EUA price determinants and the transition process

EU carbon emission prices are governed by supply and demand forces. The supply of allowances is pre-determined by policy, while demand for allowances would be driven downwards by higher abatement efforts and more investments in renewables. The level the carbon price affects the feasibility and business case for low emission technologies and, in consequence, the transition towards these technologies.

EUA price determinants and the transition process

The price of the European Union emission trading Allowance (EUA) is the main driver to reduce emissions and boost the transition process in covered sectors

The EUA price is governed by supply and demand forces. The supply of allowances is pre-determined by the emission cap and the linear reduction factor

Demand for allowances comes from the covered sectors and changes depending on inter and intra-sectoral dynamics. In general, demand for allowances would be driven downwards by higher abatement efforts and more investments in renewables

The level of EUA price affects the feasibility and business case for low emission technologies and, in consequence, the transition towards these technologies

Complementary measures and timely interventions, such as setting targets for emission efficiency, the use of Carbon Contracts for Difference (CCD), and facilitating the coordination between different stakeholders, will be needed to resolve these issues and reach climate goals on time

Introduction

The European Union Emission Trading Scheme (EU-ETS) is the flagship instrument to reduce emissions in the European Union. The EU-ETS is a cap and trade system in which a cap on emissions is set and translated into emission allowances. The cap is set to decrease over time with a linear reduction factor (set to 4.2% in the updated reforms) in order to achieve emission reduction targets in the covered sectors. The allowances are allocated through auctions or, under specific conditions, given for free to regulated installations. They are further traded in secondary markets.

The European Union emission allowance (EUA) price has an essential role not only in incentivizing relevant installations to reduce their emissions in the member countries, but also in boosting the transition process in the covered sectors through its impact on the feasibility and business case of low carbon technologies.

In this note we aim to understand the main EUA price determinants from the demand and supply side, along with shedding the light on the relationship between EUA price and the transition process.

Drivers of EUA price

As in any market, the EUA price is a product of supply and demand forces for allowances. From the supply side, the number of allowances available in the market is governed by the emission cap, the linear reduction factor, and the decisions governing the time of loading allowances to the market (front loading, or back loading) (1).

Demand for allowances comes from the covered sectors (2) and changes depending on inter and intra-sectoral dynamics. In general, demand for allowances would be driven downwards by higher abatement efforts and more investments in renewables. Noting that developments in non-covered sectors could also affect the EUA price. For instance, even though transport and real-estate sectors are not directly covered by EU-ETS, the developments in these sectors affect the carbon market through their effects on power demand. To better understand the dynamics, we focus on the electrification of the transport sector. This process will increase the demand for electricity, and unless the switch to renewables is growing at a faster rate, conventional fossil based power may become needed for longer period of time. Thus, the demand for allowances from the power sector will increase, driving a higher price for EUA.

(1) Front loading mean that more allowances are put in the market sooner than planned, while back loading induce a postponement of supply and the market become tighter. (2) EU-ETS covers the aviation, power generation, and heavy industry sectors. As of 2024, it will be extended to emissions from maritime shipping.

