FOMC Preview - Hedging against Trump

We expect the Fed to stay on hold this Wednesday, and to push back against more aggressive easing priced by markets. Recent inflation data, upside inflation risks, and the risk of de-anchoring expectations limit the scope for easing. Holding rates steady now decreases the probability of having to raise rates in the near term, avoiding the ire of the Trump administration.

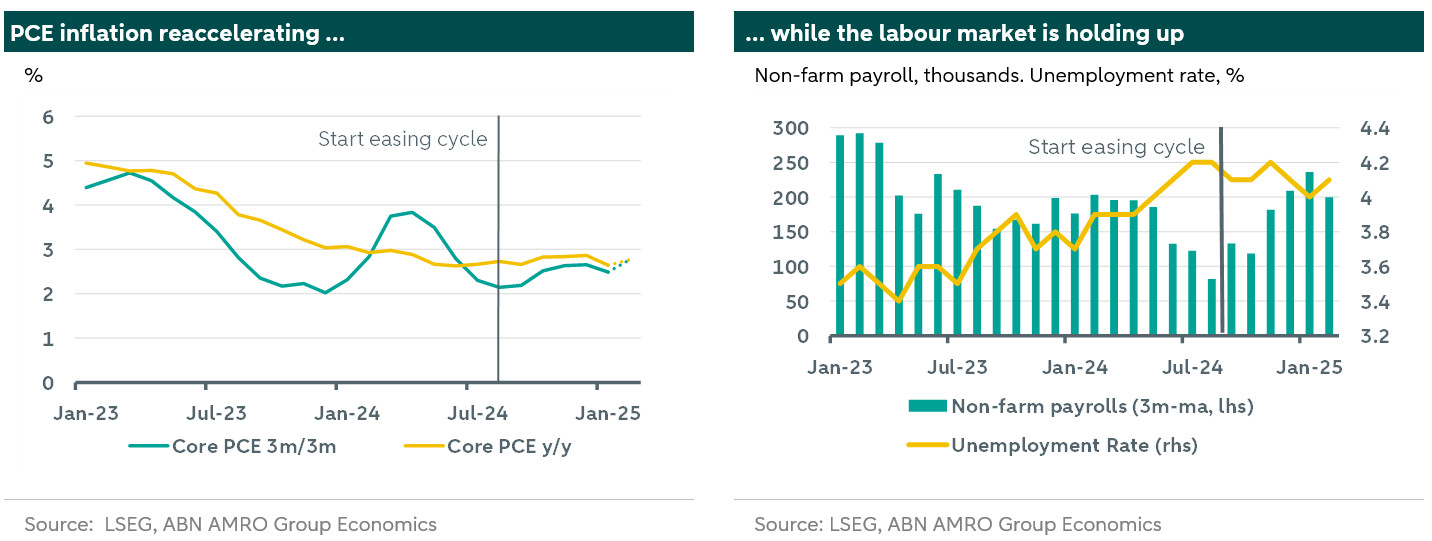

We expect the Fed to once again hold rates steady in the March FOMC meeting, after pausing the easing cycle in the previous meeting. The Fed has made it clear that patience in further easing comes at little cost amidst uncertainty about the actual level of restrictiveness. The labour market is holding up for now, despite efforts by the government to decrease its own workforce. Inflation is seemingly re-accelerating, with our nowcast for the upcoming core PCE reading at 0.35% m/m. This increases the annualized 3m/3m rate to almost the y/y rate, a sign of stalling momentum. A strict interpretation of the Fed’s dual mandate, price stability and full employment, makes it clear that the Fed has no reason to ease further at this juncture.

Casting the net slightly wider, and factoring in growth and the stock market, which feed into employment, the picture is slightly different. This ‘Fed put’ has been reason for market pricing of rate cuts to increase. The change in sentiment followed a shift in the Atlanta Fed Q1 GDP nowcast from +2.3 to -2.8 in the span of less than a week. While predominantly related to strong imports, the nowcast led to rising recession fears. The question is whether the Fed would exercise this put. While a slowdown in consumption and investment is also likely, final private demand is likely to remain positive. Similarly, the US stock markets saw a reasonably strong correction, but still stands at a relatively high valuation level.

