Eurozone - Entering a moderate recession

Incoming economic data for October-November suggests GDP contracted in Q4. Core inflation is on a clear downward trajectory, which should continue in the coming months. The ECB is expected to start cutting rates in June, with ECB officials trying to bring down market expectations of an earlier cut.

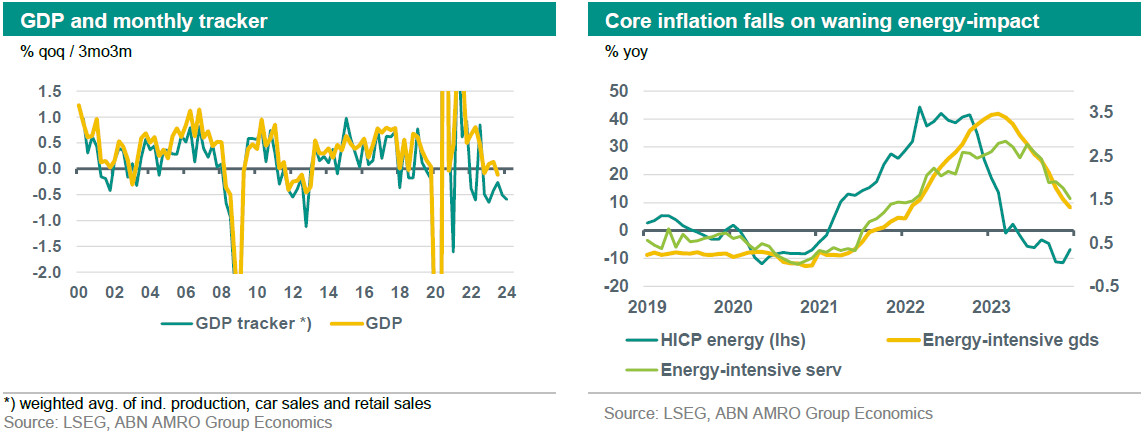

Economic data for October-November suggests that GDP contracted in Q4 (number will be published on 30 January). We have pencilled in -0.2% qoq, but our monthly GDP tracker (graph below) indicates that the risks to this forecast are tilted to the downside. Indeed, the volume of retail sales fell by 0.3% 3mo3m in November and industrial production by 1.6%. Services output is not covered by our tracker, but the level of the services PMI (48.8 in December) suggests the sector is shrinking moderately. As GDP shrank in Q3, another contraction in Q4 would put the EZ in technical recession. We expect GDP to roughly stabilise in 2024Q1 and to grow well below the trend rate during the rest of 2024. Growth will continue to be dampened by the high level of interest rates. Moreover, fiscal policy will be restrictive, as governments’ energy-support measures for households and companies will be unwound. That said, the upcoming start of interest rate cuts by the main central banks has resulted in some easing of financial conditions and has also lifted sentiment amongst consumers and producers, which should support domestic demand moving into 2024. No sharp rebound is expected, however.

Disinflation is ongoing. Headline inflation reached 2.4% in November, the lowest point since July 2021. It rebounded somewhat to 2.9% in December, but this was totally due to base in effects in energy price inflation. All other main components of HICP inflation (food, industrial goods and services) have remained on a downward trajectory. Core inflation has fallen from a peak of 5.7% in March 2023, to 3.4% in December, with a major driver being the waning impact of the jump in in energy prices on the inflation rate of energy-intensive goods and services (see graph below), which has further to go. Also, downward base effects should dampen food price inflation in the coming months. More fundamentally, underlying inflationary pressures are also easing. Weak consumption growth is limiting the room for companies to raise prices and labour market conditions are deteriorating, which will limit wage growth (more on this in the first chapter of this report). All in all, we expect headline and core inflation to continue to decline, reaching the ECB’s 2% target around the middle of 2024.

We expect the ECB to start cutting interest rates in June of this year. Recent comments by a string of ECB officials have also pointed in this direction. The comments have been clearly designed – as well as co-ordinated - to bring down market expectations of early cuts in policy rates. Markets continued to price in a significant probability of a rate cut in April. At the time of writing, around 20bp was priced, though that is down from 40bp at the start of this year. Given this, we think that some further correction is likely as the bar in terms of data (much weaker activity and inflation) to trigger an April rate cut is high. Looking further out, we think that once the rate cut cycle starts, it is likely to be more extensive than markets currently price, with the deposit rate eventually being reduced to 1.5% in the course of 2025.