ESG Strategist - ECB unlikely to reshuffle corporate bond portfolio in 2024

The ECB released a new climate and nature plan for 2024-2025, where it mentions that it intends to explore the case for further greening of its monetary policy portfolios. However, this seems like a watered-down commitment compared to earlier communications, suggesting that an active reshuffling of the corporate bond portfolio towards greener issuers might not take place in 2024. Further supporting this point of view is that the ECB judges its corporate bond portfolio to already be Paris-compliant for 2024, mainly supported by redemptions of carbon-intensive issuers, as well as issuers’ own decarbonization efforts. However, we do not expect these tailwinds to be sustained for the upcoming years. Furthermore, the slow pace of winding down the portfolio will require the ECB to eventually be more active in order for its portfolio to remain aligned with the Paris Agreement.

The ECB released last week a new climate and nature plan for 2024 and 2025 (see ). The plan builds on a climate agenda released in 2022 (see ) and its adjustments reflect the changing environment and improvements in data availability and methodologies.

Specifically with regards to monetary policy, the ECB mentions that it intends to “explore, within its mandate, the case for further changes to its monetary policy instruments and portfolios in view of this transition [to a green economy]”. While this sentence might give market participants the idea that the central bank will step up its efforts to green its monetary policy portfolios, we argue otherwise. The wording applied by the ECB seems to have become more vague when compared to the 2022 agenda, and there is also lack of inclusion of more tangible action points under the detailed annex of the 2024-2024 plan.

One reason for that could be the end of reinvestments in July last year. After all, the primary goal of the ECB is maintaining price stability, which means that the volume of corporate bond purchases continues to be determined solely by monetary policy considerations. Since the implementation of the greening strategy in October 2022, the ECB has been using reinvestments to tilt its portfolio towards greener issuers. The end of reinvestments means therefore that the tilting strategy has come to a complete halt. That being said, under its new plan, more focus seems to be given to areas outside of monetary policy (such as for example, the greening of its non-monetary policy portfolios, which has been included as a more detailed action point under the annex of the 2024-2024 plan).

Previously, the ECB acknowledged that “the Paris Agreement requires a stable decarbonisation trajectory in [its] portfolio irrespective of [its] monetary policy stance or companies’ individual actions” (see ). This led Executive Board Member Isabel Schnabel to propose earlier last year a move from a “flow-based to a stock-based tilting approach”, which would mean that “absent any reinvestments, actively reshuffling the portfolio towards greener issuers would need to be considered” (see ). This would move the ECB towards an active buying and selling approach. While expectations were that such reshuffling would take place as soon as reinvestments ended, a closer look at the added and excluded securities of the CSPP portfolio since July 2023 demonstrates that such a strategy is not yet in place.

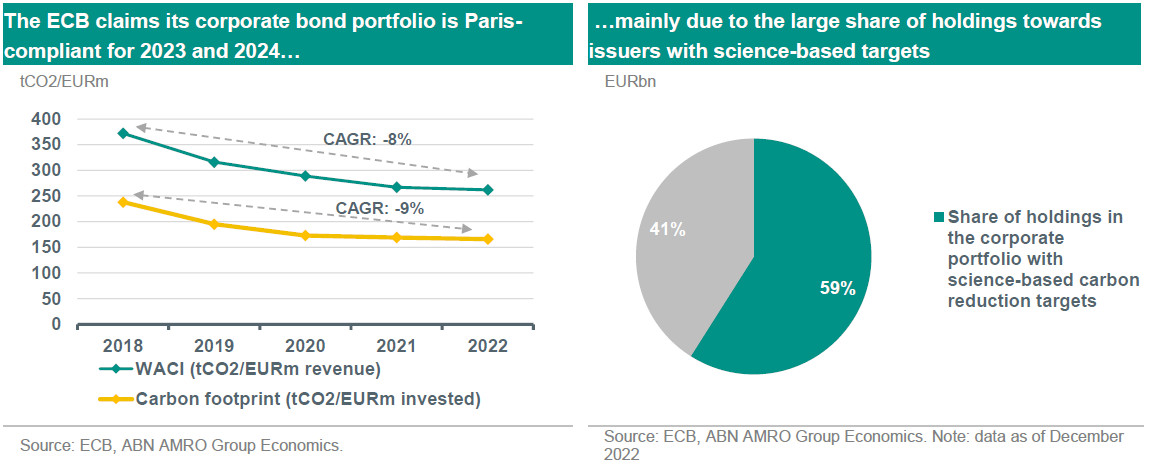

Given the more conservative wording of the ECB used in its new climate and nature plan and its (lack) of activities in the market over recent months, we think that such reshuffling will not take place in 2024. Our view is also based on the ECB’s assessment that its corporate bond portfolio is already Paris-compliant for 2023 and 2024. This was stated by Christine Lagarde at the end of last year (see more ):

“We recently concluded our one-year review of the tilting framework, and we expect the decarbonisation of our corporate sector portfolios to continue throughout 2023 and 2024 on a path that supports the goals of the Paris Agreement. There are three main factors driving this decarbonisation process. First, the effectiveness of our tilting approach. Second, redemptions of bonds with a relatively high carbon impact. And third, we see that issuers of the bonds we hold are actively working to reduce their carbon footprint, with benefits for society at large.”

