Eurozone - Economy continues to flatline

GDP was flat in 2023Q4, whereas a moderate contraction was expected. The roughly 1.5 years of economic stagnation is leaving its mark on the labour market. The ECB is expected to start cutting rates in June.

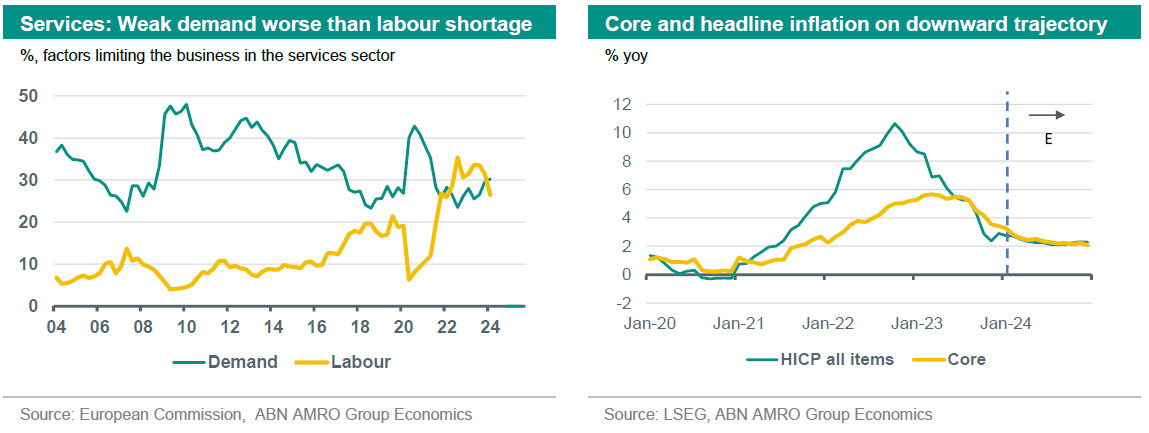

Eurozone GDP stagnated in 23Q4, which was slightly better than the consensus and our own expectation of a moderate contraction. That said, growth has been close to zero now during five consecutive quarters, and the expectation is for another stagnation in 24Q1. Subsequently, GDP should expand moderately during the rest of the year. Growth will be supported by rising real wages and easing financial conditions in anticipation of the first rate cuts by the main central banks. However, fiscal policy tightening and the still high level of interest rates will prevent a sharp rebound. The ongoing weakness in production and demand has already left its mark on the labour market, and we expect conditions to remain weak in the coming quarters. Indeed, the number of job vacancies declined significantly in the second half of 2023, and surveys gauging demand for labour have indicated sharp contraction in employment in industry. Also, when asked by the EC what factors were limiting the level of activity in the services sector, more participants to the survey mentioned lack of demand than lack of employees in 23Q4 (see graph below). The deterioration of labour market conditions that has resulted from the ongoing economic stagnation is expected to have a downward impact on wage growth this year (also see this month’s Global View).

Disinflation has continued moving into 2024. Headline inflation declined to 2.8% in January, down from 2.9% in December and core inflation decreased to 3.3% from 3.4%. A major driver behind the decline in core inflation since its peak of 5.7% in March 2023, has been the waning impact of higher energy prices on the inflation rate of energy-intensive goods and services, which is well advanced but has somewhat further to go. Also, the weakness in the global industrial sector and the sharp contraction in eurozone industrial production during the past year, should further dampen non-energy industrial goods price inflation. Services inflation has been more sticky than goods inflation in recent months, but should decline during the rest of the year. Weak (services) consumption growth is limiting the room for companies to raise prices and labour market conditions are deteriorating, which will limit wage growth. All in all, we expect headline and core inflation to continue to decline in the coming months, approaching the ECB’s 2% target around the middle of 2024.

We expect the ECB to start cutting interest rates in June of this year. The view that the central bank is moving towards rate cuts, but not imminently, was also signalled by the policy statement and the account of the January meeting, which stated “the current levels of the policy interest rates would make a substantial contribution to reaching the 2% inflation target if maintained for a sufficiently long duration” and that “further progress needed to be made in the disinflationary process before the Governing Council could be sufficiently confident that inflation was set to hit the ECB’s target in a timely manner and in a sustainable way.” We think the deposit rate will eventually be reduced to 1.5% in the course of 2025.