of possible ECB rate cuts are already affecting capital market rates. With an expected cut in deposit rates, long-term interest rates will be the first to go down. The 10-year interest rate on Dutch government bonds, which is strongly correlated with the interest rate on Dutch mortgages with a long fixed-interest period, has started to decline since late October. The 10-year rate has fallen nearly 100 basis points (1%) in two months. We think the 10-year rate will reach 2.40% by the end of this year. The recent drop has also caused mortgage rates to move downward with it since November. Mortgage rates with terms of 5 years or longer are on average 0.5% lower in January than in October last year. This puts long mortgage rates at the same level as mid-2022. The recent decline in interest rates is contributing to the affordability of owner-occupied homes.

Fewer mortgages issued, but last quarter portends recovery

Mortgage production fell as there were fewer home transactions, while the average mortgage amount remained virtually unchanged. Added to this, higher interest rates made refinancing less attractive and fewer loans were taken out for consumer spending. According to , mortgage applications decreased by 29.3% compared to 2022. Within the buyer market, there were about 8% fewer applications, while the non-buyer market saw a decline of more than 50%. The latter is largely explained by the refinancing market, which has virtually dried up since the end of 2022. Higher interest rates also put a clear stamp on the popularity of interest only loans. In fact, the number of applications with an interest only loan portion declined by nearly 72%. While at its peak in 2022 nearly half of all mortgage applications had an installment-free portion, by December 2023 that has dropped to just one in five.

Along with the change in preference for mortgage products, the preference for the term of the fixed-interest period is also changing. In early 2022, 20- and 30-year fixed was still the norm, but that is currently the 10-year rate. Almost 60% of the application volume in December 2023 was fixed for 10 years. In anticipation of future interest rate declines, 5-year rates have also gained popularity this year. In one year, the volume of 5-year interest rates in mortgage applications quadrupled to nearly 10% in December. Many mortgage applicants are thus anticipating a future decline in interest rates. However, interest rate fixes under 5 years are reviewed at the key interest rate of 5% set by Authority for the Financial Markets (AFM). Now that the difference between the 5-year mortgage interest rate and the test interest rate is small, this is often not an objection for some buyers. However, if interest rates continue to fall, buyers will be able to borrow less at the key rate than at the mortgage rate. Then, many buyers may opt for the longer 10-year rate again.

The good last quarter of 2023 may be a harbinger for the upcoming year. In the last three months of last year, growth returned for the first time since early 2022. The number of applications in the last quarter of 2023 was almost higher than in the last quarter of 2022. Whether the increase will continue is not yet certain because the Nibud has slightly the loan standards since the beginning of this year in connection with the higher housing costs due to high inflation in recent years. It may be possible that many applications have been brought forward as many home buyers can borrow less due to the change. Except for homes with a good energy label, for which, on the contrary, a lot can be borrowed. However, the loss in borrowing capacity will be by further wage increases during the year.

Starters continue to buy and get some support this year

Starters currently make up a large part of mortgage production in terms of volume and numbers. Although the total number of mortgage applications and mortgage production fell, the number of first-time buyers applying for mortgages remained more or less the same. As a result, the share of first-time buyers in total applications rose from an average of 27% in 2022 to 35% in 2023. Even with higher interest rates, the demand for housing from first-time buyers proved large enough to ensure a stable volume of applications. In terms of mortgage volume, the share of first-time buyers increased even more. Starting in early 2022, the share of first-time buyers doubled to nearly 45% by the end of December 2023.