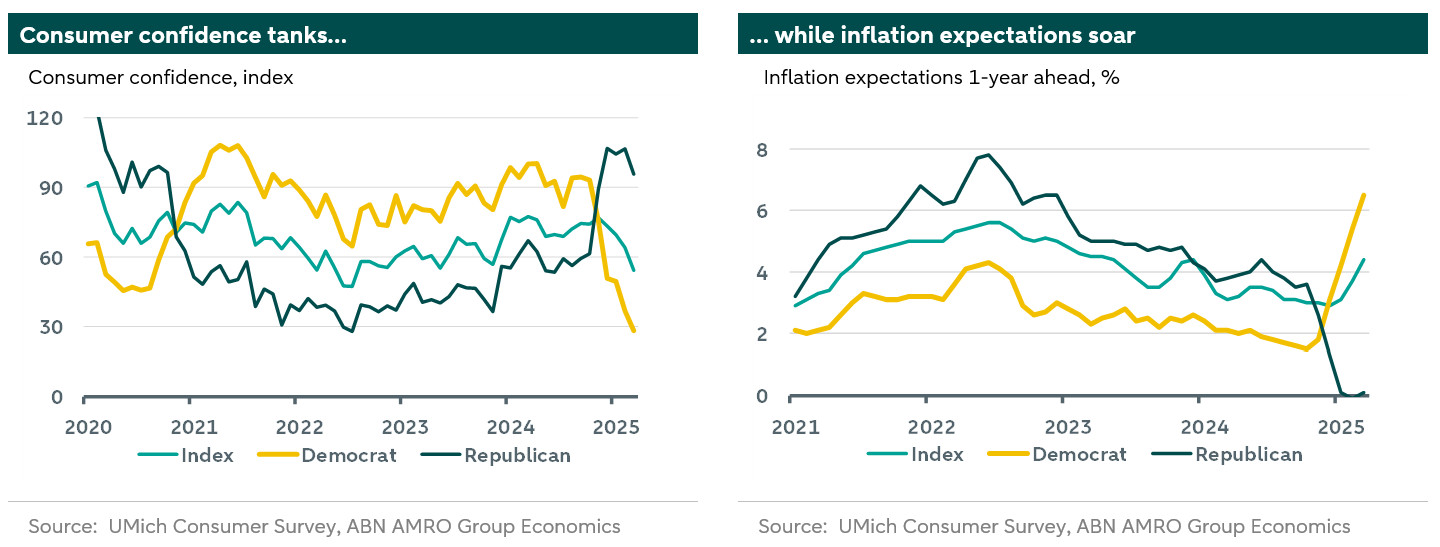

Looming risks to both sides of the dual mandate pull in either direction. Tariffs represent the worst kind of shock for the Fed, driving inflation up and activity down. They therefore also increase downside risks to the labour market, with further shocks coming from already noticeable decreases in the government workforce. Downside risks to the employment mandate will be partially alleviated through lower growth in labour supply on the back of a reduction in net migration. This deteriorating outlook is captured by the University of Michigan Consumer Confidence index, which fell abruptly with a magnitude similar to the Covid shock. Beyond the usual flip in confidence between Democrats and Republicans when an administration changes, confidence among Republicans is also now decreasing (see chart above-left). This is largely on the back of tariff threats, as also captured by their inflation expectations index. The risk of de-anchoring inflation expectations is substantial, with one-year ahead inflation expectations rising by over a percent since Trump’s election, and even the 5-year expectation, which stayed stable during the high-inflation period, rising by half a percentage point. This risk is sufficient for the Fed to focus on its price stability mandate, even in the face of weaker growth.

The natural response, then, is to keep rates in slightly restrictive territory, leaving it better positioned to deal with future shocks – whose direction is known, but magnitude is unknown. This way, in the best case scenario the Fed may even avoid having to raise interest rates. At the very least, it avoids the more messy scenario of lowering interest rates further now, only to raise them again a meeting later, and may more generally delay the time until hiking may or may not be necessary. This makes a direct confrontation with the Trump administration less likely (though pressure may still come from the administration to lower rates in any case, as it did in Trump 1.0).

Consistent with a move towards this approach, the dot plot will likely already show less easing by the end of 2025 than in the previous meeting; we expect the median FOMC member will put in one or two 25bps cuts. Growth and inflation projections are likely to reflect the tariff shocks of higher inflation and lower growth. Our base case sees rates staying at their current restrictive level through to end-2026, but the ultimate magnitude of tariffs and other policies may steer the path off course.