ESG Strategist - Investors pricing rating downgrades for TotalEnergies

Last week, the oil and gas company TotalEnergies issued a EUR 1.3bn 20-year unsecured bond, which attracted over EUR 3bn in orders. Considering the global energy transition, it is important to examine how oil and gas companies are positioning themselves and how investors anticipate their future trajectories. An analysis of the bond curves for oil and gas companies reveals that these bonds, particularly those with longer maturities, are trading at levels comparable to those of lower-rated companies. These results may suggest that investors expect these companies to be downgraded by two to three notches in the future.

Last week, the French company TotalEnergies issued a 20-year senior unsecured bond, taking investors and the broader fixed income market by surprise given its maturity. The last time a long-maturity bond was issued by an oil and gas company was in November 2024, by BP, and the one before that was more than three years ago, in 2021.

Despite the unexpected move, the bond attracted strong interest, with demand reaching EUR 3.5 billion when the final terms were announced, resulting in a bid-to-cover ratio of around 3x. Despite the attention the bond attracted, it was priced at very generous levels at MS+140bp. As such, it is worth questioning what does this price tells us about the way investors perceive the company now versus how they foresee the company going forward.

In this note, we set out how the oil and gas market might look like over the long-term on the basis of various scenarios. Additionally, we will review TotalEnergies' sustainability reports and transition plans. Finally, we will compare oil and gas companies’ bonds with other similarly rated non-financial corporate bonds to understand how investors perceive different issuers and their future strategies.

The oil and gas market in 2045

The International Energy Agency (IEA), reports energy demand and supply expectations according to three different scenarios. The first is the Stated Policies Scenario (STEPS), the second is the Announced Pledges Scenario (APS), and the third is the Net Zero Emissions by 2050 (NZE) scenario. STEPS reflects the impact of existing and announced policy intentions and targets. It considers the trajectory of energy systems if current policies are implemented as stated, without assuming any additional ambitious measures. STEPS serves as a baseline to understand the potential future under current policy settings, and is also the scenario to which we will refer to for the remainder of this note.

According to the IEA's latest outlook , in the STEPS scenario, clean energy deployment accelerates while the overall pace of energy demand growth slows, leading to a peak in all three fossil fuels before 2030. With increasing reductions in coal demand, natural gas overtakes coal in the global energy mix by 2030. Between 2023 and 2035, clean energy grows more than the total energy demand. Driven by a surge in solar photovoltaic (PV) and wind power, clean energy becomes the largest source of energy by the mid-2030s. Consequently, STEPS envisions a threefold increase in renewables, reducing the share of fossil fuels from 80% of total energy demand in 2023 to 58% by 2050.

According to TotalEnergies 2023 sustainability report (), approximately 90% of their sales were derived from oil and gas, while the remaining 10% came from low-carbon energies. Given the latter and the outlook from IEA, traditional oil and gas companies like TotalEnergies, Shell, and BP are expected to lose revenues and face an increasing number of stranded assets unless they transition their business activities accordingly. Below, we examine the latest sustainability report published by TotalEnergies to gain insight into their future plans and strategies for navigating the ongoing energy transition.

TotalEnergies plans to be net zero by 2050

TotalEnergies has pledged to reduce greenhouse gas emissions (GHG) at their operated facilities (scope 1+2) by 40% by 2030, as represented by the red dots in the graph below. According to the company’s sustainability report, these targets align with the European Union’s “Fit-for-55” programme, which aims for a 37% reduction between 2015 and 2030, and with the IEA’s 2023 Net Zero Emissions (NZE) scenario, which proposes a 31% decrease over the same period. Additionally, the graph illustrates that these targets appear to be achievable, given the reduction trajectory the company has been following, as depicted by the red line.

However, the majority of emissions from oil and gas companies are attributed to their Scope 3 emissions. These include the emissions resulting from the combustion of the fuels they sell, such as gasoline, diesel, and natural gas. Such emissions occur when end-users, like vehicles or power plants, burn these fuels. Concerning Scope 3 emissions, TotalEnergies provides relatively limited information in its sustainability reports. The sole commitment related to Scope 3 emissions that we find is as follows: "We intend to decrease by 25% [by 2030] the carbon intensity of energy products sold, which accounts for the lifecycle emissions (Scope 1+2+3) of our energy products per unit of energy sold (g CO2e/MJ)." Moreover, the company adds that “an absolute reduction target for Scope 3 (…) without any change in energy systems and therefore without the reduction of the corresponding Scope 1 of energy users, would lead to a shift of this demand towards other supplies (…). This strategy would have no effect on lowering global GHG, and therefore no positive impact on climate, and would be contrary to the interest of our Company and its shareholders”. Hence, we conclude that the company seems to lack the ambition to reduce their scope 3 emissions, which might worry investors, as well as rating agencies about the company’s future.

