Eurozone banks tighten credit standards

The ECB has published its Bank Lending Survey (BLS) for 2022 Q1. The survey was conducted after the Russian invasion of Ukraine and also after the ECB’s hawkish pivot and announcement of the reduction of its APP purchases. On balance, banks tightened credit standards on loans to enterprises in Q1, with the balance between ‘tightened’ and ‘eased’ rising to 6, up from 2 in 2021Q4. In the forward looking part of the survey banks’ expectations for the net tightening of credit standards jumped to the highest level since the peak of the pandemic in early 2020 and also the same level as during the eurozone crisis of 2011-12. The results from the BLS survey confirm that the eurozone economy will remain lacklustre in the coming quarters. Also, the results of the BLS add to the evidence that ECB’s own projections for GDP growth probably will need to be revised significantly lower.

Banks tighten credit standards in reaction to Ukraine conflict and changes in ECB policy

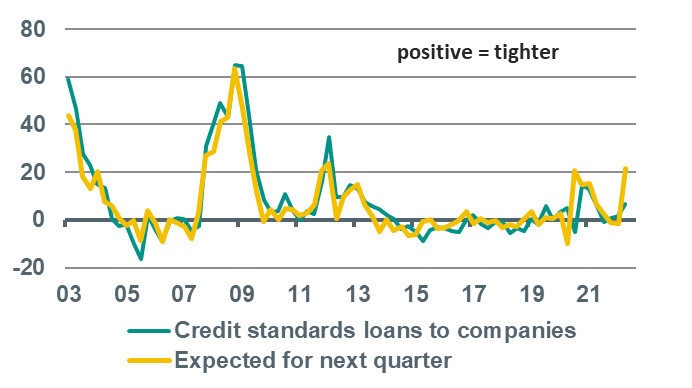

The ECB has published its Bank Lending Survey (BLS) for 2022 Q1. The survey was conducted between 7 and 22 March, which was after the Russian invasion of Ukraine and also after the ECB’s hawkish pivot and announcement of the reduction of its APP purchases. On balance, banks tightened credit standards on loans to enterprises in Q1, with the balance between ‘tightened’ and ‘eased’ rising to 6, up from 2 in 2021Q4. According to the ECB report banks referred to high uncertainty and a tightening impact from the general economic and firm-specific outlook. Banks were concerned about the impact of supply chain disruptions, high energy prices and other input costs, as well as exposure to Russia, Ukraine and Belarus on firms’ credit risk. There was also a tightening impact from banks’ risk tolerance.

Bank’s credit standards on loans to companies

Balance (tightened minus eased)

Source: ECB, the euro area bank lending survey

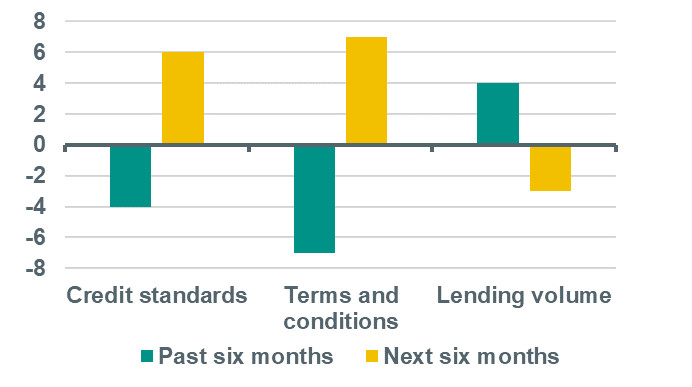

In the forward looking part of the survey banks’ expectations for credit standards in 2022Q2 increased to net tightening of 21, which is the highest level since the peak of the pandemic in early 2020 and also the same level as during the eurozone crisis of 2011-12. The details of the forward looking component of the survey show that there are high levels of uncertainty related to the Ukraine conflict and that this will remain a major factor behind the tightening of credit standards. Furthermore, the expected changes in ECB policy also play an important role. Indeed, in the ad hoc questions of the survey banks reported that their access to money markets, securitisation and particularly debt securities deteriorated, in net terms, in Q1, reflecting the tightening of financial market conditions for banks. Also, in the ad hoc questions, banks report that the ECB’s asset purchase programme had had a positive impact on their credit standards on loans to companies, their terms and conditions for loans to enterprises and the actual lending volume during the past six months, whereas they expect all these things to turn into negative during the next six months.

The impact of the ECB’s asset purchase programme on lending to companies

Balance (tightened minus eased or increased minus decreased)

Source: ECB, the euro area bank lending survey

With regards to loan demand by companies, banks reported that loan demand continued to be driven by a strong positive impact of firms’ financing needs for working capital reflecting supply chain disruptions, as well as precautionary inventories and liquidity holdings in an environment of high uncertainty. Loan demand stemming from fixed investment intentions was much weaker in Q1 (albeit still rising), but slowed down noticeably compared to 2021Q4 (balance to 9 from 19). All in all, the results from the BLS survey confirm that the eurozone economy will remain lacklustre in the coming quarters, which seems to be in line with our base scenario of eurozone GDP growth being close to the trend rate in the coming quarters. Also, the results of the BLS add to the evidence that ECB’s own projections for GDP growth (3.7% in 2022) will need to be revised significantly lower.