Eurozone economic data weak moving into Q3

Economic data for August have generally been consistent with our scenario of the eurozone economy stagnating or contracting moderately during the second half of this year.

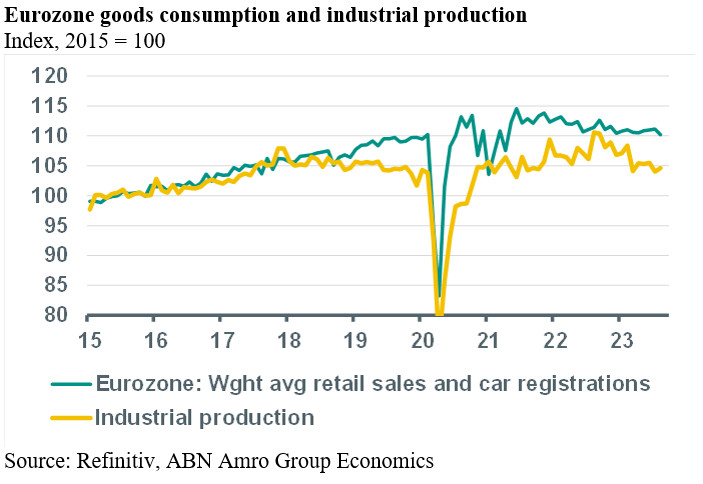

Goods consumption and industrial production contracting

Economic data for August have generally been consistent with our scenario of the eurozone economy stagnating or contracting moderately during the second half of this year. Although industrial production came in stronger than expected in August (+0.6% mom), the July outcome was revised lower (to -1.3% mom, down from 1.1%). Also the less volatile 3Mo3M growth rate remained in negative territory (-0.2% in August). If we assume stable or moderately higher production in September, which seems quite optimistic considering the low level of the manufacturing PMI (43.4 in September), quarterly growth in industrial production would be between -0.5% and -1.0% qoq during Q3 as a whole.

Next, the volume of retail sales (published last week) fell by 1.2% mom in August, following a more moderate contraction of 0.1% mom in July. Similar to the industrial production data, the 3Mo3M change in retail sales was negative in August (-0.2%). And also similar to the changes in industrial production, stable or moderately higher retail sales in September (which would also be quite optimistic considering that consumer confidence is at a historically low level and fell further in September), would keep the quarterly growth rate between -0.5% qoq and -0.8% qoq. Having said that, the volume of retail sales does not include sales of passenger cars, which have accelerated sharply in recent months, probably because of the clearing of past backlogs after the easing of supply chain bottlenecks. Indeed, new passenger car registrations rose by 5.0% mom in August, following 3.7% in July. This means that total goods consumption probably fell less sharply than suggested by the retail sales numbers. However, given the relatively low weight of new cars in the total volume of goods consumption in the eurozone, goods consumption probably still contracted in Q3. Summing up, the hard monthly economic data that has been published so far indicate contraction in activity moving into Q3.