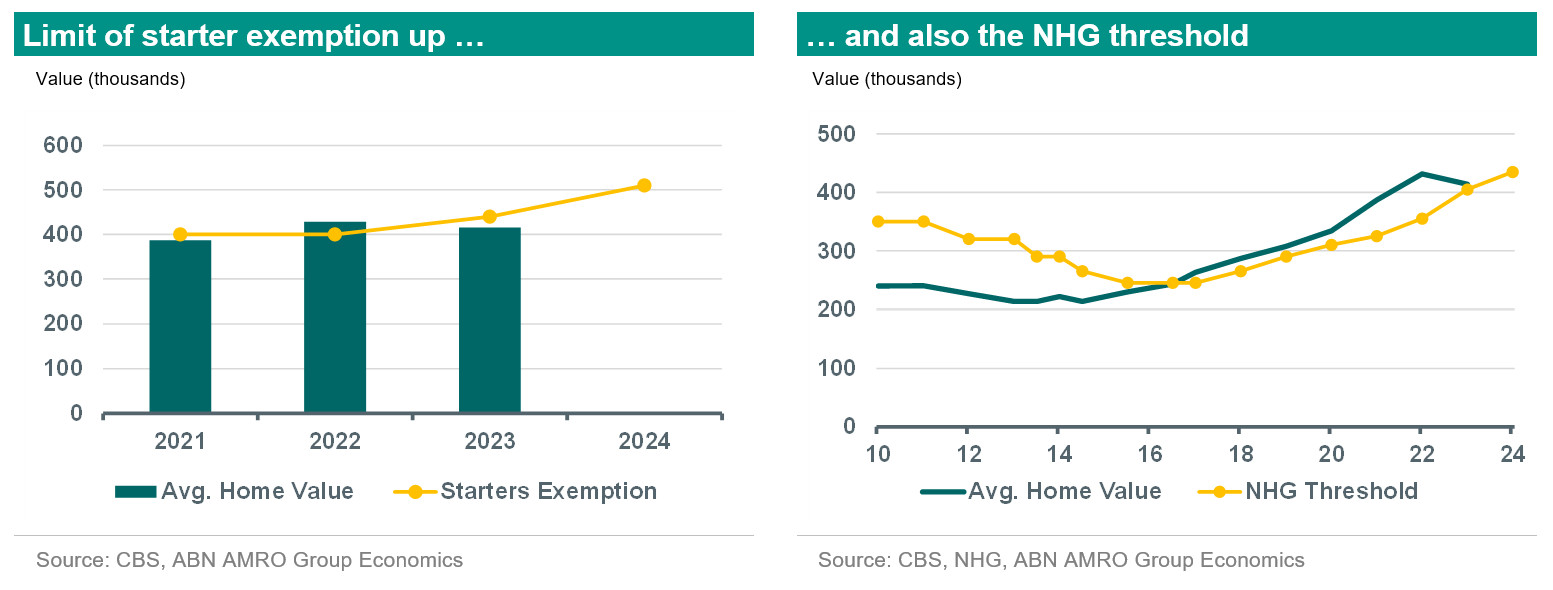

The continued dominance of first-time buyers in applications may continue next year. The amount of the starter exemption, which ensures that young homebuyers (up to 35 years old) do not have to pay transfer tax of 2% when purchasing their first home, is going up again this year. The starter exemption will be increased by EUR 60,000 in 2024, bringing it to EUR 510,000. The new limit is well above the average home value of EUR 434,000 in the last quarter of 2023. This ensures that first-time buyers can take advantage of the tax rule for a large proportion of owner-occupied homes. This increases the likelihood that starters will be able to find a suitable home because they will have to bring in less of their own money. For a EUR 450,000 home last year, a starter had to bring in EUR 9,000 of their own money to pay transfer tax, and none this year.

The NHG limit has also been raised. It was EUR 405,000 in 2023 and has been raised to EUR 435,000 in 2024, just above the price of EUR 434,000 from the last quarter of 2023. The higher limit means that more homes fall within the arrangement. The NHG scheme insures buyers against the risk of residual debt in the event of a forced home sale following job loss, divorce or deceased partner. Buyers also have the advantage of a lower risk premium on NHG-guaranteed mortgages, which means they pay a lower interest rate. By 2023, the NHG limit had been increased by EUR 50,000. This, combined with falling house prices, caused the NHG limit to move closer to the average house value. Partly because of this, the number of applications submitted to NHG increased by 36% percent.

What first-time buyers can no longer take advantage of this year is the gift exemption. The gift tax exemption, formerly known as the “jubelton”, has been completely abolished in 2024 after previously scaling down in 2023. First-time buyers with affluent and wealthy parents were able to take advantage of this tax measure in a market where high price and overbidding was the norm. This will come to an end this year. WoonOnderzoek showed in 2021 that starters is helped by their parents. Starters are more likely to have lower incomes, therefore build up less savings and have been able to build up savings for a shorter period of time due to their young age. For last year, the HDN showed that brought in a relatively large amount of their own money, namely EUR 36,000. Part of this amount could potentially fall away next year due to the abolition of the gift tax exemption, making it more difficult for first-time buyers to buy a home.

Family mortgage offers alternative to jubelton

First-time buyers who would previously take advantage of the gift tax exemption can still take advantage of the family mortgage. In the Netherlands, it is possible to take out a mortgage loan from family or friends. Through this form, there is also a tax advantage to be gained. The interest received by parents can be donated back up to a maximum of EUR 6,633 tax-free. The interest can also be deducted through income tax. This combination makes it fiscally and financially attractive to borrow money from relatives for a house. This type of financing is likely to increase this year with the complete elimination of the jubelton.

Even today, the attractive nature makes this form of financing common. shows that, on average, 1 in 6 households (partially) use a family mortgage. In 2020, the volume of outstanding family mortgages increased by EUR 1.2 billion to a total value of about EUR 70 billion. This amounts to about 10% of total mortgage debt. The increase in family mortgages in 2020 is also significantly larger than that of jubelton (EUR 700 million). To prevent abuse of the product, the interest rate paid should not deviate too much from the market conforming rate. An interest rate that is too low can be seen by the tax authorities as a gift, which means that gift tax must still be paid. On average, family mortgages do have an interest rate of 3% that is slightly lower than bank mortgages (3.3%), but whether this is due to their tax strategic use is difficult to say.