Eurozone disinflation well on its way

Two key economic reports published in the eurozone today, are indicating that disinflation is well on its way. To begin with, HICP inflation fell to 2.9% in October, down from 4.3% in September and next, GDP contracted by 0.1% qoq in Q3.

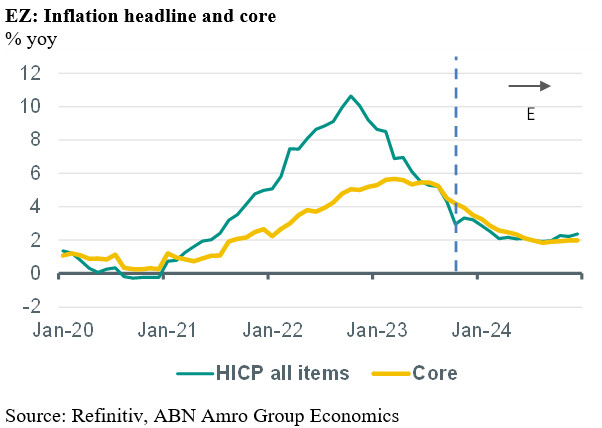

Eurozone inflation falls rapidly

Two key economic reports published in the eurozone today, are indicating that disinflation is well on its way. To begin with, HICP inflation fell to 2.9% in October, down from 4.3% in September, which was below the consensus and our own forecast. The bulk of the drop was thanks to energy price inflation, which fell to -11.1% from -4.6% on the back of a sharp negative base effect (in October 2022, energy inflation peaked at 41.5%), but the inflation rates of all other main components also declined in October. The inflation rate of food, alcohol and tobacco fell to 7.5%, down from 8.8% in September, services price inflation declined to 4.6% from 4.7% and non-energy industrial goods price inflation fell to 3.5% from 4.1%. Energy price inflation is still influenced by the implementation and unwinding of government support measures after the start of the war in Ukraine. This will continue to impact household energy inflation for the rest of this year and in the first half of 2024. Still, based on recent trends in energy commodity prices, we think that the trough in energy inflation has been reached now, and we expect a rise in the coming months, which could also result in overall inflation temporarily rebounding somewhat in the short term. In contrast to the potential rise in energy price inflation, we expect all other main components of inflation to continue to weaken during the rest of the year and in the first half of 2024. To begin with, the impact of the 2022 jump in energy prices on the inflation rate of energy-intensive goods and services is waning, while downward base effects should reduce food price inflation. Next, ongoing weakness in consumer demand is limiting the room for companies to pass on further rises in input prices to consumers. Finally, recent survey results and monthly labour market reports from individual countries have indicated that labour market conditions in the eurozone are deteriorating on the back of the continued economic weakness (also see below). Indeed, we expect unemployment to move higher in the coming quarters, which will limit wage growth and the parts of inflation that are most sensitive for wages, such as certain parts of the services sector. All in all, we expect headline inflation to approach the ECB’s 2% target in 2024Q2. Core inflation should trail a bit behind, and reach the ECB target around the middle of 2024.

Eurozone GDP contracting

According to the first estimate, eurozone GDP contracted by 0.1% qoq in Q3, following a 0.2% expansion in Q2. The outcome was a bit below the consensus forecasts but in line with our own. The decline in GDP in Q3 means that the eurozone economy was almost stagnant over the past four quarters (yoy growth was only 0.1% in Q3, down from 0.5% in Q2). No details have been published yet, but we think private consumption was roughly stagnant in Q3, while fixed investment probably contracted on the back of low producer confidence, high interest rates and sharply tighter bank lending conditions. The only positive impact on growth could be from foreign trade, as imports seem to have been weaker than exports. We expect another contraction in GDP in the final quarter of the year (we have pencilled in -0.2% qoq) and a moderate recovery to begin during the first half of next year.