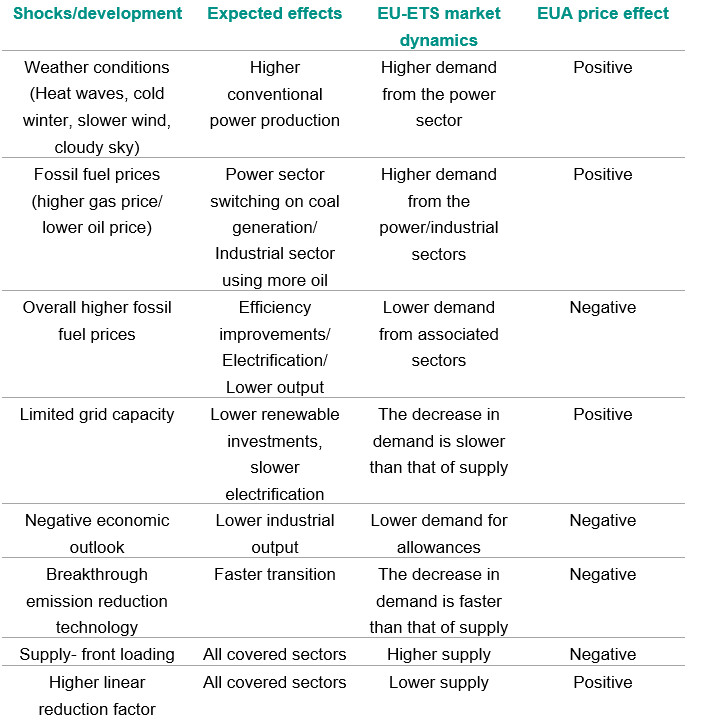

The table above summarizes main developments and their potential effect on EUA price.

Similarly, fossil fuel price affects the demand for allowances. For example, a negative supply shock to the gas market may trigger higher coal power generation raising the demand for allowances as coal is more carbon intensive than natural gas.

The economic cycle and sentiments towards economic outlook also affects demand for allowances as lower output in recession times translates into lower demand for allowances. Higher fossil fuel prices could also reduce energy demand (efficiency measures, or lower output, having the opposite effect on prices.

Moreover, the more we increase our reliance on renewable power, the more sensitive demand becomes to weather conditions. For example, heat waves and extreme cold could trigger a surge in demand for power which, in absence of sufficient storage, triggers more conventional power generation, more required allowances and higher EUA prices.

Additionally, a breakthrough technological discovery that reduces emissions in one of the covered sectors would induce a faster transition, lower demand for allowances, and lower EUA prices.

Under the same transition scope, there is a link between anticipated bottle-necks to the energy transition and the carbon market. For example, delays in grid capacity extensions would slow down renewable power capacity building, which in turn will hinder the development of green hydrogen that is needed for the transition of heavy industry. The combination of the slower industrial transition and the ongoing reduction of the cap will increase the EUA price. Noting that one way to avoid/mitigate this kind of dynamics would be for Europe to rely on imports for green hydrogen. However, in either case, the international competitiveness of European industries is affected (1). First, by the high cost of allowances, and second by the reliance on more expensive imports.

(1) The implementation of CBAM can alleviate this effect.