Nevertheless, TotalEnergies has committed to be a net zero by 2050. For that, the company commits to produce:

About 50% of its energy in the form of electricity, including the corresponding storage capacity;

About 25% of its energy, equivalent to 50 Mt/year of low-carbon energy molecules in the form of biogas, hydrogen, or synthetic liquid fuels from the circular reaction; and,

Around 1 Mboe/day of Oil & Gas (about a quarter of the production in 2030, consistent with the decline envisaged by the IEA’s Net Zero Scenario), primarily liquefied natural gas with very low-cost oil accounting for the rest.

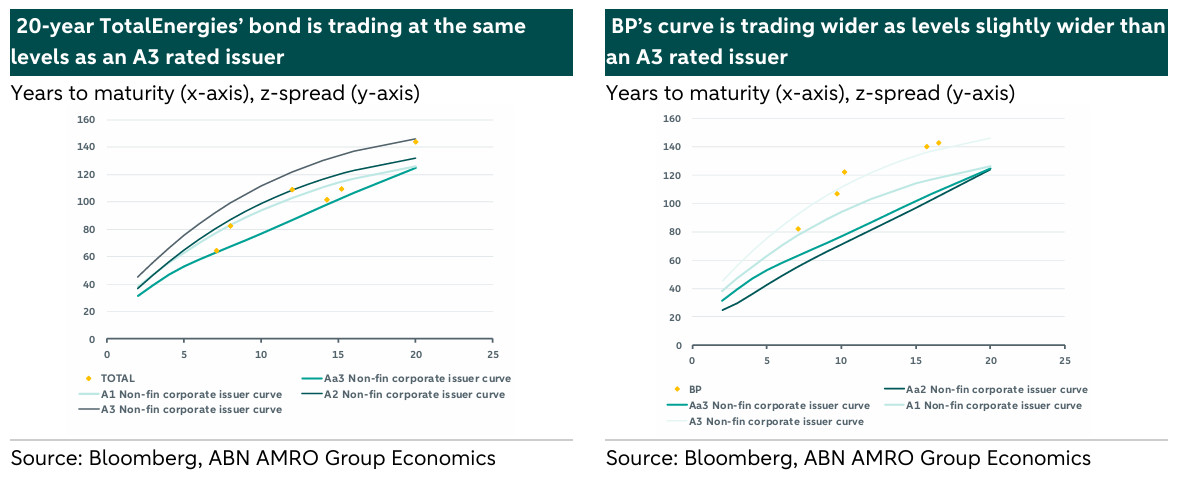

TotalEnergies’ long-term bond is trading at the same level as an A3-rated bond

In order to understand how investors perceive TotalEnergies and how do they look at the future of the company, we compare TotalEnergies’ curve with other similarly rated non-financial corporates’ curves (excluding oil and gas companies). Below we plot the graphs.

On the left-hand graph, we observe that TotalEnergies’ bonds, which are currently rated as Aa3, do not consistently trade at the same levels as bonds from other companies with the same Aa3 rating. For example, while TotalEnergies’ shortest-term bond aligns with the trading levels of other similarly-rated corporates, its long-term bonds appear to trade at levels comparable to those of companies with lower ratings. Specifically, examining the recent 20-year bond reveals that it is trading at a level akin to an A3-rated non-financial corporate. This could suggest that investors are anticipating a potential three-notch downgrade in the issuer’s rating in the future.

On the right-hand graph, we examine BP, a peer of TotalEnergies. The British company holds an A1 rating, which is one notch below TotalEnergies’ rating. Nevertheless, BP’s bonds seem to trade at significantly wider levels than those of similarly rated non-financial corporates. In fact, BP’s bonds, regardless of maturity, are trading at levels similar to those of an A3 non-financial corporate, much like the long-term bond of TotalEnergies.

These results may once again highlight investor perceptions of oil and gas companies and their future outlook over the next 20 years. Given the transition period we are currently undergoing, oil and gas companies that do not transition are expected to become increasingly outdated, with a higher number of stranded assets. Despite efforts by these companies to transition and invest in renewable energies, it is anticipated that their relevance in the global economy will diminish, potentially leading to downgrades in their ratings.

Finally, we examine the bond curves for Shell and Exxon. Both of these oil and gas companies have a current rating of Aa2, which is one notch above TotalEnergies and two notches above BP. However, as illustrated in the graph above, their bonds are trading at wider levels than those of similarly-rated corporates. For example, their bonds are currently trading at levels comparable to an A1-rated non-financial corporate issuer. This trading level is also two notches below the expected trading level for companies with their ratings.

Conclusion

Oil and gas companies are anticipated to be among the most affected by the global energy transition. With advanced economies aiming to achieve net-zero emissions by 2050, the worlds’ demand for oil is expected to decrease by 6% in the most optimistic scenario, and by more than 70% in the IEA's Net Zero scenario. Conversely, clean energies are projected to become increasingly significant, supplying more than 90% of the world’s energy needs, in a Net Zero scenario.

In light of this context, the issuance of a 20-year unsecured bond by TotalEnergies last week was unexpected. Given the anticipated changes, how will an oil and gas company strategically position itself for the next 20 years? And how do investors view it? According to our analysis, investors are already factoring in a potential two to three-notch downgrade for oil and gas companies, as evidenced by the latest 20-year bond being priced at levels comparable to a lower-rated non-financial corporate bond.