Eurozone economy stagnating, more weakness to come

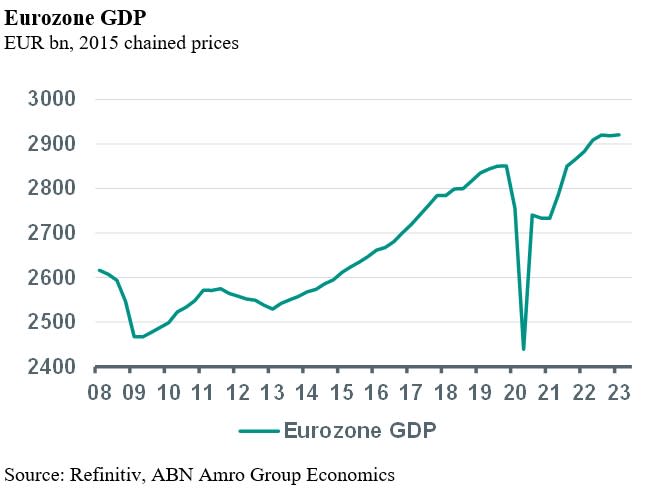

Eurozone GDP expanded by 0.1% qoq in 2023Q1, up from -0.1% qoq in 2022Q4. The result for Q1 was between the consensus forecast of 0.2% qoq and our own estimate of 0.0%. Details for eurozone GDP have not yet been published, but some of the individual countries have published more detailed reports. Overall, the picture is very mixed. Looking beyond Q1 we still expect GDP to contract modestly during the rest of the this year as domestic demand will increasingly be hit by past and upcoming interest rate hikes by the ECB, while a slowdown in global growth (also due to a slowdown in the US) will weigh on eurozone exports.

Eurozone GDP expanded by 0.1% qoq in 2023Q1, up from -0.1% qoq in 2022Q4. The result for Q1 was between the consensus forecast of 0.2% qoq and our own estimate of 0.0%. Details for eurozone GDP have not yet been published, but some of the individual countries have published more detailed reports. Overall, the picture is very mixed. To begin with, the quarterly growth numbers of the individual member states that have been published so far range from -2.7% qoq for Ireland to +1.6% for Portugal. Big countries France (+0.2%) and Germany (0.0%) are more in the middle, while Spain (0.5%) and Italy (0.5%) scored above-average, which could result from the fact that they each receive considerable amounts from the European Recovery and Resilience Facility (RRF) this year.

Zooming in on the contributions to growth in Q1, it seems that as in 2022Q4, final domestic demand contracted on balance, whereas net exports contributed positively to growth. Indeed, monthly activity data has indicated that private consumption contracted, while fixed investment in machinery and equipment probably expanded. In contrast, the sharp contraction in Ireland’s GDP suggests that investment in intellectual property (a major driver of Ireland’s economy) fell in Q1. Meanwhile, some temporary factors seem to have lifted growth in Q1, such as the post-pandemic reopening of China’s economy, which stimulated global trade, and the mild winter weather in the eurozone, which stimulated construction output.

Looking beyond Q1 we still expect GDP to contract modestly during the rest of the this year as domestic demand will increasingly be hit by past and upcoming interest rate hikes by the ECB, while a slowdown in global growth (also due to a slowdown in the US) will weigh on eurozone exports.