Gas Market Monitor - Market remains watchful for supply uncertainty

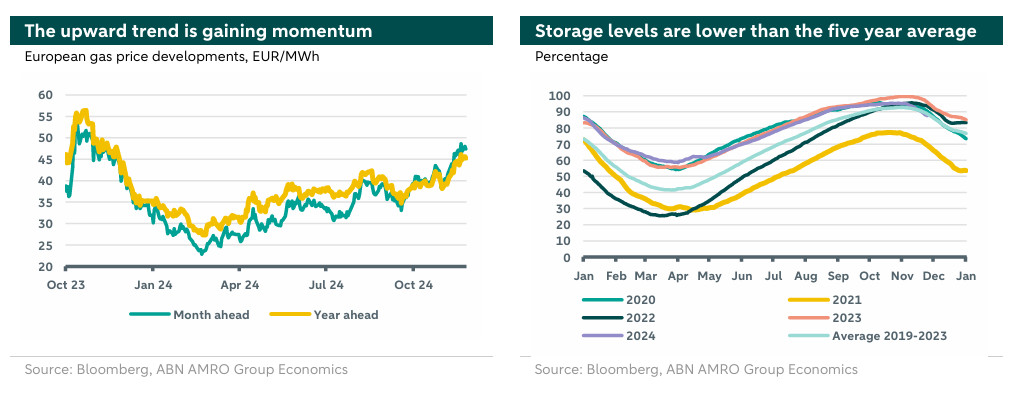

European TTF prices have been heading upwards due to adverse weather conditions, supply disruptions from Russia, unclarity about the future of transit agreement through Ukraine, and escalations in the Ukrainian war. Storage withdrawal rate has been higher than average, inducing high uncertainty and strong volatility.

Heating purposes are the leading demand driver for the fuel as demand from industrial recovery shifts towards 2025

The bullish sentiment is dominating the market with a focus on potential early halt of Russian flows before the end of the year

Markets remain vigilant to emerging disruptions through unplanned outages/maintenance in the key suppliers such as Norway and the US

We expect prices to remain elevated during the remainder of 2024 driving our outlook for TTF year-ahead price to average around 44 €/MWh in Q4 of 2024

In 2025, we expect prices to cool down in the first half and gradually firm towards the end of the year

European gas prices have been trending upwards since late September after a temporary reverse towards mid-September. The TTF has averaged 40.9 €/MWh for the benchmark year-ahead contract since the start of Q4 (42.1 €/MWh for the month-ahead contract). The increase in prices was fueled by a combination of factors: a cold spell hitting Europe which coincided with slower wind and lower renewable generation, the sudden halt of Russian supplies to Austria, the upcoming end of Ukrainian gas transit agreement with Russia, and geopolitical tensions especially the escalations in the Ukrainian war and in the Middle East. As a result, the rate of storage withdrawals has been high raising uncertainty about the timely refill before upcoming winter and increasing market volatility. European industrial demand continues to be weak, while LNG markets remain tight, and volatility is here to stay. European TTF year ahead contract was trading around 44.3V€/MWh at the time of writing.

European gas market developments

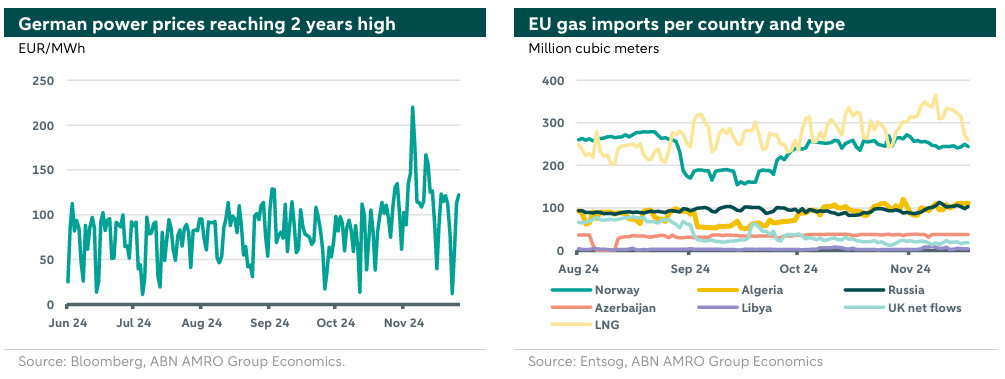

Markets have also been responsive to weather conditions. A recent cold spell hitting the North western countries, which induced higher demand for heating was combined with slower wind speed and lower renewable power generation. This has raised the storage withdrawal rate where storage levels, for the first time in three years, fell below the five year average at this time of the year (87.7% vs. 88.7% average). German electricity prices reached a two year high following high gas power generation to compensate for low renewable output (see left hand chart below). The high storage withdrawal rate means that Europe could end the winter at low storage levels which increase uncertainty about a timely refill before the following winter and push summer prices up, along with making the market more sensitive to supply disruptions and geopolitical risks.

