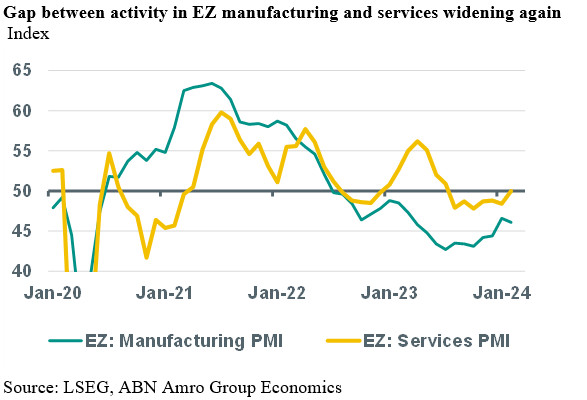

Eurozone PMIs signal ongoing contraction in industry, but stabilising services activity

The eurozone composite PMI increased to 48.9 in February, up from 47.9 in January. The rise in the composite PMI was entirely due to an increase in the services PMI to a level consistent with stag, with the manufacturing PMI declining further below the level that separates growth from contraction in activity.

The eurozone composite PMI for February came in somewhat higher than the consensus forecast, but close to our own expectation (at 48.9, up from 47.9 in January). The rise in the composite PMI was entirely due to an increase in the services PMI (to 50.0, up from 48.4), with the manufacturing PMI declining (to 46.1, from 46.6). The details of the report show that the decline in the manufacturing PMI partly was due to shortening of suppliers’ delivery times after the Red Sea related disruptions in January. However, a further decline in export orders for manufacturing and a sharper contraction in manufacturing employment had a downward impact on the manufacturing PMI as well. This suggests that the eurozone manufacturing sector still was in deep contraction territory in the first quarter of 2024. Moreover, the sub-index of the PMI that gauges output prices in the sector declined in February, moving further below the level that separates rises from falls in prices.

Turning to the services sector, the picture was opposite to the one for manufacturing, with activity, employment and output prices all increasing in February, compared to January. Indeed, we think that a rise in real wages as well as the easing of financial conditions in anticipation of the first rate cuts by the main central banks has had a positive impact on activity in certain parts of the services sector. The same factors probably also played a role in the rise in consumer confidence in February (to -15.5, up from -16.1 in January) that was reported earlier this week. That said, the part of services that is related to manufacturing (e.g. transportation, storage and logistics) probably is still contracting. Also, despite its rise in February, the level of consumer confidence still is well below its long-term average value, implying that there will not be a strong rebound in (services) consumption. All in all, we think that the results from the PMI report are in line with our base scenario for the eurozone economy, of GDP roughly stagnating in 24Q1, which would be the sixth quarter of economic stagnation in a row and should reduce underlying inflationary pressures going forward.