Global Daily – US labour market still has a way to go

US Macro: Payrolls jump will mask significant underlying slack. The March non-farm payrolls report will be published tomorrow. We expect a 700k jump in employment numbers, a touch higher than consensus forecasts for a 650k rise, and almost double what we saw in February (379k).

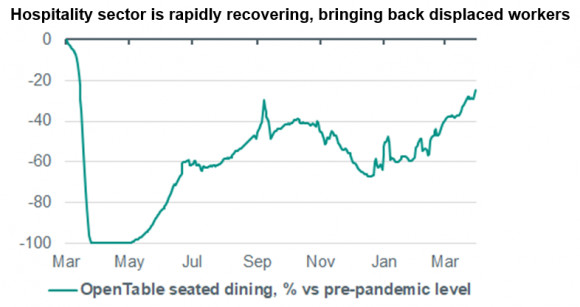

This is coming on the back of a further easing of pandemic-related restrictions in the US, which is driving a strong recovery in the hospitality sector, thereby bringing back displaced workers to the sector. Restaurant dining is now running at around 25% below pre-pandemic levels, according to OpenTable reservation data; this compares with a 60% shortfall at the beginning of the year. The jump in jobs would take the unemployment rate down to 6.0% down from 6.2%, which assumes only a modest pickup in labour force participation. Indeed, while unemployment at this rate will still be well above levels consistent with full employment, the depressed level of labour force participation means that even this overstates the true health of the labour market – were participation back at pre-pandemic levels, the unemployment rate would be closer to 8%.

Source: Bloomberg, ABN AMRO Group Economics

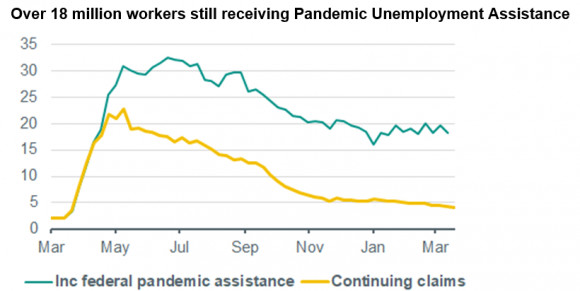

The significant remaining slack in the labour market is corroborated by the weekly jobless claims data. The headline level of continuing jobless claims has steadily fallen over the past year, from a peak of around 23 million back in May to 3.8m as of today’s latest figures (the week to 20 March). However, those claiming federal Pandemic Unemployment Assistance (PUA) are still extremely elevated, at 18.2 million. The claimants of this benefit include freelancers and the self-employed, as well as other unemployed people who are ineligible for regular unemployment benefits. This too suggests considerable underlying slack remaining in the US labour market.

Source: Datastream, ABN AMRO Group EconomicsBoth the economy and the labour market are recovering at a faster than expected pace, helped by the significant fiscal support that continues to make its way through the economy. We expect this to continue. However, even with the very strong growth momentum in the economy, we expect some degree of labour market slack to persist until early 2023. As such, we are a long way from the labour market even beginning to exert an inflationary impulse to the economy. This will keep the Fed comfortable with rates at near zero for some time to come, and as such, market pricing for rate hikes to start in late 2022 continues to look overly aggressive to us. (Bill Diviney)