Eurozone services inflation edges lower; NL still volatile

Eurozone flash HICP inflation edged lower in February, albeit the decline was a bit less than our and consensus expectations, with headline inflation falling to 2.4% from 2.6% (ABN/consensus: 2.3%). Core inflation moved down to 2.6% from 2.7%. The slight upside surprise (which is smaller unrounded) was driven by somewhat higher food inflation, which edged up to 2.6% from 2.3%, while goods inflation also came in a touch higher at a still subdued 0.6%, up from 0.5%.

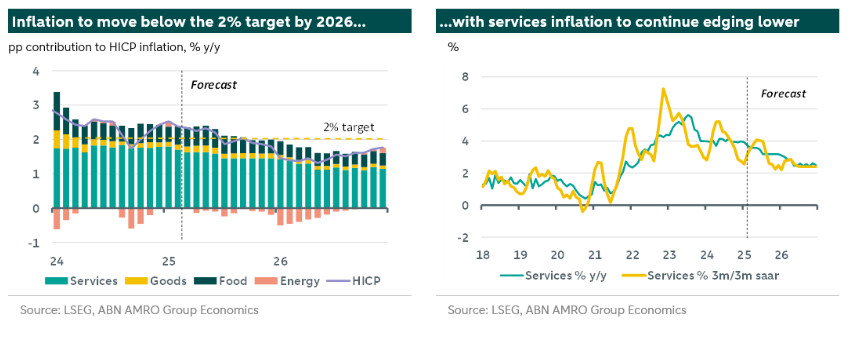

Most importantly for the outlook and for the ECB, services inflation moved lower in line with our expectations, to 3.7% y/y from 3.9% in January, which is the lowest reading since the energy crisis, if you exclude last April which was distorted by the timing of Easter. According to the ECB’s seasonally adjusted data, the m/m rise was much smaller than we have seen in recent years for February, at 0.3% (in 2023 and 2024 the m/m rise was 0.5%).

Despite the ECB’s seasonal adjustment, this data still has some residual seasonality, and is typically higher in the early months of the year when a lot of indexation for services (eg. insurance) takes place. The fact that monthly services inflation has come in significantly lower than recent years is therefore a promising sign of a substantial shift in inflation dynamics for the sector. Even though wage growth remains somewhat on the high side (albeit on a cooling trend), it seems that businesses are absorbing more of the rise in wages in their margins rather than passing it on to consumers.

Looking ahead, we expect services inflation to continue to edge gradually lower, albeit staying well above its pre-pandemic level at least for this year. This decline in services inflation is expected to drive headline inflation back down to the ECB’s 2% target on a sustained basis by the middle of 2025. Thereafter, we expect the growth hit from US trade tariffs to push inflation below target towards the end of the year, paving the way for the Governing Council to eventually lower the deposit rate to 1%. For more on our ECB outlook, including for this Thursday’s meeting, please see here. (Bill Diviney)

The Netherlands: Inflation remains volatile

Dutch CPI picked up again in February, with the flash estimate coming in at 3.8% y/y compared to the lower January figure of 3.3%, and above our expectations of a decline to 3.2%. Compared to our estimate, the largest contribution came from industrial goods prices which rose to 1.5% y/y, compared to 0.3% in January.

Food inflation also picked up again, to 7.5% y/y compared to 7.0% in January. We had already anticipated it to stay around the 7% y/y, in which a large role can be attributed to product-specific tax rates such as the tobacco tax implemented in April 2024. As expected, energy prices benefit from favourable base effects as the energy index was significantly higher in February 2024. Still, on a m/m basis energy prices increased by 0.5%.

Finally, services inflation picked up a bit compared to last month, increasing to 4.6% y/y from 4.4%. Last month the breather in the CPI was mostly driven by declining services inflation (due to a lower annual indexation). In the coming months, we expect Dutch inflation to decrease, to 2.8% in 2025 and 2.5% in 2026. This is above our estimates for the broader eurozone and also exceeds the ECB’s 2% target. (Aggie van Huisseling)