Falling US inflation paves way for 25bp Fed hike

December inflation was in line with expectations, with the headline CPI falling -0.1% m/m, and the core CPI rising 0.3% m/m. This took annual headline and core inflation down to 6.5% and 5.7% y/y respectively - the lowest readings in over a year.

US inflation continues downtrend

The fall was driven largely by further pass-through from lower oil prices to petrol prices, but continued falls in used car prices, and weak medical services inflation, were also a drag. Shelter inflation, and other components of services inflation in contrast remained elevated, as expected.

Inflation to continue to move lower...

All in all, inflation continues to trend lower in line with our base case, and this should give the Fed the confidence to to a 25bp hike when the FOMC next meets in early February. In the near term, we expect a renewed drag on headline inflation from falling utility gas prices – reflecting the mild winter and falling wholesale gas prices. Food inflation also looks to have peaked, and we are likely to see a further deceleration over the coming months.

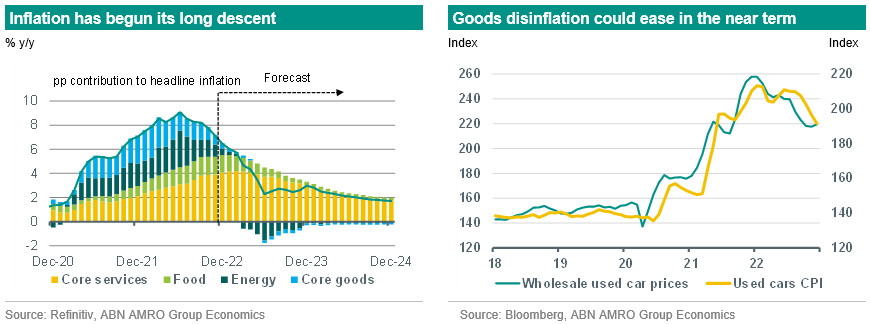

...but goods disinflation may ease

For core inflation, while annual inflation should continue to decline, we may see some near term pickup in m/m price growth, as a significant drag in recent months has come from falling wholesale prices for used cars, which for now looks to have stabilised (see figure above). Services inflation is also likely to remain elevated, as the turn in housing rents for new leases will take time to feed through to shelter inflation, while the tight labour market is keeping cost-push pressures in services a little on the high side. However, as the year progresses, we expect services inflation to ease back, and this should ultimately bring inflation within touching distance of the Fed’s 2% target.