EU-ETS and the transition process

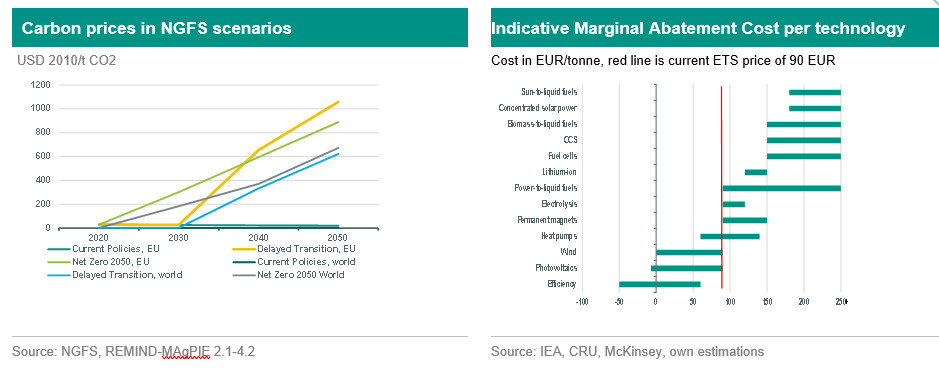

Carbon pricing is the main driver for the energy transition process as it provides incentives for different economic agents to switch towards a more sustainable low carbon practices.Accordingly, the level of carbon pricing plays an important role in governing the speed of the transition towards a certain climate goal. Scenario analysis is used to compare different pathways to reach such a goal under different levels of carbon pricing over time. The figure below depicts the carbon prices associated to different transition scenarios developed by the Network for Greening the Financial System (NGFS). The figure shows that the level of carbon price differs depending on the transition process under different scenarios. The timing of the introduction of an effective carbon price is of a high importance here. The delay in addressing emissions means that a higher carbon price will be needed to achieve the same climate goal. Accordingly, the carbon price is typically higher in the Net Zero scenario – particularly this decade - than in less ambitious scenarios. Furthermore, the carbon price to reach the same emission reduction target differs between different regions of the world due to differences in opportunities and sectoral composition to reduce emissions.

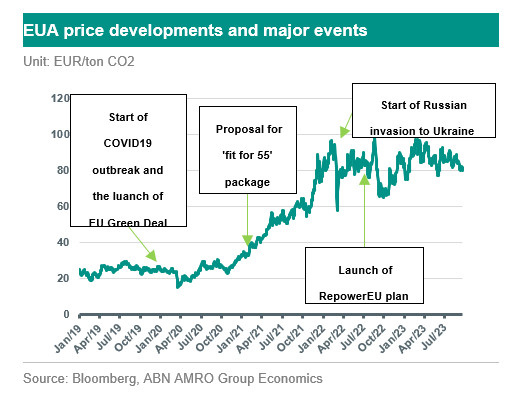

The EU-ETS represents the main driver for the transition of covered sectors towards a low carbon world. In early phases of the EU-ETS, the over-supply of allowances kept the EUA price at a low level that was not strong enough to speed up the transition. However, following the EU Green Deal and subsequently Russia’s invasion of Ukraine, reforms to the EU-ETS have been put in place: the fit for 55 package which increased the emissions reduction target to reach 62% by 2030 and the REpowerEU plan which entailed the use of 20 billion euros of allowance revenues to reduce the reliance on Russian gas.

It is worth noting that the development in the ETS price gives an indication of the speed of the transition in covered sectors. That is, as the speed of supply is decided upfront to meet the emission reductions, an increase in EUA price levels indicates that the reduction in demand is not matching the reduction speed in supply, indicating a slower transition. The other side of the coin would be that demand for allowances is also dependent on the transition speed, which in turn is linked to the availability of technological alternatives. For example, some hard to abate industries, which are mostly covered by the ETS, like steel, have green hydrogen as a strategic alternative to fossil fuels. However, the slow development of the associated infrastructure, such as pipelines to transport green hydrogen from where it is produced to where it is needed, will prolong the reliance on old technologies, slow down the transition, and entail higher price for allowances.

More specifically, the level of EUA price affects the feasibility and business case for low emission technologies. The figure above (right hand panel) depicts the link between the marginal abatement cost for different low carbon technologies against the EUA price. The figure shows that under the a permit price of 90 euros per ton of CO2, the business case of most of the transition technologies is still weak. Only efficiency measures, investments in wind and solar in the power generation have a positive business case. To make other decarbonization technologies more feasible, their marginal abatement cost should be reduced, or the EUA price should increase, or a combination of both.

Based on the costs of the needed decarbonization technologies to trigger the required transition, and given the upcoming reduction in supply, a rise in the EUA price in the coming years can be reasonably anticipated. This in turn will bring into play technologies such as CCS or biofuels.

Noting that the ETS price alone may still not be enough to trigger the required change especially when bottlenecks are present. Therefore, complementary measures and timely interventions, such as setting targets for emission efficiency and facilitating the coordination between different stakeholders, will be needed to resolve these issues and reach climate goals on time. Instruments such as Carbon Contracts for Difference (CCD) can also be used to boost the transition further (1). The main goal for this instrument is to reduce uncertainty to investors in order to ameliorate the business case of low carbon technologies. However, there are associated concerns that relate to market and futures distortions.

(1) CCD is an instrument the aim at setting a strike price for carbon emission permits under which the government will pay the difference to the industry.