At the same time, while it seems that the ECB will not engage in an active reshuffling in 2024, we argue that it seems likely that it will implement such strategy in the future.

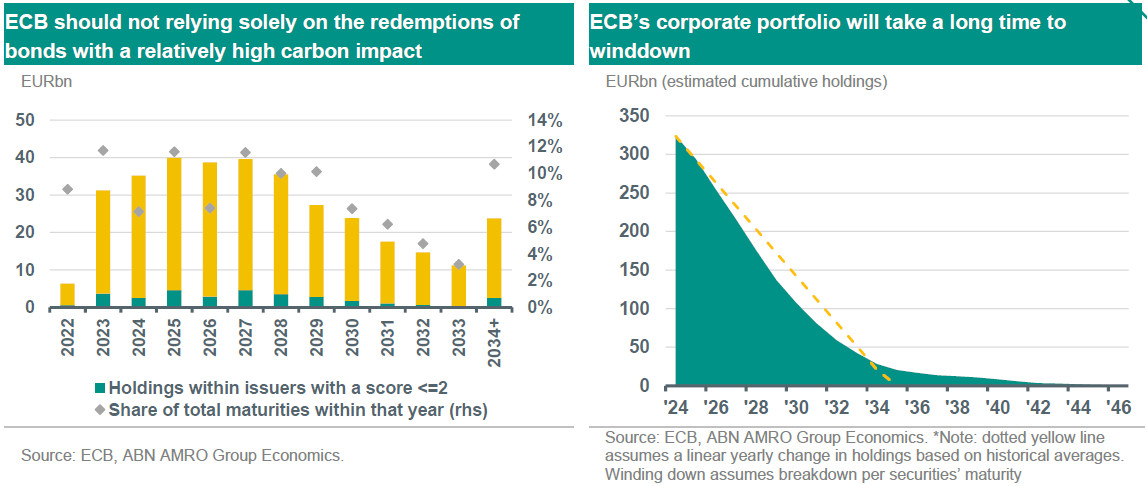

The ECB claims that its corporate portfolio is Paris-compliant due to, among others, “redemptions of bonds with a relatively high carbon impact”. While it is difficult to estimate the exact amount of holdings and the ESG score of the issuers included in the corporate bond portfolio, through our attempt to replicate those scores (see our previous note here) we can have an idea of how the maturity profile across different ESG scores looks like. This is summarized in the chart in the next page. Using ECB’s scoring system, where scores range from 0 (poor climate performance) to 5 (high climate performance), we evaluate the maturity profile for bonds of issuers that have a score of 2 or lower. Clearly, the ECB’s portfolio saw a high number of maturities in 2023 from bonds of issuers that have a poor climate performance according to the bank’s methodology. However, that will not be the case for this year.

For 2025, the pace of maturities picks up again, but the share of maturities from carbon-intensive issuers over the full maturity profile for that year still implies that more efforts might be needed. Furthermore, as shown also in the chart on the right hand side below, without an active approach, the ECB CSPP’s portfolio is only expected to winddown by 2034 the earliest. Hence, relying solely on carbon reductions by issuers implies a passive approach with very slow decarbonisation efforts – which, we judge, would not be Paris-compliant throughout the entire period.

Overall, it seems that the tailwinds that support a Paris-compliant ECB portfolio cannot be fully sustained into the future, indicating that a reshuffling will be likely be needed as long as purchases no longer remain part of ECB’s monetary policy. Still, given that an active reshuffling could result in the central bank having to market potential losses on its bonds sold, which might also be politically sensitive, it is likely that its assessment that the portfolio is currently aligned with the Paris Agreement will be used as a main argument to avoid reshuffling for the time being.

We note that the ECB is expected to release a new report updating the climate-related metrics of its corporate bond portfolio on March 2023. The report might provide more clarity on where the ECB stands with regards to its alignment with the Paris Agreement and, consequently, whether it hints on potential reshufflings for later this year. For now, we would deem it to be unlikely for 2024.