Germany - Traffic light coalition turns red

German snap elections an opportunity for step-change in fiscal policy, but political divisions will be hard to overcome

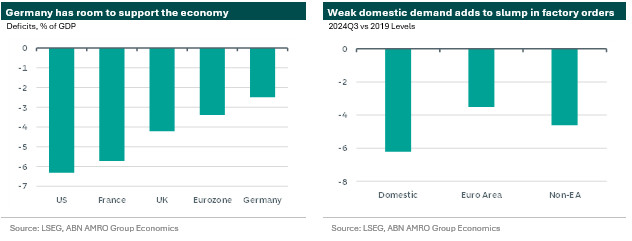

The Scholz government is on its last legs. Following the dramatic firing of the finance minister last night, the coalition government is on the cusp of a no confidence vote which looks set to lead to a snap federal election in early 2025. The key bone of contention in the coalition was the approach to budgetary discipline amid what has become a slow-burning crisis in German industry, with the SPD in favour of a suspension of fiscal rules to deal with the crisis, with coalition partner FDP firmly opposed. Following the firing of the finance minister, Chancellor Scholz remarked: “The situation is serious. There’s a war in Europe, increasing tensions in the Middle East, the economy is stagnating. Companies need support now.” Germany has the lowest budget deficit in the G7, and at 2.5% it is within the EU’s 3% deficit rule. At the same time, growth is significantly underperforming the rest of the eurozone, with the economy continuing to stagnate on the back of structural competitiveness challenges and weak domestic demand. As such, Germany arguably has both the space and the need for a fiscal response.

However, opinion polls suggest that it would be challenging to form a new coalition government. The centre-right CDU/CSU is leading at 32%, with the SPD neck-and-neck in second place with the far-right AfD at 16% and 18% respectively. The FDP looks set to be the biggest loser and may not even make the 5% threshold to get into the Bundestag. Still, it is early days and the election – while in the near-term creating uncertainty over the outlook – at least offers an opportunity for a step-change in policy at a time when the existing government is essentially paralysed.

Growth outlook remains weak overall – Following the election of president Trump, the outlook for the German economy – which was already weak – darkened further. A possible red wave, with Republican control of Congress, significantly raises the chances of Trump going all-in on tariffs. While uncertainty is high, we expect some implementation of tariffs to hit German exports to the US hard. This is likely to keep a lid on the gradual recovery we had forecast for next year (2025: 0.8%), and keep growth well below trend. As such, even if the election ultimately does herald a step change in fiscal policy and public investment, this would pose upside risks within an overall weak growth outlook, however any change that might materialise would likely not come until later next year or well into 2026.