On that note, other factors have also invoked uncertainty in the market inducing volatility in TTF prices. For a start, the sudden halt of the flow of Russian gas to Austria which translates into early withdrawals from storage and increasing competition on LNG. Furthermore, TTF prices have been sensitive to any news regarding the extension of the transit agreement of Russian gas through Ukraine, which expires by the end of 2024. The most probable solution is to substitute the Russian gas by that coming from Azerbaijan through Ukraine. However, markets remain cautious as no agreement has been reached yet. If no agreement is reached, the Russian pipeline supply would need to be compensated by higher supply from other sources such as Norwegian pipeline gas or higher LNG imports from the USA. On that note, the win of President Trump a second term increased prospects of higher future US LNG following his vows to lift the pause on new permits for exporting of US LNG.

The geopolitical premium on TTF price is back following the latest escalation in the Ukrainian war, the risk of wider conflict, and a potential lower US support under the new administration. At the same time, LNG markets remain vigilant to the situation in the Middle East following the recent truce in Lebanon. Even though most of European LNG imports comes from the USA, supply disruptions in the Middle-East would increase international competition for the fuel and put upward pressure on European prices.

Imports from Norway, the main pipeline supplier, are stable for now. Similarly for imports coming from Algeria, as can be seen in the chart above (right). In addition, flows from Russia to central Europe, other than Austria, via Ukrainian territory remain at normal levels for now, however market participants are watchful for any changes to the status quo. LNG imports are witnessing a decrease after gaining momentum in November driven by stronger competition for the fuel from Asia coinciding with a shut down in . LNG would be the main source of volatility in the coming months as long as no new disruptions in pipeline supplies would emerge.

As supply worries increase, there is a rise in bullish sentiments across investment funds reflected by the increase in their net long positions (rose 2.6% last week to its highest level since 2021). The main concern fuelling the worries is the early disruption of Russian supply before the end date of the transit agreement between Russia and Ukraine (end December 2024), which means that prices should remain high to attract more LNG cargos. All in all, market remains tight and responsive to any disruptions via supplies or weather conditions.

From the demand side, the recovery in European industrial demand still lacks a momentum. The eurozone composite PMI for November slipped into contractionary territory at 48.1 (50 in October), indicating a decrease in business activity in the eurozone halfway through Q4. Manufacturing PMI for Eurozone increased slightly towards 43.2 (was 43 in October) while that of Germany witnessed a decrease towards 45.2 (was 46), reflecting the challenges facing the biggest European economy. At the same time, the expected tariffs under the new US administration will have an adverse impact on growth and a divergence in monetary policy rates across the Atlantic in 2025 (see our global outlook for 2025 here), which would slow down the recovery in industrial demand in the second half of 2025. In addition, demand for heating purposes is expected to be higher this winter where weather forecasters predict this winter to be colder than the 10 year average. Accordingly, demand for heating purposes will be the leading driver for the fuel in the coming months.

Outlook

Looking forward, as we move through winter months, the EU gas market remains tight and responsive to supply disruptions and weather conditions, such as cold spells or lower renewable output. Most importantly, an early halt of Russian gas through Ukraine would put upward pressure on prices. Furthermore, demand for heating purposes will be the leading component for the fuel in the coming months as demand for industrial purposes shifts towards 2025. Accordingly, we expect prices to remain elevated in the remaining of 2024 driving our outlook for TTF year-ahead price to average around 44 €/MWh in Q4 of 2024. In 2025, we expect prices to cool down at the beginning of the year as the uncertainty of the Ukrainian transit agreement clears out. In any case, we expect the EU to become more dependent on LNG, while prices become more responsive to the expected depreciation in exchange rate in 2025 given the anticipated policies of the new US administration. Thus, we expect prices to gradually firm towards the end of 2025 as we enter the heating season. Our outlook for EU TTF year-ahead benchmark is summarized in the table below.